1. Introduction

Aotearoa New Zealand (Aotearoa) is a small island nation in the South-West Pacific, with a population of just over 5 million. It has a largely publicly financed health system with near-universal coverage of a wide range of health services, with services provided by a mix of publicly and privately owned providers. As with many other countries, it faces continual challenges with constraining overall health spending. Health inequities are also of ongoing concern, in particular for the Indigenous Māori population, but also for Pacific peoples, the disabled, those on lower incomes and those living in rural communities (Health and Disability System Review, 2019, 2020; Health Quality and Safety Commission, 2019; Ryan et al., Reference Ryan, Grey and Mischewski2019; Cumming, Reference Cumming2022).

This paper considers the potential for managed competition to successfully achieve key policy goals in Aotearoa. The paper first describes the key features of the health system between 2000 and 2022, and new organisational arrangements established from 1 July 2022 (Section 2). It then discusses managed competition plans that were developed in the 1990s, but which were subsequently abandoned (Section 3). In Section 4, the paper argues that the development in the 2000s of capitated, risk-bearing and competing Primary Health Organisations (PHOs) should be considered in terms of managed competition, and the paper points to the issues that have arisen in Aotearoa due to a lack of regulations that would have better supported the achievement of effectiveness, efficiency and equity goals through PHOs. In Section 5, the paper looks ahead to whether and how managed competition might again be considered in Aotearoa and the extent to which the system currently includes key pre-conditions to support such arrangements. Section 6 provides overall conclusions.

2. Aotearoa's health system

The following sections of this paper summarise key aspects of Aotearoa's health system. For further details, see Cumming (Reference Cumming2022). Note that a new, conservative, coalition government was elected to power at the end of 2023 and is likely to being making changes to the structure of the system in 2024.

2.1 Overview of financing and provision

The Aotearoa health system is predominantly publicly financed, with 80 per cent of expenditure coming from public sources (Organisation for Economic Co-operation and Development, 2022). The first key source of public financing is from general taxes (Cumming, Reference Cumming2022) (called ‘Vote Health’), making up 71 per cent of overall financing. There is near-universal coverage from this source, with some new immigrants the only ones not covered by public financing. A wide range of services are provided through public financing, but there are some notable exceptions, such as adult dental care, optometry and, until recently, primary care services such as mental health support through counselling or health promotion coaching (Cumming, Reference Cumming2022).

Around 50 per cent of this government funding is allocated to publicly owned organisations to deliver hospital and hospital-related services; a further third is allocated to privately owned providers to deliver primary and community care services (The Treasury, 2022). Most publicly financed services are delivered free of charge to service users, but there are a range of user charges, especially for primary care services.

A second key source of public financing is from a separate accident-related compensation (ACC) scheme. This covers all those in Aotearoa (including visitors), and is financed via social insurance levies from employers, employees, car registrations and fuel. It funds health, disability and rehabilitation services for those who have been injured, and it compensates for loss of earnings if people are off work due to an accident. There is then no right to sue for injury-related costs and recompense (Cumming, Reference Cumming2022). ACC funding makes up around 9 per cent of overall financing (Organisation for Economic Co-operation and Development, 2022).

A third source of financing is from out-of-pocket payments. These are of three types, making up around 13 per cent of total health expenditure (Cumming, Reference Cumming2022):

(a) Through user charges which are charged for some primary health care services.

(b) For services which are not covered by the publicly financed system, such as over-the-counter medicines, adult dental care and optometry services.

(c) For hospital services delivered by privately owned hospitals (e.g. for elective services such as hip operations).

A fourth source of financing is through private health insurance, which offers duplicate, complementary and supplementary coverage, including faster access to, e.g. elective services; choice of privately owned hospital and specialist; better facilities; coverage of user charges; and coverage of some services not generally available through the publicly financed system (e.g. dental care). It may also provide lump sum payments for those facing terminal conditions. People buy private health insurance from privately owned insurance companies, one of which owns some hospitals and general practices. Around 35 per cent of people have private health insurance (Cumming, Reference Cumming2022). Private health insurance makes up around 8 per cent of total health financing (Organisation for Economic Co-operation and Development, 2022).

Finally, there are a few other minor sources of financing, such as from local governments to support public health and through philanthropic funds.

Health expenditure reached 9.7 per cent of gross domestic product in 2020, with a per capita amount of US$4,469, lower than, for example, in Australia, Canada, the United Kingdom and the United States of America (Organisation for Economic Co-operation and Development, 2022). Total appropriations for health spending in the 2022/2023 government budget were NZ$24,009,000,000 (i.e. just over $24 billion) (The Treasury, 2022).Footnote 1

Overall, in terms of financing, the Aotearoa health system differs from other health systems by having a higher proportion of government financing and a lower proportion of out-of-pocket payments, by funding largely being capped through extensive government budget controls, by including community-based services for older people, by having ACC covering accident-related care, and by enabling the parallel purchase of private health insurance.

