1. Introduction

As a measure to provide liquidity to Chilean households, which faced mobility restrictions and reduced activity in the context of the 2019 coronavirus (COVID-19) pandemic (Madeira, Reference Madeira2023), three laws (in July 2020, December 2020, and April 2021) were approved that allowed the exceptional withdrawal of part of the pension savings of members of the pension system (Madeira, Reference Madeira2022b). The Chilean pension withdrawals, as a response to social unrest during the pandemic, were four times greater in terms of gross domestic product (GDP) than those of any other country (OECD, 2021; Madeira, Reference Madeira2022b), reducing pension assets in around 18% of the pre-pandemic GDP and affecting the contributory pension savings of almost 11 million workers (Evans et al., Reference Evans, Pienknagura and Miur2021; Fuentes et al., Reference Fuentes, Quintanilla, Rueda, Salvo, Herrera and Toledo2021). The pension withdrawals weakened the financial position of workers with respect to their future retirement (Fuentes et al., Reference Fuentes, Quintanilla, Rueda, Salvo, Herrera and Toledo2021). Furthermore, the local capital market suffered a negative impact due to the reduced availability of pension savings for long-term investments such as stocks, corporate bonds, and mortgage loans (Evans et al., Reference Evans, Pienknagura and Miur2021). The low level of contributory pension savings has intensified calls for reform (Evans et al., Reference Evans, Pienknagura and Miur2021; López and Rosas, Reference López and Rosas2022; Parada-Contzen, Reference Parada-Contzen2022; Madeira, Reference Madeira2022b), leading to the approval of a new pension law in January 2025, which introduced significant changes to the Chilean pension system.

This study analyzes the impact of pension withdrawals on Chilean social security affiliates and their households, as well as their implications for retirement income. Our study improves on previous literature by: (i) using a unique combination of survey data and administrative information; (ii) elaborating a methodology to simulate the future pension contributions of a sample of affiliates and their eligibility for government transfers; and (iii) measuring the fiscal costs of the Chilean non-contributory pensions under different policy reforms. Our results show that allowing for pension withdrawals without any required conditions as in the Chilean case can be expensive for governments in terms of higher solidarity transfers. However, fiscal costs can be reduced through reforms such as delaying the retirement age or increasing the contribution rate (although such reforms may be politically difficult to implement).

We use a unique combination of administrative information for the universe of the social security affiliates in Chile, which is then used to calibrate the pension savings losses of a representative survey sample of households. We used information on the withdrawals from the Superintendency of Pensions’ anonymous affiliate database and cross-referenced it with socioeconomic information on affiliates from the Unemployment Insurance Fund. Using this anonymous affiliate database, we obtained the average withdrawal amounts for each of the three withdrawals, as well as the average residual balance after the withdrawals, according to the affiliates’ age, gender, education and quintile of taxable income. We then used the Chilean Household Finance Survey (Encuesta Financiera de Hogares, in spanish, hence on EFH) of 2021 and imputed the average value of the three withdrawals and the residual balance for each household member, using their age, gender, education and quintile of taxable income. After imputing the value of the withdrawals and residual balance for each household member, we then estimate the average withdrawals experienced by the households.

Our analysis confirms that 36.5% of Chilean social security affiliates entirely depleted their contributory pension balances. We find that both lower-income individuals and low income households withdrew a higher percentage of their individual accounts, which is consistent with the findings of (Fuentes et al., Reference Fuentes, Mitchell and Villatoro2023). Thus, the effects of pension withdrawals are very similar for the populations of affiliates and households. This is due to two factors: (i) 11% of households have only one adult member and (ii) many households mix affiliated members of different genders (i.e., male and female partners), but in most cases, these are members with similar age, education, and income.

We then simulate the workers’ labor paths and accumulated pension contributions until their retirement at age 65 years, under a no-reform and under different reform scenarios. At the time of retirement, the future pension is estimated as a life annuity using the predicted life expectancy of the sex and age cohorts (from the United Nations forecasts, (ECLAC, 2020)). The solidarity component to the final pension (contributory plus solidarity contributions) is then calculated.

Our baseline simulation exercise considers two counterfactuals under a no-reform scenario: (i) with the pension withdrawals and the new non-contributory pension law of 2022 and (ii) without the pension withdrawals and the legislation that increased non-contributory pension benefits in 2022.Footnote 1 We analyze the counterfactual pension income and government pension transfers of the current generation of workers and retirees in both scenarios. Therefore, the object of our analysis is the joint effect of the three pension withdrawals and the PGU 2022 law, which were legislated during the COVID-19 pandemic period, between 2020 and 2022. Furthermore, we also provide exercises showing the potential effect of the new pension reform legislated in January of 2025.

We show that the withdrawal effects on contributory pension income are large and persist over several years. However, due to the large expansion of public non-contributory pensions in 2022, the withdrawal effects are substantially reduced once the total pension income is accounted for. The results show an average reduction of 21% in the contributory pension, but a reduction of only 8% in the total pension, after accounting for government transfers. Government contributions in present value represent a fiscal cost equivalent to 78.9% of the pension withdrawals (an amount equivalent to 15.8% of the pre-pandemic real GDP).Footnote 2

Policy reforms, such as the pension reform approved by Congress on January 29, 2025, can significantly reduce fiscal costs by lowering the value of government transfers to future retirees. To evaluate these impacts, we simulate five reform scenarios alongside the baseline scenario of no reform. These scenarios include: (i) an increase of 6% in the contribution rate (reflecting the recently approved reform); (ii) setting a unified retirement age of 65 years for both sexes; (iii) raising the retirement age by 2 years for both sexes; (iv) delaying retirement to age 67 for both sexes; and (v) and combining a delay in retirement to age 67 years with a 6% increase in the contribution rate (integrating the delay and the approved reform).

Our analysis shows that a 6% increase in the contribution rate has a greater impact on reducing fiscal costs than each of the options for delaying the retirement age separately. Higher contributions decrease fiscal costs to 61.8% of the pension withdrawals, while establishing a retirement age of 67 years reduces it to 62.3%. However, when both measures are implemented simultaneously, fiscal costs decrease further to just 38.1% of the withdrawals value (equivalent to 7.6% of the pre-pandemic real GDP), which is less than half the cost under the no-reform scenario. Under a 4% risk-free interest rate assumption, the current legislation proposal, which increases the individual contribution rate by 6% (but leaves the retirement age unchanged), is projected to lower the fiscal cost of withdrawals and non-contributory pensions by 3.4% of pre-pandemic GDP. Additionally, we conduct a robustness analysis to examine how fiscal costs vary with changes in the risk-free interest rate parameter.Footnote 3 Our findings indicate that fiscal costs (in present value) increase in scenarios with lower interest rates.

This paper builds on previous empirical analyses of the COVID-19 pension withdrawals in Chile. Earlier studies show that these withdrawals increased household liquidity during the pandemic, helping to reduce indebtedness (Cerletti et al., Reference Cerletti, Cortina, Inzunza, Martínez and Toro2024) and debt risk (Madeira, Reference Madeira2022a). Additionally, the withdrawals, combined with other household support measures, mitigated the decline in consumption during this period (Madeira, Reference Madeira2023). Expanding on this research agenda, our paper examines how affiliates and their households may experience changes in future pension income due to the pension withdrawals and the recently implemented 2022 universal guaranteed pension scheme, under no-reform and reform scenarios. Furthermore, we advance prior research by utilizing a representative sample of households and their members to simulate the future distribution of pension income, whereas earlier studies primarily focused on a limited set of representative worker types (Evans et al., Reference Evans, Pienknagura and Miur2021; Fuentes et al., Reference Fuentes, Quintanilla, Rueda, Salvo, Herrera and Toledo2021; Reference Fuentes, Mitchell and Villatoro2023). Our findings on the increased fiscal burden caused by the pension withdrawals and the universal pension of 2022 align with previous evidence showing that these measures may reduce households’ private savings rates (Madeira, Reference Madeira2022b).

This article also complements international evidence on the role of pension withdrawals, which are allowed in other countries under different restrictions. Among 6 developed countries, only the USA allows pension withdrawals with low penalties and justifications, while Canada and Australia allow withdrawals under a proof of extraordinary need (Beshears et al., Reference Beshears, Choi, Hurwitz, Laibson, Madrian and Wise2015). Australia also allowed withdrawals during the pandemic for workers under financial hardship (Bateman et al., Reference Bateman, Dobrescu, Liu, Newell and Thorp2023). Workers in the United States make significant withdrawals from their retirement accounts as soon as their age makes them eligible without penalty (Goda et al., Reference Goda, Jones and Ramnath2022), with stronger withdrawals observed after the Great Recession (Argento et al., Reference Argento, Bryant and Sabelhaus2015). Catherine et al. Reference Catherine, Miller and Sarin(2020) show that US retirement withdrawals allowed households to access extra liquidity during the pandemic, while avoiding costs to government liabilities. Our work presents a different view from (Catherine et al., Reference Catherine, Miller and Sarin2020) in the case of governments that may later be induced to increase non-contributory transfers to compensate for the withdrawals. Note that Peru also allowed large pension withdrawals during the Covid pandemic, depleting pension assets by roughly 10% of GDP (Olivera and Valderrama, Reference Olivera and Valderrama2022; Olivera, Reference Olivera2022), and is now considering pension reform.