2.2 Organisational arrangements, as at June 2022

The Aotearoa health system had a fairly stable structure between 2000 and 2022, but the system was reformed from 1 July 2022. What follows is a brief description of the system as at June 2022; the new system is described further below.

There was a single, national governance structure, covering both health and disability services, with a Minister (and Associate Ministers) of Health overseeing the system, supported by the lead policy advisory and regulating agency, Manatū Māori/Ministry of Health (the Ministry). Until 1 July 2022, the Ministry was also a purchaser of some services (e.g. public health, midwifery and ambulance services, and services for disabled people aged under 65). There was a separate Minister for ACC.

Twenty geographically based District Health Boards (DHBs) were funded by the Ministry, through a weighted population-based funding formula. DHBs planned services for their regions and owned and delivered hospital and hospital-related services. They also purchased a range of primary and community services from privately owned providers (e.g. primary care, pharmacy, laboratory, home and residential care services and disability support services for those aged 65 and over). DHBs also purchased some services (e.g. elective services) from privately owned hospitals, using public finances.

Thirty PHOs, funded through DHBs, oversaw primary care arrangements for those enrolled. A national, weighted capitation formula was used to fund PHOs; PHOs in turn had to pass most of this funding onto the primary care providers with whom they had service delivery contracts.

There were then, and remain, many privately owned health care providers, delivering services. Many primary care and residential rest home providers are for-profit, while there are a wide range of not-for-profit providers also delivering care, including Māori- and Pacific-led providers, delivering health promotion and primary and community services (Cumming, Reference Cumming2022). All these providers were funded via contracts, either from the Ministry, their district DHB or a PHO.

A number of independent Crown organisations also supported the health and disability system, such as PHARMAC (which decides which medicines, vaccines and devices should be publicly financed and which negotiates prices and contracts with suppliers); a Health Quality and Safety Commission; a Health and Disability Commissioner, including an Aged Care Commissioner (which oversees a national code of conduct for health care providers and receives and acts on complaints); and a recently established Mental Health Commission.

A number of privately owned hospitals also delivered services, sometimes on contract to DHBs paid for through public financing (e.g. when DHBs could not meet elective services targets). These hospitals continue to deliver services, largely to those privately funding care, including via private health insurance.

Overall, the Aotearoa health system can be viewed as having had a more streamlined structure than many other countries, with a single, national Ministry, with a geographically based approach to planning and funding through DHBs, and with PHOs acting as meso-level organisations to support primary care providers. But, as with many other countries, service provision has been delivered through many organisations and by many health professionals, fragmenting service delivery.

2.3 Performance of the Aotearoa health system

Generally, the Aotearoa health and disability system has been seen to perform very well (Health and Disability System Review, 2019, 2020; Cumming, Reference Cumming2022). It has offered good overall value for money, providing high levels of life expectancy relative to health expenditure (Organisation for Economic Co-operation and Development, 2021), with recent improvements in life expectancy and reductions in mortality from, e.g. cancer and cardiovascular disease (Cumming, Reference Cumming2022). There is universal coverage of a wide range of services, and many New Zealanders have a choice of a wide range of service providers. There are many dedicated and well-trained staff.

There have been, however, some key concerns about the system's performance. These include key gaps in service delivery (e.g. adult dental care and, until recently, primary care counselling/health promotion); insufficient health promotion, preventive and primary care; user charges creating barriers to access to primary care; an increasing burden of long-term conditions; fragmented service delivery; a lack of responsiveness by key organisations to different health care needs (by gender, ethnicity and disability status); long and increasing waiting lists and times for elective services; and perceived poor incentives for efficiency. Of most concern have been significant inequities in health, quality of care and access to health services, particularly for the Indigenous Māori population, Pacific peoples, those on lower incomes or who live in less well-off areas and the disabled. There had also been increasing concern over the number of planning and delivery organisations, for a small population (see e.g. New Zealand Government, 1974; Upton, Reference Upton1991), with 20 DHBs and 30 PHOs during the early 2020s (Health and Disability System Review, 2019, 2020; Health Quality and Safety Commission, 2019; Ryan et al., Reference Ryan, Grey and Mischewski2019; Cumming, Reference Cumming2022).

2.4 Organisational arrangements from 1 July 2022

Between 2018 and 2020, a major review of the health and disability system took place (Health and Disability System Review, 2019, 2020), pointing to the above concerns and suggesting significant structural reforms. A new structure was established from 1 July 2022 including:

• Manatū Hauora/Ministry of Health, with a stronger Public Health Agency established within it (in response to COVID-19). The Ministry no longer purchases the range of services it previously did.

• A single, national organisation, Te Whatu Ora/Health New Zealand (Te Whatu Ora/Health New Zealand, 2022), that has taken over the roles of the 20 DHBs. It plans services, delivers services through its own publicly owned hospital provider arm and funds services through contracts with privately owned providers for primary and community services, including those previously funded by the Ministry. It employs over 80,000 people – the largest employer in Aotearoa by far (Dunkley, Reference Dunkley2020; Public Service Commission, 2022).