This paper is organized as follows. Section 2 describes the Chilean pension system. Section 3 describes the data. Section 4 explains the methodology for simulating the workers’ future employment, income, and pension contributions until retirement. Section 5 shows the withdrawals’ effects on the population of future retirees under a no-reform scenario. Section 6 shows the effects of the 2025 Chilean pension reform and other policy alternatives on the estimated fiscal burden. Finally, Section 7 concludes with a summary of the findings and policy implications.

2. The Chilean pension system

2.1. Contributory, solidarity, and voluntary savings pillars

The Chilean pension system created in 1981 is based on three pillars (Berstein, Reference Berstein2010). Its major component is based on defined contribution accounts funded by the workers’ wages. There is then a second pillar based on non-contributory “solidarity” pensions, which are funded from general taxes. Finally, a third pillar is based on a supplementary component given by voluntary pension savings with tax benefits. The general pension age is 65 years for men and 60 years for women, although the “solidarity” pensions are available only at age 65 years for both genders.

The Chilean pension system’s first component is a fully funded, “defined contribution” scheme based on private retirement accounts owned by each worker. During their working years, employees are required to contribute 10% of their gross income to these accounts, which are managed by private Pension Fund Administrators (PFA, Administradoras de Fondos de Pensiones in spanish) and can only be accessed upon retirement. Each worker can select their preferred PFA (among 7 currently) and fund; there are five fund alternatives that vary by asset composition and risk exposure–ranging from low-risk options, close to government bonds, to high-risk portfolios with global investments in thousands of asset classes. If workers do not make a choice, they are automatically assigned to the more conservative fund offered by their designated administrator. The government acts as a guarantor of last resort in cases of unfavorable portfolio performance (Berstein, Reference Berstein2010). By the end of 2019, the pension funds amounted to 81% of Chile’s GDP, serving as a significant source of funding for corporate debt and equity.Footnote 4

The second pillar of the Chilean pension system consists of non-contributory “solidarity” pensions, funded by general taxes (Berstein, Reference Berstein2010). These pensions provide financial support to the most vulnerable families, including those with no retirement savings or very low savings. Until December 2019, retired individuals aged 65 years or older from families in the lowest three income quintiles were eligible for a pension subsidy. This subsidy ensured a minimum total monthly pension of 82,058 pesos (approximately 106 USD) and gradually decreased as the worker’s own pension amount increased. Once the pension reached 266,731 pesos (approximately 346 USD), retirees were no longer eligible for public pension benefits.Footnote 5

The third pillar of the Chilean pension system consists of voluntary contributions with tax benefits. This pillar allows workers to enhance their retirement savings by contributing to voluntary pension accounts managed by pension fund administrators, banks, or insurance companies. In 2008, the Collective Voluntary Pension Savings program was introduced, enabling employers to offer voluntary savings plans to their employees.

Since its inception as a defined contribution system in 1982, Chilean pension funds have delivered real interest rates averaging 7.6%. While the Chilean pension system is highly regarded for its sustainability and funding efficiency, it scores poorly in terms of the adequacy of pensions paid to retirees (Madeira, Reference Madeira2021). In recent years, public dissatisfaction has grown due to the low pension amounts received by retirees (Madeira, Reference Madeira2022b). This issue is primarily driven by two factors: a low contribution rate of 10% of workers’ earnings and high informality rates, which result in long periods without contributions for many workers, particularly women. Indeed, Chile’s 10% contribution rate is significantly lower than the OECD average of 19% (Inzunza and Ruiz, Reference Inzunza and Ruiz2024). Additionally, the retirement age—65 years for men and 60 years for women—is considerably lower than the current OECD average of 66 years for both men and women (OECD, 2021).

2.2. The pension fund withdrawals

Following the social upheaval of October 2019 (Madeira, Reference Madeira2022a), the Chilean pension system underwent significant changes to both the defined contribution and solidarity pillars. To address public discontent, the government introduced measures to strengthen the solidarity pension system. On December 11, 2019, Law 21190 established a minimum pension of 169,649 pesos (approximately 220 USD) for retirees aged 65 years or older, from families in the lowest three income quintiles.Footnote 6 The COVID-19 pandemic further deepened the social and political unrest, which prompted the government to implement an even larger increase of the solidarity pensions. On January 29, 2022, Law 21419 introduced the Universally Guaranteed Pension (Pensión Garantizada Universal in spanish, PGU), which raised the minimum solidarity pension to 185,000 pesos (approximately 228 USD), and supplemented contributory pensions by this amount for those perceiving under 630,000 pesos (approximately 780 USD).Footnote 7

The COVID health crisis caused widespread disruption in Chile (as in the rest of the World), with mobility restrictions and job losses leaving many households facing significant liquidity constraints. In response, the government implemented three exceptional pension withdrawal laws, which allowed workers to access their pension savings—funds typically reserved for use after retirement. These measures were aimed to address short-term financial challenges, but came at expense of the defined contribution accounts, therefore undermining the ability of many Chileans to secure adequate income during retirement, as later shown in this paper.

The first withdrawal, enacted on July 30, 2020, under Law 21248, permitted workers to withdraw a significant portion of their accumulated contributory pension savings without penalties or taxes. A second withdrawal, approved on December 10, 2020, under Law 21295, followed similar guidelines but introduced a tax on high-income earners. The third withdrawal, legislated on April 28, 2021, under Law 21330, further expanded access, allowing all retirees, including those with annuities, to withdraw funds. Like the first withdrawal, the third was tax-exempt but included an optional provision for workers to contribute an additional 1% to their accounts. Additionally, the third withdrawal uniquely permitted annuity retirees to advance their future rent payments. Table 1 summarizes these differences, including taxation rules and the absence of fund restoration requirements.

Table 1. Pension withdrawal characteristics

Note: This table highlights the main differences between withdrawal regulations. Only the third withdrawal allowed for annuity retirees to advance their rent payments. For a comprehensive regulatory analysis, please visit the Chilean Pension Supervisor site.

Each withdrawal wave had a 12-month window during which funds could be accessed, after which normal pension rules resumed, restricting access until retirement. All the withdrawals were available for anyone with available savings at the PFA’s, irrespective of their employment status and wealth, they could be taken in cash, check, or deposit, and there was no obligation for workers to replenish the withdrawn funds.

All the pension withdrawals were structured in the same way in terms of the amount that each worker could request from its individual defined contribution account. Each withdrawal allowed every affiliate to withdraw up to 10% of their savings, with a limit of 4,400,000 pesos (approximately 5,700 USD). However those with less than 35UF in savings (approximately 1,300 USD) could retire their entire balance. This meant that certain affiliates of the defined contribution pension system (people that had held a formal job in the past) could withdraw up to 100% of their funds, those with low enough savings. Table 2 provides the withdrawal limits.

Table 2. Withdrawal limits

Note: This table presents the retirement limits depending on the accumulated retirement savings. For a comprehensive regulatory analysis, please visit the Chilean Pension Supervisor site.

In a country of 19 million people, there were 10.6 million workers making use of the first withdrawal, 7.9 million using the second withdrawal, and 5.6 million using the third withdrawal (at this point, 3.8 million people had already exhausted their pension wealth), which corresponds to roughly 97%, 81%, and 57% of the account holders before the Covid pandemic early in 2020 (Fuentes et al., Reference Fuentes, Quintanilla, Rueda, Salvo, Herrera and Toledo2021). Until the end of 2021, the first, second, and third pension withdrawals implied, respectively, a total amount withdrawn of 20.3, 19.2, and 16.3 billion USD.Footnote 8 Overall, the three pension withdrawals represented 20% of the GDP, 18% of the total pension assets that existed at the end of 2019, depleted the accounts of around 4 million workers, and reduced the future pensions of more than 10.5 million people. Since the third withdrawal on April 2021, further withdrawals have been proposed, yet none have been approved.

Several other countries implemented some form of pension withdrawal during the Covid pandemic in 2020 and 2021 (Madeira, Reference Madeira2022b). However, the most significant pension withdrawals related to Covid measures were those in Peru and Chile, with withdrawal amounts above 18% of the total pension assets. Due to its weight on the GDP, the economic implications of the Chilean pension withdrawals may have strong implications for investment and growth in the near and medium term future.

2.3. The 2025 reform

On January 29, 2025, the congress approved a pension reform set to take effect in March 2025. Here, we introduce some key elements of the reform.Footnote 9

Employer’s contribution will gradually rise by 7% over a period of 9–11 years, on top of the 1.5% they already contribute to disability and survivorship insurance (Seguro de Invalidez y Supervivencia in spanish, hence SIS). From the total 8.5% increased contribution, 4.5% will go directly to individual accounts, while 4% will be allocated to a newly created social security fund, consistent with 2.5% SIS and 1.5% as a protected return contribution. The protected return contribution acts as a government-backed bond that workers accumulate over time. Upon retirement, these contributions are converted into amortizable bonds, which can be traded in financial markets or used to finance pension payments, ensuring the return of funds originally “loaned” to the system. This set of measures addresses both the contributory and solidarity aspects of the system.

Furthermore, the solidarity pillar is enhanced by gradually increasing the PGU to $250,000 pesos monthly (approximately 265 USD) in the span of 30 months, with all retirees aged 65 years and above being eligible for this rise. Additionally, two measures to reduce gender pension gaps were introduced, (i) a bonus per contributed year and (ii) compensation for life expectancy differences. Within the contributory pillar, individual pension savings will be automatically adjusted to match investment risk with the affiliate’s age. Furthermore, to promote competition, 10% of the affiliate pool will be randomly reassigned every 2 years to the PFA offering the lowest commission fees.

3. DataFootnote 10

Our analysis integrates multiple data sources to link withdrawal amounts and remaining pension balances to Chilean households. First, we use the anonymous withdrawal register reported by PFA’s to the Superintendency of Pensions. However, this dataset lacks socioeconomic information on affiliates.Footnote 11 To enrich this dataset, we cross-reference individual records from the Superintendency of Pensions with data from the public Unemployment Insurance Fund using a fictitious identifier.Footnote 12 This allows us to incorporate key socioeconomic variables, including age, gender, level of education attained, and taxable income. Using this information, we calculate the average percentages withdrawn by each group of policyholders based on their gender, age, education, and income quintile and associate these average balance values with individuals in other datasets such as surveys.

Subsequently, we use as a reference the members of the households surveyed by the EFH in its 2021 wave, which is conducted by the CBC since 2007. This wave includes 4,400 urban households nationwide. The EFH survey is useful for our purpose since it asks for a wide range of information on every household member’s demographic characteristics, its labor occupation and non-labor income, their social security affiliation, and knowledge of their account balances, plus self-reported values of other real and financial assets (including bonds, stocks, ownership of private companies, housing, other real estate properties and vehicles) and debts (including mortgage, educational, auto, retail, and consumer loans). The EFH survey has an over-representation of richer households, since rich households have more complex finances in terms of assets and debts and undertake a higher portion of the economic activity. To adequately correct for the over-representation of wealthier households, all the statistics in this article use expansion factors (or population weights), meaning that each observation is weighted with a number fi representing the statistical number of households equivalent to i (Madeira, Reference Madeira2019).

We link the pension account balances and withdrawal percentages from the administrative dataset of the Superintendency of Pensions to demographic groups by matching them with the gender, age, education, and income quintile characteristics of EFH survey household members. Using the reported balances of survey respondents, we estimate their withdrawals based on withdrawal percentages corresponding to their socioeconomic characteristics. For other household members, we reconstruct their balance and withdrawal history based solely on their demographic attributes and pension system affiliation status.

To evaluate the quality of the matching between the Superintendency of Pensions dataset and the EFH survey, we conducted the following two regressions:

(i)

$\text{Pre-withdrawals balance}_{k,t} = \beta_1 X_{k,t} + \varepsilon_{1,k,t}$

$\text{Pre-withdrawals balance}_{k,t} = \beta_1 X_{k,t} + \varepsilon_{1,k,t}$(ii)

$\text{Post-withdrawals balance}_{k,t} = \beta_2 X_{k,t} + \varepsilon_{2,k,t}$

Here,  $X_{k,t} = 1(\text{sex}_{k,t} \times \text{age}_{k,t} \times \text{education}_{k,t} \times q_{k,t}),$ which includes 2,698 dummy variables generated by the interaction of sex, age, education, and the five income quintile dummies based on the ranking of individual affiliates’ labor income. Using these regressions, we calculated the linear predictions for the pre-withdrawals and post-withdrawals balances as

$X_{k,t} = 1(\text{sex}_{k,t} \times \text{age}_{k,t} \times \text{education}_{k,t} \times q_{k,t}),$ which includes 2,698 dummy variables generated by the interaction of sex, age, education, and the five income quintile dummies based on the ranking of individual affiliates’ labor income. Using these regressions, we calculated the linear predictions for the pre-withdrawals and post-withdrawals balances as  $\hat{\beta}_1 X_{k,t}$ and

$\hat{\beta}_1 X_{k,t}$ and  $\hat{\beta}_2 X_{k,t}.

$

$\hat{\beta}_2 X_{k,t}.

$

The correlation coefficient between the actual pre-withdrawal balance and its predicted value ( $\hat{\beta}_1 X_{k,t}$) is 52.4%, while the correlation coefficient for the post-withdrawal balance and its predicted value (

$\hat{\beta}_1 X_{k,t}$) is 52.4%, while the correlation coefficient for the post-withdrawal balance and its predicted value ( $\hat{\beta}_2 X_{k,t}$) is 50.7%. These results indicate a reasonable fit between the balances in the original Superintendency of Pensions dataset and the mean values of each group used for matching with the EFH survey.

$\hat{\beta}_2 X_{k,t}$) is 50.7%. These results indicate a reasonable fit between the balances in the original Superintendency of Pensions dataset and the mean values of each group used for matching with the EFH survey.

Note that the matching between the Superintendency’s administrative dataset and the EFH survey is based only on key variables that influence contributory pension accumulation. The contributory pension balances considered in this analysis include only the first pillar of the pension system, which consists of compulsory contributions made by each worker during periods of formal employment.Footnote 13 Formal employment is influenced by factors such as sex, age, education, and skill level, as measured by income quintile (Madeira, Reference Madeira2015). Notably, only 56% of working-age women in Chile participate in the labor force, a comparatively low rate among OECD countries. However, financial variables such as debt and savings are not significant determinants of formal employment. Therefore, these variables are not included in the statistical matching between the administrative register and the survey dataset. Additionally, only variables present in both the pension administrative registry and the survey can be used for matching. Since debt and savings are not recorded in the pension registry, they cannot be incorporated into the matching process.

Our coverage of the total amount of pension withdrawals is adequate. Our matched value for the pension withdrawals corresponds to around 13,718 billions of pesos for the first withdrawal, 11,877 billions of pesos for the second withdrawal, and 12,084 billions of pesos for the third withdrawal. Furthermore, this corresponds to 25,595 billions of pesos for the sum of the first two withdrawals and 37,679 billions of pesos for the sum of the three withdrawals (Figure 4 shows these totals separated across income quintiles). These values correspond to 87.9%, 89.8%, and 96% of the total amount reported by the Superintendency of Pensions for the first, second, and third withdrawals, respectively (Superintendencia de Pensiones, 2022a; 2022b; 2022c).Footnote 14 In terms of the sum of the three withdrawals, our matched value corresponds to 91% of the total reported in the three reports of the Superintendency of Pensions. These values are slightly lower than the total withdrawal amounts reported by the Superintendency of Pensions for two reasons: (i) the EFH survey only represents the urban population (88% of the total population of Chile in 2022, according to the World Bank) and (ii) we use a cross-match between the Pensions dataset and the Unemployment Insurance Fund (which excludes workers that had contracts starting before 2008).

This methodology allows us to associate the withdrawals with the households surveyed by the EFH. It should be noted that we used the EFH to identify households, because it includes information on the financial balance of the Chilean households, which can be enriched with the average value of the withdrawals according to the affiliate’s characteristics. Additionally, the EFH survey sample indicates a considerable knowledge on the part of affiliates regarding their pension balances, as can be seen in Figure 1, with 44% of those interviewed stating that they know their pension balance in 2021, a substantial increase compared to 2017 (25%). It also shows that affiliates report having lower balances in their accounts, consistent with the withdrawals, as seen in Figure 2. One issue that negatively impacts the contributive pensions of lower income quintiles in Chile is the long dated practice of only contributing by the minimum wage even though the real labor income is above this threshold. This means that even if someone is formally employed, they might perceive a lower contribution toward their pension, since their labor income is partially formal and partially informal, even coming from a single employer.Footnote 15

Figure 1. Knowledge of the funds accumulated in the personal account.

Figure 2. Amount saved in personal account.

We found heterogeneous amounts and percentages withdrawn by households according to their income level. Figure 3 shows the amounts withdrawn by the total households in each quintile and accumulates the values for each subsequent withdrawal. It can be observed that the poorest income quintiles were able to access lower withdrawal amounts than the households in the higher income quintiles. The richest income quintiles accessed higher withdrawal amounts and their accumulated withdrawals grew substantially, since—unlike some poor households that withdrew their entire pension savings—their pension savings’ accounts were not depleted. Figure 4 provides information on the average percentage withdrawn from individual accounts, accumulated over time. The households in the different quintiles withdrew a proportion greater than 10% of their savings, which also increased over time. On average, households with lower incomes withdrew 42% of their pension savings, while the highest income quintile only withdrew 26%. We emphasize that these statistics are at the household level and hence might not match efforts made at the individual level, since our results are accounting for household composition. Composition is an important factor as (Fuentes et al., Reference Fuentes, Quintanilla, Rueda, Salvo, Herrera and Toledo2021) also note in their work at the individual level. Indeed, they find that active workers withdrew between 40% and 30% of their pension savings, given withdrawals limits on Table 2. By the third withdrawal, most still could not access the entirety of their savings. Also, only very young workers could access high percentages of their savings, but they are not the bulk of the labor force.Footnote 16 Additionally, our results are reported by income quintile, not wealth quintile (meaning that, for example, wealthy pensioners might fall in the lower quintile). Moreover, it should also be noted that the EFH surveys the urban population, and this is matched conditional on being in the unemployment insurance fund, which might also lead to differences.

Figure 3. Cumulative withdrawn amount.

Figure 4. Cumulative withdrawals as a percentage of the initial balances of the individual accounts.

Linking the withdrawals to the Household Financial Survey (EFH) enhances the analysis of Chilean households during this anomalous period. According to the EFH, household labor income declined; however, this decrease was more than offset by higher government subsidies, particularly for lower-income quintiles, resulting in relatively stable effective income levels. Figure 5 illustrates how withdrawals served as an additional source of liquidity for households by distributing the total withdrawal amount evenly over 12 months. The results indicate that the liquidity benefit from withdrawals increased with household income, meaning lower-income households had less additional liquidity available compared to wealthier households.