• A new organisation Te Aka Whai Ora/Māori Health Authority (Te Aka Whai Ora/Māori Health Authority, 2022), to oversee Māori health, and to purchase specific services to improve Māori health, including Kaupapa Māori services (i.e. services incorporating Māori worldviews and values).

• The establishment of around 80 localities, aimed at increasing the involvement of local communities and consumers in decision-making and developing more integrated delivery of a wider range of services at local level, through local provider networks (Department of Prime Minister and Cabinet, 2022). PHOs will no longer have a formal role in the system.

• The removal of disability from the system, and the establishment of Whaikaha/Ministry of Disabled People (Whaikaha/Ministry of Disabled People, 2022) to oversee disability policy and services (Sepuloni, Reference Sepuloni2021).

The details of how these arrangements would work were still being developed at the time of writing. However, a new government was elected at the end of 2023. Its policy platform includeing disestablishing Te Aka Whai Ora, merging its functions with those of Manatū Hauora and Te Whatu Ora. This change is likely to occur in 2024. It was not clear at the time of writing what other changes there might be to the system.

3. Road maps to managed competition: proposals in the 1990s

Managed competition models are seen as a means of employing ‘market dynamics’, such as competition and choice, to deliver more integrated care efficiently and equitably (Enthoven, Reference Enthoven1993, Reference Enthoven1994). It includes funding arrangements where some financial risks are passed onto key health care organisations, and where people have a choice of insurer/purchaser and/or service provider. It requires a set of ‘management’ regulations to be effective. In this section, I look at how managed competition was envisaged for Aotearoa in the 1990s.

The backdrop to Aotearoa considering managed competition in the 1990s was threefold.

First, the economy underwent major reforms during the 1980s, increasing the role of market forces in allocating resources. These reforms included opening the economy up more to international competition and removing major subsidies to key sectors (e.g. farming), as well as reorganizing government-owned organisations as State Owned Enterprises to deliver services on a commercial basis (e.g. postal and communications, and electricity services) (Cumming, Reference Cumming2022).

Second, two major reports were completed on the health system during the 1980s, with each considering how more market-based models might also work in health. These, however, did not result in major changes to the health system (Health Benefits Review, 1986; Hospital and Related Services Taskforce, 1988).

Third, in late 1990, a new National Party (conservative) government came to power, immediately establishing 17 major reviews, including for health, ACC, housing, social welfare, etc. The health system review document Your Health and the Public Health was published in July 1991 (Upton, Reference Upton1991). It recommended major reforms, arguing for purchasing and provision roles to be formally separated, and greater use of contracting and competition to drive change. This was known in Aotearoa as a ‘purchaser/provider’ split, and internationally as a ‘quasi-market’ (Le Grand and Bartlett, Reference Le Grand and Bartlett1993).

The reformed model was to be formally established on 1 July 1993. It included four Regional Health Authorities as government-owned geographically based purchasers and 23 Crown Health Enterprises operating separately as government-owned hospital and community care providers. Regional Health Authorities would hold funding for all health and disability services, could allocate funding as they determined and would have formal contracts with a range of publicly owned Crown Health Enterprises and with privately owned providers, all of which would compete against each other for contracts. Such contracts and competition would operate for all services (Upton, Reference Upton1991).

The goals of the reforms were to improve efficiency, quality of care and responsiveness, via competition and formal contracts. Crown Health Enterprises were set up to make a surplus, which would be reallocated to health and disability care, with an explicit goal of, e.g. reducing waiting times for elective services. People were to have a choice of providers in most parts of the country, and funding would follow those choices (Upton, Reference Upton1991).

This approach was designed as a transition stage towards a planned fully managed competition model. New privately owned Health Care Plans would eventually be allowed to compete with Regional Health Authorities for clients. People would be allocated a ‘voucher’ amount of government funding and could choose to purchase coverage from a government-owned Regional Health Authority or from a privately owned Health Care Plan. Regional Health Authorities and Health Care Plans would have contracts with health care providers to deliver services; potentially, they might have selectively and exclusively contracted with particular providers, developing as more integrated insurer/purchaser/provider organisations over time (Upton, Reference Upton1991).

The 1990s reforms therefore initially included work on the regulations that would support managed competition. This included (i) the establishment of a formal ‘core’ (or basket) of services to which all New Zealanders would be entitled and for which Regional Health Authorities and Health Care Plans would be held to account for delivering; and (ii) the development of a fair and equitable funding formula, to determine the ‘voucher’ amounts people would have from government funding to spend on their health and disability care.

The Core Services Committee was established to decide on core services (Cumming, Reference Cumming1994). However, the managed competition model was dropped before the Committee's work had really begun (see below). The Committee did, however, lead a national discussion on priority setting (see e.g. National Advisory Committee on Core Health and Disability Services, 1992); set up an elective services prioritisation and booking system (Fraser et al., Reference Fraser, Alley and Morris1993; Cumming, Reference Cumming, Siciliani, Borowitz and Moran2013); and worked on a range of national guidelines to support clinical decision-making (see e.g. New Zealand Guidelines Group, 2005). The elective services prioritisation and booking system still exists, but the Guidelines Group was abolished in 2016 (Cumming, Reference Cumming2022).