Figure 5. Household monthly effective income and perceived withdrawals.

4. Methodology

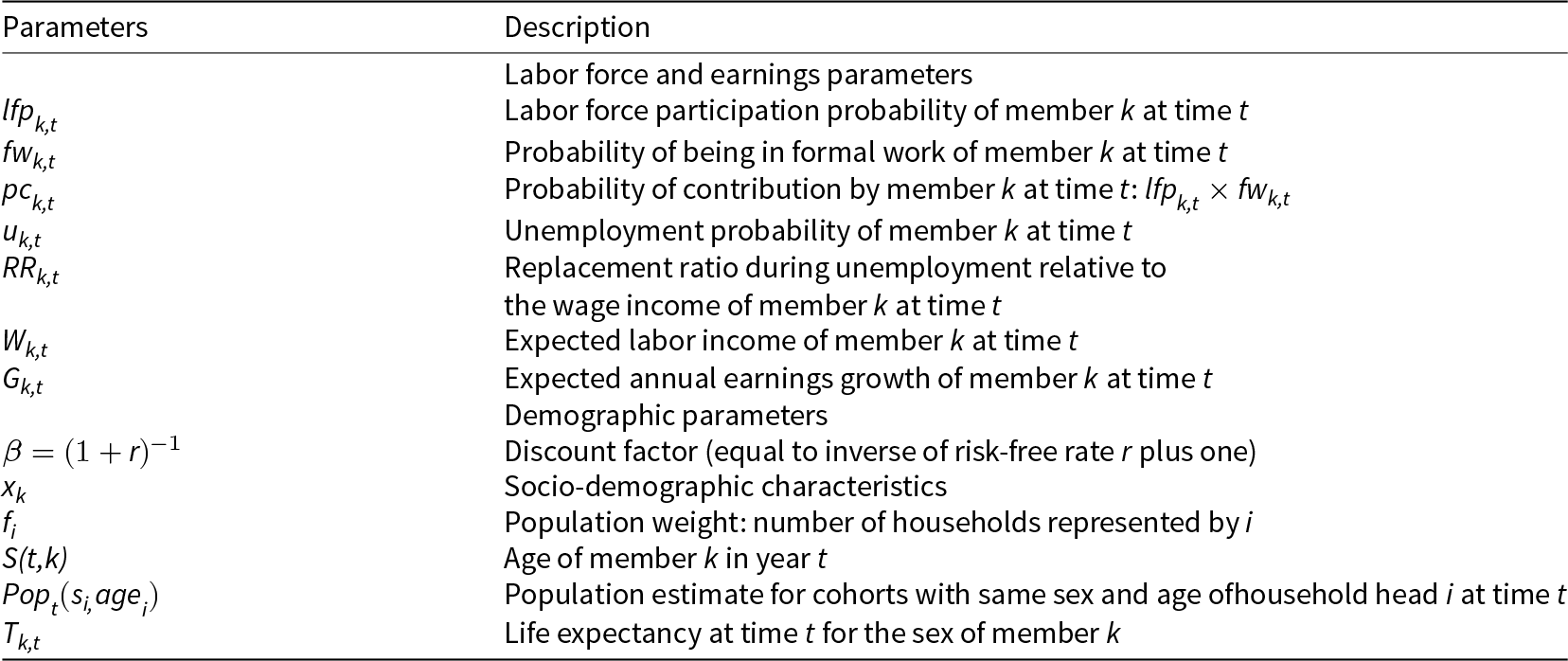

4.1. Parameters of the pension system

We simulated the future accumulation of pension contributions until age 65 years for all household members aged 26 years or older. The accumulation of contributions in each member’s individual account takes into account the probability of contributing, which is determined by the probability of each member being in formal employment, conditional on their gender, age (3 categories), education level (3 categories), occupation industry (3 categories), geographical area (Metropolitan Region or Other Regions), and income quintile. Additionally, we consider that expected income has an annual growth rate, conditional on gender, age, and education. The probability of being employed in formal employment and the annual income growth rate are calibrated with the New Supplemental Income Survey (Nueva Encuesta Suplementaria de Ingresos, in spanish, hence on NESI), a module of the New National Employment Survey (Nueva Encuesta Nacional de Empleo, in spanish, hence on NENE).

Table 3 summarizes the main components of the labor market and future pension contribution model for workers and lists the data sources used for the calibration. It should be noted that there are idiosyncratic labor risks (unemployment, formal employment, labor force participation), but there is no economic cycle; therefore, the labor market is the same as in 2018 and with a constant real interest rate of 4%. The model is very similar to the one used to analyze pension reform proposals discussed in 2015 (Madeira, Reference Madeira2021) and the effects of pension withdrawals on household saving rates in 2022 (Madeira, Reference Madeira2022a).

Table 3. Labor market and future pension contribution model for workers, with respective data sources

Source: (Madeira, Reference Madeira2021; Reference Madeira2022b). (*) For women we estimate retirement age based on a simulated workforce absence greater than 3 years after turning 60 years.

At the time of retirement, the future pension is estimated as a life annuity, using a duration based on the life expectancy in Chile at age 60 years by gender for each annual cohort of pensioners until 2060 (ECLAC, 2020). Using the life expectancy  $T_{k,t}$ by sex-age for each year t from United Nations estimates (ECLAC, 2020), the total pension solidarity contributions are then calculated based on the Guaranteed Universal Pension (PGU) legislated in January 2022. In our mathematical notation, we use subscript k for the household member (i.e., the individual worker), i for the household to which k belongs, and t for the time period (measured at the yearly frequency). The model’s labor market and demographic parameters are summarized in Table 4. Table 5 summarizes the parameters required to calibrate the pension system, either before 2020 or after 2022. Table 6 summarizes the main outcome variables calculated after the model’s simulations. We made publicly available all the software codes necessary to replicate the methodology and results of this article in Mendeley Data: https://data.mendeley.com/datasets/zn3cyzm7r5/1.

$T_{k,t}$ by sex-age for each year t from United Nations estimates (ECLAC, 2020), the total pension solidarity contributions are then calculated based on the Guaranteed Universal Pension (PGU) legislated in January 2022. In our mathematical notation, we use subscript k for the household member (i.e., the individual worker), i for the household to which k belongs, and t for the time period (measured at the yearly frequency). The model’s labor market and demographic parameters are summarized in Table 4. Table 5 summarizes the parameters required to calibrate the pension system, either before 2020 or after 2022. Table 6 summarizes the main outcome variables calculated after the model’s simulations. We made publicly available all the software codes necessary to replicate the methodology and results of this article in Mendeley Data: https://data.mendeley.com/datasets/zn3cyzm7r5/1.

Table 4. Parameters of the simulated future income and demography

Note: The table summarizes the main parameters used in the model for simulated future income and demography.

Table 5. Parameters of the pension system

Note: The table summarizes the main parameters used in the model for the pension system.

Table 6. Main model results

Note: The table establishes the model’s outcome variables after simulation.

To calculate representative population statistics for future years, we adjusted the population weights of each household i as follows:

\begin{align*}

w_{i,t}=w_{i}^{EPF}\dfrac{Pop_{t}(s_{i,}age_{i})}{Pop_{2021}(s_{i,}age_{i})},

\end{align*}

\begin{align*}

w_{i,t}=w_{i}^{EPF}\dfrac{Pop_{t}(s_{i,}age_{i})}{Pop_{2021}(s_{i,}age_{i})},

\end{align*} with  $w_{i}^{EPF}$ denoting the original EPF weights and

$w_{i}^{EPF}$ denoting the original EPF weights and  $Pop_{t}(s_{i,}age_{i})$ being the number of people in each sex-age bracket. Life expectancy for each worker k,

$Pop_{t}(s_{i,}age_{i})$ being the number of people in each sex-age bracket. Life expectancy for each worker k,  $T_{k,t}$, and population by sex-age

$T_{k,t}$, and population by sex-age  $(Pop_{t}s_{i,}age_{i})$ for each year t are obtained from United Nations projections (ECLAC, 2020).

$(Pop_{t}s_{i,}age_{i})$ for each year t are obtained from United Nations projections (ECLAC, 2020).

4.2. Current workers

Contributory pension wealth for each worker k is obtained as the sum of the value of the past pension contributions since joining the labor force (at age 25 years) until their current age ( $S(t,k)$), plus the present value of the future pension contributions until the retirement age Rk. In the Chilean pension system Rk is age 65 years for men, while women can choose to retire at age 60 years, but are only eligible for non-contributory pension benefits at age 65 years. We estimate their retirement age based on a simulated workforce absence greater than 3 years after turning 60 years.Footnote 17 The contributory rate from formal labor income in each period is cr, with mc being the top value of income considered for social security contributions. The probability of the worker k making a pension discount at time t,

$S(t,k)$), plus the present value of the future pension contributions until the retirement age Rk. In the Chilean pension system Rk is age 65 years for men, while women can choose to retire at age 60 years, but are only eligible for non-contributory pension benefits at age 65 years. We estimate their retirement age based on a simulated workforce absence greater than 3 years after turning 60 years.Footnote 17 The contributory rate from formal labor income in each period is cr, with mc being the top value of income considered for social security contributions. The probability of the worker k making a pension discount at time t,  $pc_{k,t}$, is equal to the probability of being in the labor force times the probability of doing formal work,

$pc_{k,t}$, is equal to the probability of being in the labor force times the probability of doing formal work,  $pc_{k,t}=lfp_{k,t}\times fw_{k,t}$, with

$pc_{k,t}=lfp_{k,t}\times fw_{k,t}$, with  $lfp_{k,t}=\Pr (LFP_{k,t}=1\mid

x_{k,t})$ and

$lfp_{k,t}=\Pr (LFP_{k,t}=1\mid

x_{k,t})$ and  $fw_{k,t}=\Pr (FW_{k,t}=1\mid LFP_{k,t}=1, x_{k,t})$. We consider independent workers with a contract and self-employed workers that provide receipts as formal workers. These workers are obliged to make contributions to the pension system, except for women above age 50 years, men above age 55 years, and workers with a total annual income lower than 4 minimum wages. In Chile, there is around 22% of informal labor participation, which does not provide contributions during their periods of informal labor (Madeira, Reference Madeira2022a).