Work also began on a funding formula to determine the value of the vouchers that people would have to spend with their chosen Regional Health Authority or Health Care Plan. This, however, was to prove difficult, in part due to a lack of good information about relative health and disability care needs and about the existing use and cost of services, especially in primary care, where privately owned providers held most of the data needed, and in part due to concerns that competing Health Care Plans would select good risks, leaving the government-owned Regional Health Authorities serving higher risk populations.

In any case, the idea of transitioning through Regional Health Authorities to a managed competition model was dropped early in the reform process (Gauld, Reference Gauld2009). This was in part due to the reforms being highly contentious. The emphasis on competition was not supported, with major concerns over whether the desired gains would in fact be achieved in a small country such as Aotearoa. The reforms were very expensive to implement, requiring high levels of expenditure on consultants to unbundle funding, establish new entities and design and manage contracts and contracting processes. There were four Ministers of Health between 1990 and 1996 (Wikipedia, 2022) as the government struggled to implement the reforms and retain public confidence, including by putting in substantial new funding to keep the public on side.

There were some gains from these 1990 reforms. For example, there were some savings via new contracts for primary care and via a newly established PHARMAC; new Māori- and Pacific-led providers became established; and new meso-level Independent Practitioner Associations were set up to support and co-ordinate services, and support quality improvement initiatives, across general practice primary care providers.

But, overall, the model did not work in the ways expected; nor did it deliver the expected gains. For example, it proved difficult to contract on the basis of quality, due to a lack of information, while opening Crown Health Enterprise services to competition could lead to higher prices as they sought to recover losses and avoid increasing deficits. Few savings eventuated from Crown Health Enterprises and waiting times for elective services actually increased. Various Ministers placed key restraints on aspects of the model (e.g. asking Crown Health Enterprises to give six months' notice of intention to quit services), and, in practice, Regional Health Authorities and Crown Health Enterprises were effectively in local monopsony-monopoly arrangements (see below).

Following the removal of the surplus requirements for Crown Health Enterprises and the move to a more collaborative (rather than competitive) approach in the mid-1990s, the four Regional Health Authorities were in 1997 amalgamated into a single, national Health Funding Authority, in order to reduce contracting costs and improve national consistency. (For further details on the reforms see Crown Company Monitoring Advisory Unit (1996); Ashton (Reference Ashton, Boston, Dalziel and St John1999); McLean and Ashton (Reference McLean and Ashton2001); Cumming and Mays (Reference Cumming and Mays2002); Ashton et al. (Reference Ashton, Cumming and Mclean2004a, Reference Ashton, Cumming, McLean, McKinlay and Fae2004b); Ashton et al. (Reference Ashton, Mays and Devlin2005); Gauld (Reference Gauld2009); Cumming (Reference Cumming2022).)

The market-based reforms were completely overturned in late 1999, following the election of a Labour-Party-led (left-leaning) government, leading to the ‘local’ DHB model in place until 30 June 2022 (Gauld, Reference Gauld2009; Cumming, Reference Cumming2022).

4. Road maps to managed competition – primary care – 2002–2022

Although the attempt to introduce managed competition into the health system in the 1990s failed, there developed from 2002 on a key example of where there are risk-bearing providers and where competition occurs, and which might be thought about in terms of managed competition; and that is with primary care services.

As a result of the Primary Health Care Strategy (King, Reference King2001), the government enabled the establishment, from 2002 on, of privately owned and managed but publicly financed meso-level PHOs. PHOs would oversee primary care planning and provision for those enrolled with them, with services delivered by primary care providers which PHOs would have contracts with. PHOs were to be funded on a capitation basis, using a weighted formula (see below). In practice, New Zealanders would actually enrol with their local general practice, which in turn would join a PHO. General practices could voluntarily join a PHO, or not; but if they did not, they could not access new funding and hence would be unlikely to be able to offer lower user charges.

Over the past 20 years, PHOs worked with primary care providers (mostly general practices) to deliver services to those enrolled. PHOs funded general practices using the same capitation formula as the PHOs themselves receive, but it has been up to practices to fund their owners and staff however they wish (Croxson et al., Reference Croxson, Smith and Cumming2009). PHOs have supported general practices with enrolment and funding systems, with new service development and implementation, and they have also delivered services across a range of practices (e.g. health promotion, specialist nursing roles, practice pharmacist roles). A pay-for-performance programme was initially part of the PHO arrangements, but is no longer formally in place (Cumming, Reference Cumming2022).

PHOs were effectively mini health plans, albeit focused only on primary care. They competed against each other, although not so much for service users, as for providers who bring enrolled service users with them. At first, there were over 80 PHOs, with a good deal of competition, but over time, they have been encouraged to merge and there are now 30. In some parts of Aotearoa, there is still competition between PHOs for providers/enrolees; but in other parts of the country, there is a single PHO, and primary care providers have no choice but to join that PHO if they are to access the higher amounts of government funding available only through PHOs (Cumming, Reference Cumming2022).