$fw_{k,t}=\Pr (FW_{k,t}=1\mid LFP_{k,t}=1, x_{k,t})$. We consider independent workers with a contract and self-employed workers that provide receipts as formal workers. These workers are obliged to make contributions to the pension system, except for women above age 50 years, men above age 55 years, and workers with a total annual income lower than 4 minimum wages. In Chile, there is around 22% of informal labor participation, which does not provide contributions during their periods of informal labor (Madeira, Reference Madeira2022a).

The individual k members wealth  $PWI_{k,t}$ is given by

$PWI_{k,t}$ is given by

\begin{align}

PWI_{k,t}=12\times cr(\sum\limits_{h=25}^{S(t,k)-1}\bar{r}

_{h}pc_{k,t}\min(mc,P_{k,h})+\sum\limits_{h=0}^{R_{k}-S(t,k)}

\beta^{h}pc_{k,t}\min(mc,P_{k,h})),

\end{align}

\begin{align}

PWI_{k,t}=12\times cr(\sum\limits_{h=25}^{S(t,k)-1}\bar{r}

_{h}pc_{k,t}\min(mc,P_{k,h})+\sum\limits_{h=0}^{R_{k}-S(t,k)}

\beta^{h}pc_{k,t}\min(mc,P_{k,h})),

\end{align} with the permanent labor income of each worker k expressed as  $

P_{k,t}=W_{k,t}(1-u_{k,t}+u_{k,t}RR_{_{k}})$, and

$

P_{k,t}=W_{k,t}(1-u_{k,t}+u_{k,t}RR_{_{k}})$, and  $

W_{k,t},u_{k,t},RR_{_{k}}$ denoting the labor income of the worker while employed, the probability of unemployment, and the replacement ratio of income during unemployment, respectively (conditional on the characteristics

$

W_{k,t},u_{k,t},RR_{_{k}}$ denoting the labor income of the worker while employed, the probability of unemployment, and the replacement ratio of income during unemployment, respectively (conditional on the characteristics  $x_{k,t}$). The replacement ratio of income during unemployment spells is obtained as the income received during unemployment spells by workers employed in the previous quarter (Madeira, Reference Madeira2015), which is obtained from the rotating sample of the NENE-NESI survey datasets (that is, from the sample of households interviewed in the quarters 3 and 4 of each year):

$x_{k,t}$). The replacement ratio of income during unemployment spells is obtained as the income received during unemployment spells by workers employed in the previous quarter (Madeira, Reference Madeira2015), which is obtained from the rotating sample of the NENE-NESI survey datasets (that is, from the sample of households interviewed in the quarters 3 and 4 of each year):  $RR_{_{k}}(x_{k})=E(\frac{Y_{k,t}}{Y_{k,t-1}}\mid

x_{k},U_{k,t}=1,U_{k,t-1}=0)$.

$RR_{_{k}}(x_{k})=E(\frac{Y_{k,t}}{Y_{k,t-1}}\mid

x_{k},U_{k,t}=1,U_{k,t-1}=0)$.

Using the NENE and NESI surveys, we estimate the labor force participation, formal work, income growth, and unemployment risk parameters ( $

lfp_{k,i,t},fw_{k,i,t},G_{k,i,t},u_{k,i,t},RR_{_{k,i,t}}$), using the methodology in (Madeira, Reference Madeira2021), with around 538 mutually exclusive worker types given by the characteristics

$

lfp_{k,i,t},fw_{k,i,t},G_{k,i,t},u_{k,i,t},RR_{_{k,i,t}}$), using the methodology in (Madeira, Reference Madeira2021), with around 538 mutually exclusive worker types given by the characteristics  $x_{k}\in \{$Santiago Metropolitan area or not, Industry (primary, secondary, tertiary sectors), Formal sector, Gender, Age (3 brackets,

$x_{k}\in \{$Santiago Metropolitan area or not, Industry (primary, secondary, tertiary sectors), Formal sector, Gender, Age (3 brackets,  $\leq 35$,

$\leq 35$,  $35-54$,

$35-54$,  $\geq 55$), Education (secondary school or less, technical degree, college), and Household Income quintile

$\geq 55$), Education (secondary school or less, technical degree, college), and Household Income quintile $\}$. Only these variables were selected, because the NENE and NESI surveys do not have the same categorical variables for education and occupation every year (some years may have more categories, other years have fewer categories). These variables xk are found to be present in the NENE, NESI, and EFH surveys (Madeira, Reference Madeira2015) and allow us to simulate the labor market results of the EFH members for a long period of time.

$\}$. Only these variables were selected, because the NENE and NESI surveys do not have the same categorical variables for education and occupation every year (some years may have more categories, other years have fewer categories). These variables xk are found to be present in the NENE, NESI, and EFH surveys (Madeira, Reference Madeira2015) and allow us to simulate the labor market results of the EFH members for a long period of time.

4.3. Pension fund withdrawals

As we already introduced in Section 2, the Chilean congress implemented three pension savings withdrawals, starting on July 2020, for amounts established in Table 2.Footnote 18 As stated in this table, the laws regarding withdrawals were written in Chilean nominal pesos, but adjustments to pension benefits are regularly made to account for inflation.Footnote 19 This work does not consider inflation. Therefore, all analyses are done in real currency. Nonetheless, Chile usually uses an inflation indexed currency called Unidad de Fomento (UF) to refer to real amounts. Additionally, using UF allows us to simplify equations, therefore the remainder of this article uses the following values to translate all the income and pension benefits to this currency: (i) the EFH 2021 survey uses an UF value of 30,991 pesos, which corresponds to the average UF in December 2021 and (ii) the solidarity pension law of 2019 values use an UF value of 28,309 pesos; ii) the values of the solidarity law of 2022 use an UF value of 31,212 pesos. This means that if the worker had saved less than 35 UF, they could withdraw their total savings; if they had between 35 and 350 UF, they could withdraw up to 35 UF. If the savings were higher than 350 UF, they could withdraw 10% of their savings, up to an overall maximum of 150 UF.

The calibration considers the current parameters of the pension system: cr = 0.10 and mc = 78.3 UF.  $\bar{r}_{h}=\prod\limits_{l=t+h-S(t,i)}^{t-1}(1+r_{l})$ is the accumulated real asset return of the Chilean pension system between the last period

$\bar{r}_{h}=\prod\limits_{l=t+h-S(t,i)}^{t-1}(1+r_{l})$ is the accumulated real asset return of the Chilean pension system between the last period  $t+h-S(t,i)$ the worker made pension contribution and the current period t. Here rl denotes the realized interest rate for the pension fund system in Chile during the past period l. Future accumulated pension contributions earn the riskless interest rate:

$t+h-S(t,i)$ the worker made pension contribution and the current period t. Here rl denotes the realized interest rate for the pension fund system in Chile during the past period l. Future accumulated pension contributions earn the riskless interest rate:  $r=\beta

^{-1}-1=0.04$. If member k from the household i retires at age Rk in year t, its accumulated pension becomes a monthly annuity for their life,

$r=\beta

^{-1}-1=0.04$. If member k from the household i retires at age Rk in year t, its accumulated pension becomes a monthly annuity for their life,  $\tilde{p}a_{k,t^{\ast }}(R_{k})=\dfrac{rPWI_{k,t^{\ast }}}{1-(1/\beta

)^{-12\times (T_{k,t}-R_{k})}}$.

$\tilde{p}a_{k,t^{\ast }}(R_{k})=\dfrac{rPWI_{k,t^{\ast }}}{1-(1/\beta

)^{-12\times (T_{k,t}-R_{k})}}$.

Let  $pw_{k,i,t=2020}^{d=1}$,

$pw_{k,i,t=2020}^{d=1}$,  $pw_{k,i,t=2020}^{d=2}$, and

$pw_{k,i,t=2020}^{d=2}$, and  $pw_{k,i,t=2021}^{d=3}$ denote the amount of the first, second, and third pension withdrawals, respectively. Let

$pw_{k,i,t=2021}^{d=3}$ denote the amount of the first, second, and third pension withdrawals, respectively. Let  $PWI_{k,t=2020}^{d=1}=PWI_{k,t=2020}$,

$PWI_{k,t=2020}^{d=1}=PWI_{k,t=2020}$,  $PWI_{k,t=2020}^{d=2}=PWI_{k,t=2020}-pw_{k,i}^{d=1}$ and

$PWI_{k,t=2020}^{d=2}=PWI_{k,t=2020}-pw_{k,i}^{d=1}$ and  $PWI_{k,t=2021}^{d=3}=PWI_{k,t=2021}-pw_{k,i}^{d=1}-pw_{k,i}^{d=2}$ denote the contributory wealth of worker k from household i before the first, second, and third pension withdrawal.

$PWI_{k,t=2021}^{d=3}=PWI_{k,t=2021}-pw_{k,i}^{d=1}-pw_{k,i}^{d=2}$ denote the contributory wealth of worker k from household i before the first, second, and third pension withdrawal.

The counterfactual pension wealth in 2021 corresponds to the value of 2020 plus an additional year of contributions:  $PWI_{k,t=2021}=PWI_{k,t=2020}+cr\min

(mc,P_{k,t=2021})pc_{k,t=2021}$. The value of each pension withdrawal is given by

$PWI_{k,t=2021}=PWI_{k,t=2020}+cr\min

(mc,P_{k,t=2021})pc_{k,t=2021}$. The value of each pension withdrawal is given by  $pw_{k,i,t}^{d}=\min (PWI_{k,t}^{d},35UF)1(PWI_{k,t}^{d}\leq 35UF)$ +

$pw_{k,i,t}^{d}=\min (PWI_{k,t}^{d},35UF)1(PWI_{k,t}^{d}\leq 35UF)$ +  $35UF\times 1(35UF \lt PWI_{k,t}^{d}\leq 350UF)$ +

$35UF\times 1(35UF \lt PWI_{k,t}^{d}\leq 350UF)$ +  $0.10\times

1(350UF \lt PWI_{k,t}^{d}\leq 1500UF)$ +

$0.10\times

1(350UF \lt PWI_{k,t}^{d}\leq 1500UF)$ +  $150UF\times 1(PWI_{k,t}^{d} \gt 1500UF)$. The accumulated contributory pension wealth of worker k (

$150UF\times 1(PWI_{k,t}^{d} \gt 1500UF)$. The accumulated contributory pension wealth of worker k ( $PWI_{k,t}^{d=1+2+3}$) and household i (

$PWI_{k,t}^{d=1+2+3}$) and household i ( $PW_{i,t}$) after the three withdrawals is given by

$PW_{i,t}$) after the three withdrawals is given by

\begin{align}

PW_{i,t}=\sum\nolimits_{k}PWI_{k,t}^{d=1+2+3},

\end{align}

\begin{align}

PW_{i,t}=\sum\nolimits_{k}PWI_{k,t}^{d=1+2+3},

\end{align} with  $PWI_{k,t}^{d=1+2+3}=PWI_{k,t}-pw_{k,i,2020}^{d=1}-pw_{k,i,2020}^{d=2}-pw_{k,i,2021}^{d=3}$.

$PWI_{k,t}^{d=1+2+3}=PWI_{k,t}-pw_{k,i,2020}^{d=1}-pw_{k,i,2020}^{d=2}-pw_{k,i,2021}^{d=3}$.

The expected contributory pension value of each worker k after the three pension withdrawals is

\begin{align*}

\tilde{p}a_{k,t^{\ast }}^{d=1+2+3}(R_{k})=\dfrac{rPWI_{k,t^{\ast }}^{d=1+2+3}}{1-(1/\beta )^{-12\times (T_{k,t}-R_{k})}}.

\end{align*}

\begin{align*}

\tilde{p}a_{k,t^{\ast }}^{d=1+2+3}(R_{k})=\dfrac{rPWI_{k,t^{\ast }}^{d=1+2+3}}{1-(1/\beta )^{-12\times (T_{k,t}-R_{k})}}.

\end{align*}4.4. Non-contributory benefits

The minimum pension established prior to the withdrawals, in December 2019, following the social upheaval (see Section 2), was set at 5.99 UF for any retired member aged 65 years or older belonging to households within the three lowest income quintiles. However, due to government budget constraints, its implementation was gradual, and by 2022, it fully applied to all eligible retirees. Additionally, in 2022, the Pensión Garantizada Universal (PGU) was introduced, a universally guaranteed pension aimed at retirees in households within the lowest 90% of the income distribution, providing near-universal coverage. The monthly PGU amount is 5.93 UF for retirees with pensions below 20.18 UF and decreases linearly until it reaches zero for pensions at or above 32.04 UF.

For analytical purposes, this study compares the retirement income under the 2019 and 2022 policies over the period 2022–2055. Under the 2019 law, all retirees aged 65 years or older receive non-contributory (“solidarity”) benefits expressed as:  $B_{k,t}^{2019} = SB_{i}^{2019} \max \left( a_{1} - \tilde{p}a_{k,t}(R_{k}), B(\tilde{p}a_{k,t}(R_{k}))\right)\!,$ where

$B_{k,t}^{2019} = SB_{i}^{2019} \max \left( a_{1} - \tilde{p}a_{k,t}(R_{k}), B(\tilde{p}a_{k,t}(R_{k}))\right)\!,$ where  $a_{1} = 6.61 \, \text{UF}$,

$a_{1} = 6.61 \, \text{UF}$,  $SB_{i}^{2019}$ is a dummy for households within the lowest three income quintiles, and

$SB_{i}^{2019}$ is a dummy for households within the lowest three income quintiles, and  $ B(\tilde{p}a_{k,t}(R_{k}))$ represents the solidarity scheme in place before 2019. The pre-2019 scheme provided a basic pension (

$ B(\tilde{p}a_{k,t}(R_{k}))$ represents the solidarity scheme in place before 2019. The pre-2019 scheme provided a basic pension ( $ BP = 3.88 \, \text{UF}$), reduced at a rate of

$ BP = 3.88 \, \text{UF}$), reduced at a rate of  $ \frac{BP}{MP}$ until reaching a maximum pension (

$ \frac{BP}{MP}$ until reaching a maximum pension ( $ MP = 12.62 \, \text{UF}$):

$ MP = 12.62 \, \text{UF}$):  $pa_{k,t}(R_{k}) = \tilde{p}a_{k,t}(R_{k}) + B(\tilde{p}a_{k,t}(R_{k})),$ where:

$pa_{k,t}(R_{k}) = \tilde{p}a_{k,t}(R_{k}) + B(\tilde{p}a_{k,t}(R_{k})),$ where: $B(\tilde{p}a_{k,t}(R_{k})) = \left( BP - \frac{BP}{MP} \tilde{p}a_{k,t}(R_{k}) \right) \times 1(MP \gt \tilde{p}a_{k,t}(R_{k})).$

$B(\tilde{p}a_{k,t}(R_{k})) = \left( BP - \frac{BP}{MP} \tilde{p}a_{k,t}(R_{k}) \right) \times 1(MP \gt \tilde{p}a_{k,t}(R_{k})).$

The PGU, implemented in 2022, introduced significant changes to the system by broadening coverage and increasing generosity compared to earlier non-contributory pension programs. Unlike previous programs that targeted only the poorest retirees, the PGU aimed for near-universal coverage. Prior to these reforms, non-contributory pensions, such as the program Pensiones Asistenciales Solidarias (PASIS) program created in 1975, covered only 6.8% of retirees by 1990 and 14.7% by 2000 (Gana, Reference Gana2002). The 2008 reform introduced the “basic solidarity pensions,” which applied to retirees in the lowest three income quintiles (Berstein, Reference Berstein2010).Footnote 20 Under the PGU, the new solidarity benefits for each retiree k are expressed as follows:

\begin{equation*}

B_{k,t}^{2022} = SB_{i}^{2022} \left( b_{1}1(\tilde{p}a_{k,t}(R_{k}) \leq b_{2}) + b_{1} \left( 1 - \frac{\tilde{p}a_{k,t}(R_{k}) - b_{2}}{b_{3} - b_{2}} \right) 1(b_{2} \lt \tilde{p}a_{k,t}(R_{k}) \lt b_{3}) \right),

\end{equation*}

\begin{equation*}

B_{k,t}^{2022} = SB_{i}^{2022} \left( b_{1}1(\tilde{p}a_{k,t}(R_{k}) \leq b_{2}) + b_{1} \left( 1 - \frac{\tilde{p}a_{k,t}(R_{k}) - b_{2}}{b_{3} - b_{2}} \right) 1(b_{2} \lt \tilde{p}a_{k,t}(R_{k}) \lt b_{3}) \right),

\end{equation*} where:  $b_{1} = 5.93 \, \text{UF}, \quad b_{2} = 20.18 \, \text{UF}, \quad b_{3} = 32.04 \, \text{UF}$, and

$b_{1} = 5.93 \, \text{UF}, \quad b_{2} = 20.18 \, \text{UF}, \quad b_{3} = 32.04 \, \text{UF}$, and  $ SB_{i}^{2022}$ is a dummy variable indicating whether household i is within the lowest nine deciles of income.

$ SB_{i}^{2022}$ is a dummy variable indicating whether household i is within the lowest nine deciles of income.

The loss in the contributory pensions of each worker k is therefore obtained as follows:

\begin{align}

Contributory\_Pension\_Loss_{k,t^{\ast }}=\dfrac{\tilde{p}a_{k,t^{\ast }}-

\tilde{p}a_{k,t^{\ast }}^{d=1+2+3}}{\tilde{p}a_{k,t^{\ast }}},

\end{align}

\begin{align}

Contributory\_Pension\_Loss_{k,t^{\ast }}=\dfrac{\tilde{p}a_{k,t^{\ast }}-

\tilde{p}a_{k,t^{\ast }}^{d=1+2+3}}{\tilde{p}a_{k,t^{\ast }}},

\end{align} with  $t^{\ast }=2022+65-S(t,k)$ denoting the year in which worker k reaches age 65 years and becomes eligible for solidarity benefits.