Thus, Aotearoa has had aspects of a competitive health plan model in place since the first PHOs were established in 2002, and continues to have competitive health plans in parts of the country where there are multiple PHOs operating within a former DHB district. However, the regulations that (in theory) would deliver effective, efficient and equitable PHOs in a managed competition model are missing in Aotearoa. This has had serious consequences for the performance of primary care in recent years.

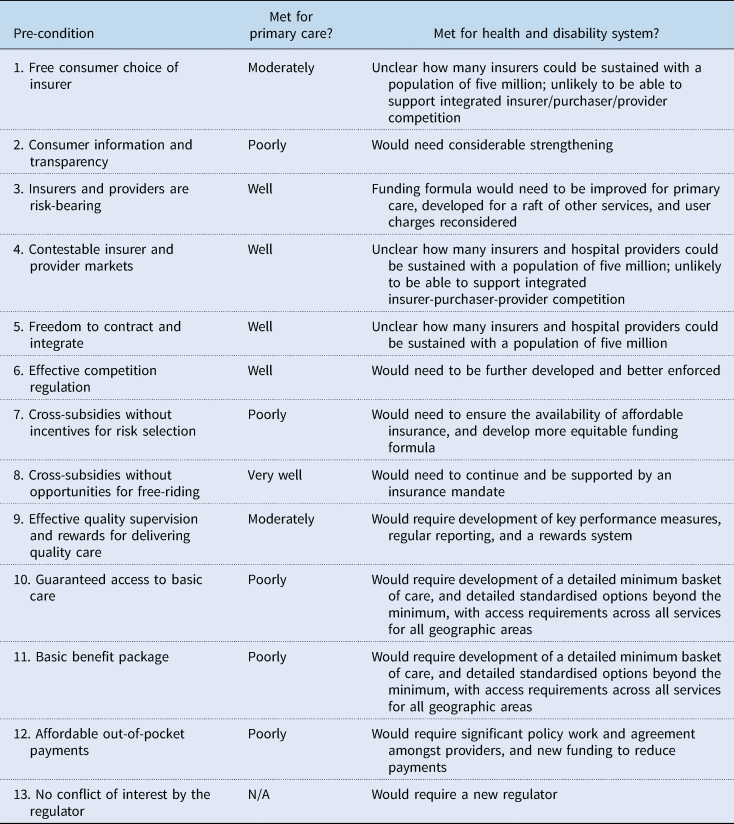

The following sections discuss whether the pre-conditions for managed competition are relevant to, or exist to support, effective, efficient and primary care delivery in Aotearoa. An assessment is provided of how well Aotearoa achieves the pre-conditions, including very poorly, poorly, moderately, well or very well. Table 1 summarises how well Aotearoa performs with respect to each pre-condition.

Table 1. Meeting the pre-conditions for managed competition in primary care and at the health and disability system level in Aotearoa

First, is free consumer choice of insurer, in this case, capitated general practices and PHOs. On the one hand, many New Zealanders do have a choice of which general practice to enrol with, and they can switch practices very easily. But there may be very limited choice of general practices in rural areas, while, increasingly, general practices are closing their books to new enrolees (see below). Many general practices then have a choice of PHO, but some will have only one PHO operating in their area.

On the other hand, there is no guaranteed enrolment in Aotearoa. Although it might have been difficult to have an enrolment mandate at general practice level, as this would potentially force small general practices to take on more patients than they could work with, a guarantee of enrolment with the much larger PHOs could have put the onus on PHOs to find and/or set up new practices with which people could enrol. The lack of a mandate has likely contributed to a steady increase over time in the number of people not able to formally enrol (General Practice NZ, 2022), which means they have no continuity of care, and they likely pay more for services as casual patients.

Overall, taking into account the existence of considerable choice of general practice and PHO, but also the lack of an enrolment mandate and its consequences, on balance, Aotearoa does only moderately well in terms of this pre-condition for primary care.

Second, is consumer information and transparency. Information on price in terms of insurance is not relevant, as the government directly funds PHOs and general practices. But there are user charges for primary care, and consumers will usually know the price of care at any particular general practice (e.g. with information available online or on general practice noticeboards), so the system does well on this score. But even the limited information on quality of care that was available through the performance programme is no longer available for PHOs, and performance information has never been available for individual general practices, where arguably it is more relevant, as that is where service users make choices, over which practice to enrol with. Crucially, there is no ‘core’ of services which all PHOs and general practices are to deliver (see below). This means that people enrolled with different PHOs and general practices may not get the same access to services as those in another PHO or general practice – but people cannot tell this as no such information is available. Aotearoa therefore scores poorly on this pre-condition.