$t^{\ast }=2022+65-S(t,k)$ denoting the year in which worker k reaches age 65 years and becomes eligible for solidarity benefits.

The total pension value is equal to the sum of the contributory pension and solidarity transfers. The total pension income in the scenario before the pension withdrawals and the solidarity pension law of 2022 is expressed as  $tp_{k,t^{\ast }}=\tilde{p}a_{k,t^{\ast }}+B_{k,t^{\ast }}^{2019}$. After the pension withdrawals and the solidarity pension law of 2022, the new projected total pension income is obtained as

$tp_{k,t^{\ast }}=\tilde{p}a_{k,t^{\ast }}+B_{k,t^{\ast }}^{2019}$. After the pension withdrawals and the solidarity pension law of 2022, the new projected total pension income is obtained as  $tp_{k,t^{\ast}}^{d=1+2+3}=\tilde{p}a_{k,t^{\ast }}^{d=1+2+3}+B_{k,t^{\ast }}^{2022}$. The total pension income loss is, therefore, given by

$tp_{k,t^{\ast}}^{d=1+2+3}=\tilde{p}a_{k,t^{\ast }}^{d=1+2+3}+B_{k,t^{\ast }}^{2022}$. The total pension income loss is, therefore, given by

\begin{align}

Total\_Pension\_Loss_{k,t^{\ast }}=\dfrac{tp_{k,t^{\ast }}-tp_{k,t^{\ast

}}^{d=1+2+3}}{tp_{k,t^{\ast }}},

\end{align}

\begin{align}

Total\_Pension\_Loss_{k,t^{\ast }}=\dfrac{tp_{k,t^{\ast }}-tp_{k,t^{\ast

}}^{d=1+2+3}}{tp_{k,t^{\ast }}},

\end{align} with  $t^{\ast }=2022+65-S(t,k)$.Footnote 21

$t^{\ast }=2022+65-S(t,k)$.Footnote 21

4.5. Current retirees

Our analysis also covers the effects of pension withdrawals and the increase in non-contributory benefits on current retirees. The methodology for this group is easier because it does not require simulations on the future employment and income paths of the individuals. The EPF survey reports the pension income for each retiree,  $\tilde{p}a_{k,t}$. This income is taken to be the contributory pension income before either the 2019 or 2022 laws were implemented. The contributory pension wealth of each retiree is therefore calculated with an annuity formula based on their current age and the life expectancy in 2022, after reaching age 60 years (ECLAC, 2020):

$\tilde{p}a_{k,t}$. This income is taken to be the contributory pension income before either the 2019 or 2022 laws were implemented. The contributory pension wealth of each retiree is therefore calculated with an annuity formula based on their current age and the life expectancy in 2022, after reaching age 60 years (ECLAC, 2020):

\begin{align}

PWI_{k,t}=12\times \tilde{p}a_{k,t}\dfrac{1-(1/\beta )^{-12\times

(T_{k,t}-S(t,k))}}{r}.

\end{align}

\begin{align}

PWI_{k,t}=12\times \tilde{p}a_{k,t}\dfrac{1-(1/\beta )^{-12\times

(T_{k,t}-S(t,k))}}{r}.

\end{align}For retirees with a life annuity (about 53.4% of the retirees), it is assumed that they used all three withdrawals. Therefore, their post-withdrawal pension wealth is

\begin{align}

PWI_{k,t}^{d=1+2+3}=PWI_{k,t}-pw_{k,i,2020}^{d=1}-pw_{k,i,2020}^{d=2}-pw_{k,i,2021}^{d=3},

\end{align}

\begin{align}

PWI_{k,t}^{d=1+2+3}=PWI_{k,t}-pw_{k,i,2020}^{d=1}-pw_{k,i,2020}^{d=2}-pw_{k,i,2021}^{d=3},

\end{align} where again the withdrawal amount is given by  $pw_{k,i,t}^{d}=\min

(PWI_{k,t}^{d},35UF)1(PWI_{k,t}^{d}\leq 35UF)$ +

$pw_{k,i,t}^{d}=\min

(PWI_{k,t}^{d},35UF)1(PWI_{k,t}^{d}\leq 35UF)$ +  $35UF\times

1(35UF \lt PWI_{k,t}^{d}\leq 350UF)$ +

$35UF\times

1(35UF \lt PWI_{k,t}^{d}\leq 350UF)$ +  $0.10\times 1(350UF \lt PWI_{k,t}^{d}\leq

1500UF)$ +

$0.10\times 1(350UF \lt PWI_{k,t}^{d}\leq

1500UF)$ +  $150UF\times 1(PWI_{k,t}^{d} \gt 1500UF)$. For retirees under the programmed retirement modality (about 46.6% of the retirees), the law only allowed them to use the third withdrawal. Therefore, their post-withdrawal contributory wealth is still given by Equation 6, but under the assumption that

$150UF\times 1(PWI_{k,t}^{d} \gt 1500UF)$. For retirees under the programmed retirement modality (about 46.6% of the retirees), the law only allowed them to use the third withdrawal. Therefore, their post-withdrawal contributory wealth is still given by Equation 6, but under the assumption that  $pw_{k,i,2020}^{d=1}=pw_{k,i,2020}^{d=2}=0$.

$pw_{k,i,2020}^{d=1}=pw_{k,i,2020}^{d=2}=0$.

The expected contributory pension value of each retiree k after the three pension withdrawals is then

\begin{align}

\tilde{p}a_{k,t}^{d=1+2+3}=\dfrac{rPWI_{k,t}^{d=1+2+3}}{1-(1/\beta

)^{-12\times (T_{k,t}-S(t,k))}}.

\end{align}

\begin{align}

\tilde{p}a_{k,t}^{d=1+2+3}=\dfrac{rPWI_{k,t}^{d=1+2+3}}{1-(1/\beta

)^{-12\times (T_{k,t}-S(t,k))}}.

\end{align} Finally, the Contributory Pension Loss and the Total Pension Loss are still given by Equations 3 and 4, but specifying  $t^{\ast }=2022$.

$t^{\ast }=2022$.

The annuity values in Equation 5 and Equation 7 assume that the life expectancy is the same for all agents in the same sex-cohort,  $T_{k,t}$, as given by the United Nations projections (ECLAC, 2020). Therefore, there is no need for the application of survival probabilities sequentially after each year. This is consistent with the model simulated in Equation 1, which assumes that all agents live until retirement age and live exactly the number of periods given by the life expectancy of their sex and cohort (projections obtained from the (ECLAC, 2020)).

$T_{k,t}$, as given by the United Nations projections (ECLAC, 2020). Therefore, there is no need for the application of survival probabilities sequentially after each year. This is consistent with the model simulated in Equation 1, which assumes that all agents live until retirement age and live exactly the number of periods given by the life expectancy of their sex and cohort (projections obtained from the (ECLAC, 2020)).

4.6. Fiscal costs

Finally, the fiscal cost of the pension withdrawals and the 2022 solidarity law for the current adult generation is obtained in present value as a fraction of the total pension withdrawals:

\begin{align}

FC_{P}=\dfrac{\sum\nolimits_{k\in P}12\times (B_{k,t^{\ast

}}^{2022}-B_{k,t^{\ast }}^{2019})\dfrac{1-(1/\beta )^{-12\times

(T_{k,t}-R_{k})}}{r(1/\beta )^{R_{k}-S(t,k)}}}{\sum\nolimits_{k\in

P}pw_{k,i,2020}^{d=1}+pw_{k,i,2020}^{d=2}+pw_{k,i,2021}^{d=3}},

\end{align}

\begin{align}

FC_{P}=\dfrac{\sum\nolimits_{k\in P}12\times (B_{k,t^{\ast

}}^{2022}-B_{k,t^{\ast }}^{2019})\dfrac{1-(1/\beta )^{-12\times

(T_{k,t}-R_{k})}}{r(1/\beta )^{R_{k}-S(t,k)}}}{\sum\nolimits_{k\in

P}pw_{k,i,2020}^{d=1}+pw_{k,i,2020}^{d=2}+pw_{k,i,2021}^{d=3}},

\end{align} where for the population of current retirees, the calculation applies their current age, that is  $R_{k}=S(t,k)$ and

$R_{k}=S(t,k)$ and  $R_{k}-S(t,k)=0$. The fiscal cost is measured as an opportunity cost, not as a budget item, and therefore it deduces the payments that would have been made under the 2019 solidarity benefits formula. The population P can either be the population of all current workers (age 25–64 years), the current retirees (all aged 65 years and older, and some women between age 60 and 64 years), or all current affiliates (the sum of current workers and retirees).

$R_{k}-S(t,k)=0$. The fiscal cost is measured as an opportunity cost, not as a budget item, and therefore it deduces the payments that would have been made under the 2019 solidarity benefits formula. The population P can either be the population of all current workers (age 25–64 years), the current retirees (all aged 65 years and older, and some women between age 60 and 64 years), or all current affiliates (the sum of current workers and retirees).

It should be noted that this measure only corresponds to the fiscal costs of the government with the current generation of adults. The simulation does not consider the current people who are below age 25 years and who will become working adults in the future. It also does not consider the fiscal costs with the generations that will be born in the future.

Also, this formula is not evaluating the costs of the pension withdrawals in isolation. It is evaluating the increased costs implied by the scenario of the “2022 PGU law plus withdrawals” relative to a scenario with the “2019 law and no withdrawals.” Some retirees used the pension withdrawals, but will not be eligible for the universal guaranteed pension and therefore imply zero fiscal cost, which is accounted for in Equation 8. Some retirees only benefited from the universal guaranteed pension and did not use the pension withdrawals, but this is a small minority. According to (Fuentes et al., Reference Fuentes, Quintanilla, Rueda, Salvo, Herrera and Toledo2021), more than 90% of the social security affiliates (11 million affiliates among a total of 12.2 million) used at least one withdrawal. This segment of the population is accounted in the fiscal costs formula of Equation 8, but it corresponds to a small minority.Footnote 22 Therefore, as stated in Section 1 and at the beginning of this subsection, this result calculates the fiscal costs of the universal guaranteed pension plus the pension withdrawals as a joint combined policy.

The measure of fiscal costs proposed in Equation 8 uses both numerator and denominator based on the EFH survey dataset. Note that the denominator understates the total dimension of the pension withdrawals, since our matched dataset gives a total of 37,679 billions of pesos (instead of the official amount of 41,424 billions of pesos). This is due to the inclusion of only the urban population in the survey dataset and the match being conditional on the unemployment insurance fund. Since the numerator is also limited to the urban population, it makes sense that both numerator and denominator must be calculated using the simulated EFH survey data.

5. Losses in pension income under a no-reform scenario

This methodology allows us to associate the average value of the withdrawals according to the members’ characteristics with the households surveyed by the EFH. Furthermore, we calibrated a model of pension contributions over the entire life cycle to obtain the simulated impact of the withdrawal policies on retirement income.

We find that Chilean households face a loss in their expected pensions as a result of the withdrawals. Figure 6 shows the distribution of estimated losses in the contributory pension among the population of affiliates and families, compared to a scenario without pension withdrawals. Figure 7 displays the distribution of losses incurred by withdrawals in the total pension (contributory plus solidarity contributions) among affiliates and families.

Figure 6. Distribution of the loss (in percentage) in the contributory pensions.

Figure 7. Distribution of the loss (in percentage) in the total pensions.

The results indicate that households experience an expected loss of approximately 15% of their contributory pension at the median level (Figure 6) and 10% of their total pension (Figure 7). On average, there is a 21% loss in the contributory pension among the population of affiliates, with average values of 18% for men and 24% for women. The average losses in family pensions would be around 21%, with average values of 18.5% for families with male heads of household and 23% for families with female heads of household. As shown in Figure 8, losses in the contributory pension decrease as the income quintile rises, with average values of nearly 35% in the first quintile (the poorest) and decreasing to around 11% or 12% for the fifth quintile (corresponding to the wealthiest 20% of families).

Figure 8. Average loss in the contributory pension across income quintiles.

As shown in Figure 7, there is a substantial fraction of affiliates and households that were fully compensated from the pension withdrawals with the 2022 PGU legislation. Table 7 summarizes the fraction of affiliates that were fully compensated from the withdrawals, according to groups of sex, age, and education. It shows that all men above age 65 years and all women above age 60 years were fully compensated, whatever their education background. There are no affiliates below age 60 years (in the simulation from the survey sample) that will be fully compensated from the withdrawals, even with the 2022 legislation. In terms of education background, around 24% of the men and 40% of the women with secondary school or less will be fully compensated by the 2022 legislation. Affiliates with technical or college education are much less likely to be fully compensated, whether men or women. Less than 17% of the affiliates with college education or more were fully compensated by the loss of their contributory pensions.

Table 7. Fraction of affiliates that were fully compensated (or more) from the withdrawals by the 2022 legislation (% of affiliates in each group)

Note: The table shows the percentage of affiliates that were fully compensated from the withdrawals.

However, when looking at the total pension, it is easy to observe that the losses are more limited, being lower for women and the poorest individuals. The average loss in the total pension for affiliates is 8.3%, with figures of 8.6% for men and 8% for women, respectively. The average loss in households is 8.5%, with similar values for households with male or female heads. As shown in Figure 9, the losses increase with income, ranging from approximately 6% in the first quintile to around 11% in the fifth quintile.

Figure 9. Average loss in the total pension across income quintiles.

Table 8 presents a more complete picture of the simulated contributory and total pension losses from the withdrawals, according to sex, age, and education. For both men and women, the contributory pension loss falls with higher education levels, irrespective of the age group. Average contributory pension losses for men with elementary school are more than twice the losses of affiliates with post-graduate education. For women, average contributory pension losses for affiliates with secondary school or less are more than twice those of affiliates with college or post-graduate education. However, for total pension losses among men, it is affiliates with elementary school that have the lowest losses, while those with technical education show the highest losses. Among women, total pension losses are lowest for those with elementary and secondary school, while being highest for post-graduates. It is also noticeable that women experience the strongest contributory pension losses relative to men across any education group. However, lower educated women benefit more from the PGU. For the total pension income, women experience smaller losses than men in the elementary and secondary school groups. Women and men with technical education experience almost the same total pension losses. Interestingly, women with college and post-graduate education experience substantially larger losses than men in the same educational groups. Perhaps this last result can be explained by men having higher wages and regaining their pension balances more rapidly. For instance, Table 8 shows that women in these groups experience much larger contributory pension losses than men.

Table 8. Average difference (in %) between the pensions after the withdrawals and the 2022 law relative to the no withdrawals and legislation scenario

Note: For simplicity, the table omits the group of men above age 65 years and women above age 60 years, because those groups were fully compensated from the withdrawals (Table 7). However, those age groups are still included in the average statistics for the groups of “All men” and “All women.”

Figure 10 and Figure 11 present the average loss in the contributory and total pension for cohorts of affiliates and households (based on the retirement year of the household member who retires later) until 2055 for each income quintile. The loss in the contributory pension for the cohort retiring in 2022 is around 12% for the fifth quintile and reaches nearly 50% in the first income quintile. These losses gradually decrease until 2045 and then decline sharply. In terms of the total pension, all income quintiles experience a loss between 9% and 12% in 2022, which remains until 2040 and then declines sharply after 2045. Therefore, pension withdrawals will impact the income of retirees until the cohorts retiring in 2050 (which have a life expectancy of 84 and 89 years for men and women, respectively, according to projections by ECLAC for Chile in 2020).

Figure 10. Average loss in the household contributory pension across income quintiles and for the cohorts retiring in each year until 2055.

Figure 11. Average loss in the household total pension across income quintiles and for the cohorts retiring in each year until 2055.

6. Fiscal costs under different policy reforms

6.1. The 2025 Pension Reform

On January 15, 2025, after years of extensive debate, a pension reform proposal was formally submitted to the Chilean Congress. The proposal was the result of prolonged negotiations involving the Ministry of Finance, the Ministry of Labor and Social Security, and key opposition parties. Following these discussions, the reform was approved by Congress on January 29, 2025. It is worth noting that, for much of the period during which this article was written, significant uncertainty surrounded the submission and approval of the reform, given that five previous legislative attempts had failed to gain approval since 2015.

Although introduced earlier in Section 2, the key elements of the reform are re-examined here to support our analysis of fiscal costs under this reform and alternative scenarios. The approved reform mandates a gradual increase in employer contributions, totaling 6% over a period of 9–11 years. Of this, 4.5% is allocated directly to workers’ individual pension accounts, while an additional 1.5% is contributed indirectly through the newly created social security fund. The full implementation of the reform is expected to be completed by the end of 2034.Footnote 23

The reform also establishes a new social insurance, funded by an additional 1% increase in the contribution rate and the reallocation of current employer contributions to the Disability and Survival Insurance (SIS, currently set at 1.5%), effectively replacing the existing SIS. The new insurance aims to address pension gaps between men and women, while also covering disability and survival risks. This will provide a pension benefit of 0.5 UF for each year of contributions, up to a maximum of 2.5 UF. To qualify, women must have at least 13 years of contributions, while men must contribute for a minimum of 20 years. In particular, this benefit is temporary and is expected to be gradually phased out over a 10-year period starting in 2045. Additionally, the reform includes a 12.3% increase in the non-contributory benefits of the PGU. However, this increase is not incorporated into the simulations presented in this article. As a result, the fiscal costs of non-contributory pensions in Chile are likely to be higher than estimated in this paper, by the 12% increase in PGU.

Both the 6% increase in contributions to individual pension accounts and the 1% increase in contributions to the Social Insurance Fund will be made by employers as a fraction of workers’ earnings. As a result, Chile is expected to experience a steady-state increase in the overall contribution rate of 6%.Footnote 24 For the purposes of our calibration, we only include the 6% increase in contributions allocated to individual accounts. We do not simulate the benefits associated with the new Social Insurance Fund, as the full implementation details of this mechanism remain unclear.

Currently, there are no active discussions regarding changes to the retirement age for men and women. However, the Chilean Association of Pension Funds has proposed equalizing the retirement age for men and women to improve pension outcomes.Footnote 25 Their proposal also suggests raising the retirement age to 66 years or higher in response to increasing life expectancy. While this is not part of the current legislative debate, including a delayed retirement age as a potential policy option in our analysis offers valuable insights.

6.2. Fiscal burden reduction from possible pension reforms

To obtain a clear picture of the fiscal costs of the withdrawals, we simulate the EFH survey dataset under different assumptions for future pension reforms. The baseline scenario (shown in the previous section) assumes that there will be no additional changes in the pension policy. The computation of fiscal costs in this baseline assumes a risk-free rate of 4%. We also show how sensitive the results are to changes in the risk-free interest rate.