Third, both insurers and providers should be risk-bearing. This is the case in Aotearoa, as PHOs and general practices both bear financial risk through the capitation formula. However, general practices can mitigate some financial risk through their ability to set their own levels of user charges. Practices delivering services in more wealthy parts of the country can also do this more easily than practices operating in lower income areas. Although user charges do reduce moral hazard amongst service users, there are long-standing concerns that the charges act as major barriers to access to primary care in Aotearoa, especially for those with higher needs and/or on lower incomes. There are now some rules around how much general practices can increase their user charges by each year, but it is not clear how well those rules are operating (Cumming, Reference Cumming2022). On balance, Aotearoa scores no better than well on this pre-condition.

Fourth, both the provider and insurance market should be contestable, with limited barriers to entry and exit. In Aotearoa, the primary care market for PHOs is not always contestable, as DHBs have had the ability to determine whether a new PHO can be established in a particular geographical area. The primary care market for general practices is more contestable, as new practices can be relatively easily set up, provided they meet certain minimum standards (e.g. practitioners being registered with the appropriate authority; both medical practitioners and nurses delivering services) (Anonymous, 2022). Once approved, both new PHOs and general practices are eligible for government subsidies. So, Aotearoa scores well on this pre-condition.

Fifth, in terms of freedom to contract and integrate, PHOs as insurer/purchasers have the freedom to decide which providers to contract with, although funding levels are largely set through national agreements. Not all general practices will, however, have a choice over which PHO to join. Aotearoa thus scores well on this pre-condition.

Sixth, is effective competition regulation. Aotearoa's Commerce Act should prevent anti-competitive behaviour by PHOs and general practices. However, it is unclear how proactive the Commerce Commission is in actually preventing anti-competitive behaviours, given recent experiences with, e.g. petrol suppliers, supermarkets and some building products, where oligopolies prevail. Recently, the government has been stepping in to increase oversight of such businesses (Clark, Reference Clark2021, Reference Clark2022; Commerce Commission, 2022). Overall, on balance, Aotearoa scores no more than well on this pre-condition.

Seventh, is the issue of cross-subsidies without incentives for risk-selection, to ensure that all income and risk groups can afford premiums. In Aotearoa, the issue of affordable premiums does not arise in the publicly financed system. There is, however, the potential for risk selection problems arising from the weighted capitation funding formula used for PHOs and general practices, which is widely regarded as totally inadequate in terms of ensuring fairness and promoting equity. This is because the formula for ‘first-level services’ (the largest pool of funding) is based on age and sex only; it does not weight funding based on ethnicity and deprivation, where there is poorer health status, including earlier onset of key long-term conditions (Health Quality and Safety Commission, 2019; Ryan et al., Reference Ryan, Grey and Mischewski2019). The formula also means that those PHOs serving higher needs populations are not sufficiently paid for the work they do, threatening their financial viability (Primary Care Working Group on General Practice Sustainability, 2015; National Hauora Coalition, 2016; Waitangi Tribunal, 2020; Cumming, Reference Cumming2022).

The formula therefore generates financial incentives to both ‘cream skim’ (select the healthiest people) and ‘skimp’ on care (to encourage higher needs people to go elsewhere) (van Barneveld et al., Reference van Barneveld, van Vliet and van de Ven1996). Moreover, because there is no mandate for PHOs and general practices to accept all who apply to enrol, PHOs and practices can easily engage in cream skimming if they choose to do so. In recent years, there has been an increasing number of practices with ‘closed’ books, i.e. who do not take on new enrolees, or where new enrolees are limited to, e.g. family members of existing enrolees (General Practice NZ, 2022). This is in part due to significant shortages of general practitioners and primary care nursing staff, worsened by the COVID-19 outbreak (Health Quality and Safety Commission, 2022), but it could also be a means of providers avoiding enrolling higher needs patients who might cost more than they are funded for. Similarly, because there is no longer any quality information available at PHO level, and there never was such information at general practice level, and because there is no longer any performance programme (Cumming, Reference Cumming2022), PHOs and general practices can easily engage in skimping if they choose to do to. The extent to which professional values may over-ride these financial incentives for cream skimming and skimping has not been studied in Aotearoa. So, overall, Aotearoa scores poorly on this pre-condition.

Eighth, is the pre-condition of cross-subsidies without the opportunity for free-riding, requiring that all people be covered and pay their share of health funding. At the health system level, all New Zealanders do pay their share – through taxes. Thus, there is no free-riding at the system level and Aotearoa scores very well on this pre-condition in terms of the overall system. The same is not, however, true for private health insurance, which is entirely voluntary.

Ninth, is effective quality supervision and rewards for delivering quality care. There are some elements within the Aotearoa health system that promote quality of primary care, including through a Cornerstone accreditation process for general practices (Royal New Zealand College of General Practitioners, 2020), the work of the Health Quality and Safety Commission (Health Quality & Safety Commission, 2021) and the work of PHOs. However, more would need to be done to regularly and systematically assess quality of care across PHOs and general practices, and to make this information available, for Aotearoa to score more than a moderate on this pre-condition.

Tenth, is guaranteed access to basic care, ensuring that providers do deliver the services they should be delivering. Aotearoa scores poorly on this pre-condition, as there is no mandate for PHOs and general practices to take on all potential enrolees, there is no true minimum basket of services with clear access criteria, and there is no real monitoring that quality service delivery occurs.

Eleventh, is having a basic benefit package, to ensure a minimum standard of care is available to all and to ensure fair competition between insurers and providers. A range of standardised benefit packages would also allow service users to easily make comparisons across insurers. Aotearoa does not have such a package in primary care. There are some minimum standards set out in the national contract that PHOs and general practices sign, but the service descriptions are very general (e.g. ‘improve… health…through health promotion’; ‘maintain…health…through appropriate evidence based screening, risk assessment and early detection of illness, disease and disability’), and there are few access requirements (e.g. for services to be available within certain travel times, but not relating to how soon people should be seen when seeking an appointment) (Anonymous, 2022). Thus, Aotearoa scores poorly on this pre-condition.

Twelfth, is affordable out-of-pocket payments. It was noted above that the existence of these in Aotearoa allows general practices a way of avoiding the full financial risk associated with capitation payments. But most importantly, they have long been seen as a major barrier to access to primary care in Aotearoa, especially for high-needs and low-income populations. Median user charges have risen recently, reaching $39 in 2016/17 (in 2018 New Zealand dollars) (Jeffreys et al., Reference Jeffreys, Lopez, Russell, Smiler, Ellison-Loschmann, Thomson and Cumming2020). The government does provide additional funding to support those who may not be able to afford user charges, both through the tax and welfare system, as well as through schemes to keep user charges low (for those aged under 14 years of age, those enrolled in certain very-low-cost-access general practices and those with lower household incomes). There is a safety net (of 20 items per family per year) for prescription medicine user charges (which are usually $5 per item). But families would need to spend a lot more on the much higher cost general practice user charges before each individual family member reached the relevant safety net criteria for general practice services, where once someone has had 12 visits in a year, they become eligible for a high use health card, which must be applied for, and hence they are eligible for free care (Cumming, Reference Cumming2022). Aotearoa thus scores poorly on this pre-condition.

Finally, there should be no conflict of interest by the regulator, who would be responsible for the basic benefit package, enrolment mandates, contracts, funding arrangements and performance management, for example. Currently, oversight of the health system for these pre-conditions sits with key government agencies, and although they have no conflict of interest with respect to these functions, with primary care providers all being privately owned, they have not been approaching primary care from a managed competition perspective. On balance, Aotearoa scores well on this pre-condition.

5. Road maps to managed competition: a future health system?

The above section has considered how well Aotearoa meets the pre-conditions for managed competition within primary care, which comes closest at present in terms of having the features of a competitive, risk-bearing market. We could also ask how likely it might be that a more integrated, managed competition model could be introduced across the entire health and disability system.

Given, as noted earlier, that Aotearoa planned a managed competition model in the 1990s, that it was highly contentious, that it did not achieve the desired gains, and that it was swiftly dropped as an idea, it seems politically unlikely such a model would be considered again. However, setting this aside, this section considers other issues that might influence whether such a model could be contemplated in Aotearoa.

5.1 General issues

Aotearoa would firstly need to consider whether and how to link ACC arrangements with the health and disability systems, and to bring disability responsibilities back with health. On the one hand, ACC already operates as an insurer. However, the three systems work very differently from each other: for example, ACC is fully funded for future costs, while health and disability services are funded on a pay-as-you-go basis; ACC covers everyone (even visitors), while the health and disability systems exclude some people (especially new migrants); ACC offers a wider range of services (e.g. acupuncture, chiropractic care); ACC has financial incentives to deliver care in a timely way to get people off income-related compensation payments and back to work quickly; and contracting and payment arrangements also differ. Disability advocates would be unlikely to support linking disability support services with health, the health system being seen as too sickness focused, with disability services long seen as missing out to health priorities (Palmer, Reference Palmer2020). Overall, a significant amount of work would therefore be required to bring the health and disability systems and ACC together.

Aotearoa would secondly need to consider how to bring private health insurance together with the health, disability and ACC systems. If private health insurance companies were also to compete as insurer/purchasers or integrated insurer/purchaser/providers, Aotearoa would also need all the pre-conditions for managed competition to be met. Private health insurers would also have to move from their current largely complementary role to becoming insurers that cover, and manage risks for, all health and disability services. This approach would be a major shift in its role in Aotearoa.

Aotearoa would thirdly need to consider the feasibility of managed competition succeeding to achieve key goals. The main constraints are a likely lack of service provision competition, especially for hospital services. Given geographically the country is long and skinny, some populations are always going to face geographic barriers (e.g. rivers, mountains) to get to services, and there are always going to be the regionally or nationally (not locally) based higher-technological hospital services. Some highly specialised services are only available in the largest centre (Auckland), with tertiary services only available in five centres, in Auckland, Waikato, Wellington, Christchurch and Dunedin. Competition between (currently publicly owned) hospitals is really only possible in three of these centres (Auckland, Wellington and Christchurch), and even then, in Wellington and Christchurch, only between two hospitals in each case. For other secondary hospital services, typically, there is only one publicly owned main hospital in many parts of the country. There are privately owned hospitals, largely in the main centres; but, even where these exist, they are not full-service hospitals (e.g. they do not support emergency or intensive care services, and have major gaps in service delivery). If Aotearoa were to create meaningful competition in the hospital market, it would require significant new investment in hospital facilities. Over time, more telehealth services might be possible, but there is a significant amount of investment required to make telehealth services more widely available in Aotearoa.

In terms of other services, there are already difficulties with providing some services in many parts of the country, given workforce shortages (e.g. general practitioners, nurses, pharmacists, disability support and residential rest home service staff). The potential for competition would also be difficult if it were expected that each competing insurer/purchaser or insurer/purchaser/provider were to offer, for example, culturally appropriate services for Māori, Pacific, disabled and other populations; there are extremely limited numbers of such providers already.

5.2 Does Aotearoa have the pre-conditions in place for managed competition?

Beyond these issues, does Aotearoa have the pre-conditions in place to appropriately regulate a managed competition approach? Looking at the pre-conditions for a more integrated, competitive approach across all services, the following issues arise. Table 1 provides a summary (see column three).

In addition to better managing the issues raised with respect to primary care discussed above, two main issues arise.

First, significant attention would need to be paid to the issues already discussed for primary care, to improve regulatory arrangements, in this case across all services, significantly increasing the scope of regulatory work required. Most importantly, there would need to be better consumer information and transparency, strengthened funding formula across all services, performance measures across all services, guaranteed access to basic care and a basic benefit package.

Second, with respect to pre-conditions 1, 4 and 5, it is highly unlikely that Aotearoa could sustainably support competing integrated insurer/purchaser/providers. Competing insurer/purchasers that have overlapping contracts with providers may be a possibility, but the limited competition in the provider market – especially for hospital services – would make such a model difficult to run efficiently. Administration costs would likely increase significantly as providers have to check coverage with insurers and as providers would have multiple contracts with multiple insurers.

6. Concluding remarks

It is unlikely that Aotearoa will consider a managed competition model in the near future.

Firstly, re-consideration of the model would be highly risky politically. The model was first considered in the 1990s but was quickly abandoned as an idea. The market-based reforms that were implemented did not achieve the gains expected of them and were also abandoned by the end of that decade. Any new attempt to develop a managed competition would be seen as returning to an unsuccessful past.

Secondly, it would also be difficult to sustain the competition required to make managed competition work, especially in relation to hospital services. Significant new investment in new, competing hospitals might allow for an efficient provider market to be established, but such services are unlikely to be seen to be priorities. This is especially the case given there is a need to deal with key social determinants of health (such as poverty, education, employment and racism), enhance health promotion and primary care services to improve health and wellbeing and to reduce inequities in health, replace ageing infrastructure, and grow the workforce, including the Māori and Pacific workforces to better meet those populations' needs.

Thirdly, establishing a managed competition model would require a significant amount of reform and regulatory work (see Table 1), unlikely to be viewed positively when there is so much pressure on enhancing the workforce and delivering services.

As has been shown in this paper, however, Aotearoa needed to have been thinking about the extent to which its arrangements in primary care established risk-bearing competitive mini health plans (PHOs), and whether the regulatory arrangements in place have supported the key goals of effectiveness, efficiency and equity in the past 20 years. It is clear from the discussion in Section 2, and from Table 1, that Aotearoa does not have many key pre-conditions in place to support PHOs as competing health plans, and that major problems have arisen as a result. The overall result is a system that has not delivered well on stated key goals, especially with respect to equity.

A new structure for health and disability services came into being on 1 July 2022. PHOs had no formal planned role in the new structure, but they remained in place at the end of 2023 as mini health plans and the problems with not thinking of them through a managed competition lens remain. It is, however, likely that, under the new government elected at the end of 2023, that the capitation funding formula will change soon, and it is to be hoped that it adequately adjusts for need to ensure better access to services and fairer funding for providers, both at PHO and at general practice level.

Beyond PHOs, new locality arrangements were being established. These might have become be funded via a weighted capitation formula, but as localities were to be geographically determined, and people wwould not have a choice over which locality they belong to, some problems that arose from having competing risk-bearing providers (such as incentives for cream-skimming) would no longer be relevant in Aotearoa, although it would still be important to ensure that the funding reflects high needs and was fair and equitable. Whether individual providers within localities were to be funded in ways that make them competing risk-bearing providers was yet to be seen. If they were, careful consideration needed to be given to the regulations that might be needed to ensure these latest reforms succeeded, especially in promoting equity, where previous reforms have failed. However, the future of localities is now also not clear as a result of a new coalition government being elected into power at the end of 2023.

Acknowledgements

The author acknowledges funding support for this paper from the Asia Pacific Observatory on Health Systems and Policies.

Open access

Open access