1. Introduction

Small and medium enterprises (SMEs) are important for development and economic growth. Data from the World Bank (2017) indicated that a great percentage of global business (approximately 90%) is concentrated in this sector, and that SMEs contribute to the creation and maintenance of employment (approximately 50%). In emerging countries, formal SMEs provide 40% of the national gross domestic product. In contrast, SMEs generate an elevated environmental footprint, and studies in the European context have demonstrated that this sector provides 60–70% of the industrial pollution in this region (OECD, 2018a, 2018b); specifically, SMEs in the manufacturing industries require green transformation for a large share of their global resource use, waste generation and contamination (OECD, 2013). These facts show the importance of analysing and implementing adequate strategies to improve environmental performance in this sector, emphasizing SMEs in developing countries to promote the adoption of clean technologies and processes.

In many emerging economies, the productivity and competitiveness gap between large firms and SMEs are especially great. For example, the global productivity gap amounts to about US$15 trillion equivalent on value added, or approximately 7% of global gross domestic product (Albaz, Dondi, Radi, & Schubert, Reference Albaz, Dondi, Radi and Schubert2020), which dictates the formulation and application of different public and private strategies that allow improving levels of productivity and competitiveness, strengthening quality of products, increasing value-added services and expanding into the local and other markets (OECD, 2018a, 2018b).

Around the world, many SMEs are implementing different sustainability strategies with the aim of optimizing environmental and social processes in parallel to other business areas and possibilities across strategic platforms. This could generate conflict with short-term financial objectives, taking into account that sustainability is a fundamental driver of the long-term success of the business (OpenSAP, 2014). Sustainability business models seek to produce profit by delivering products and/or services that directly and/or indirectly decrease the pressure on the (social) environment and job creation while still producing profits equal to or greater than conventional business models that are mainly focused on sales of goods and/or services. In the first stage, minor sustainable changes can be implemented, whereas radical changes imply the migration of a sustainability system (Bohnsack, Pinkse, & Kolk, Reference Bohnsack, Pinkse and Kolk2014; Chun & Lee, Reference Chun and Lee2013; Schaltegger, Lüdeke-Freund, & Hansen, Reference Schaltegger, Lüdeke-Freund and Hansen2011).

Sustainability business models imply the application of practices in every link of the value chain (Boons & Lüdeke-Freund, Reference Boons and Lüdeke-Freund2013): in supply chain management (sustainable logistics and cocreation); in customer services to preserve relationships with customers and stakeholders with responsibility for their production and consumption systems (consumer education models, product assistance, guarantee of security and transparency) and in finance, in which the costs and benefits should be equally distributed among the involved stakeholders as ethical and socially responsible practices. Moreover, the criteria that can follow the sustainable models according to Willard (Reference Willard2012) are the following: (1) radical resource productivity (reduce dependencies on natural resources), (2) investment in natural capital (restore, maintain and expand ecosystems to meet society and organization needs), (3) green redesign (implement closed-loop production systems where waste is reduced or treated as a resource), (4) service and flow economy (replace goods with services; lease products and solutions to customers and when they become obsolete, recycle or remanufacture the returned product) and (5) responsible consumption (to reduce the demand for products and thereby to reduce negative environmental impacts). These elements show the importance of analysing the practices and processes in SMEs to determine the level of application and potential migration to sustainability business models in emerging economies, taking into account internationalization, digitalization and sustainability lead innovation and new business processes in this sector. Such processes seek to increase sales in national and international markets as a strategy to guarantee the maintenance of business according to the requirements of stakeholders and the environment, which requires more research, especially in developing countries (Denicolai, Zucchella, & Magnani, Reference Denicolai, Zucchella and Magnani2021).

Moreover, the main constraints of SMEs are related to limited access to long-term and reasonable finance, low income, a lack of organizations for training and developing a skilled class of entrepreneurs and workers and inadequate policies to support economic and social promotion and advances in this sector (Herr & Nettekoven, Reference Herr and Nettekoven2017). In these economies, SMEs present an important opportunity to improve economic, social and sustainable development through adequate, proactive and effective package policies that promote (Curtis, Reference Curtis2016) business regulatory environments (tax legislation, property rights, employment law, labour rights and trade rules); improvements in infrastructure, finance and education; value chain programmes and social empowerment and inclusive economies (e.g. good working conditions and adequate salaries) and support innovation, new technologies and start-ups with specific programmes (e.g. subsidies for specific sectors or businesses, development banks).

SMEs have different challenges in promoting and achieving sustainable and equitable development. According to different studies such as Jayasundara et al. (Reference Jayasundara, Rajapakshe, Prasanna, Naradda, Sisira, Ekanayake and Abeyrathne2019), The Institute of Leadership and Management (2020), Sault (Reference Sault2021) and Generali SME EnterPRIZE (2021), these challenges are related to environmental change and change in the business environment and can be summarized as follows: (1) change management promoting inclusive and sustainable industrialization (capabilities of flexibility and adaptability analysing the trends and dynamics of products, markets and technologies to adapt the business for sustainable survival); (2) responsible and ethical business practices focusing on both supporting current growth and long-term sustainability (action plan and strategies to promote legal, ethical, social demand and philanthropic aspects in the enterprise); (3) quality products and services through the adoption of sustainable practices and integrating sustainability information into reporting cycles (adequate and appropriate product and services planning that include access to growth, technology decisions, training, financing, national awards and akin to multinational corporation); (4) balance of stakeholder needs (to define the shared vision, stakeholder management and strategic proactivity to determine the influence on the environmental sustainability of the enterprise); (5) efficient use of natural resources and environmental protection practices (action to reduce environmental problems, increase the longevity of natural resources and maintain ecological support systems through innovation and ecological and social performance) and (6) awareness, education, transfer of competencies and capacity building to strengthen sustainability (to engage in activities suitable to reach SMEs through multiple channels promoting innovation, technology transfer and digitalization). These challenges demonstrated the importance of promoting sustainability in SMEs as a strategy to promote growth and development in transition economies with adequate programmes and political instruments.

Another challenge for SMEs is the risks that require survival and resilience in national and global economies, although SMEs are less prepared to manage the risks. According to the World Economic Forum global risk report (2019) and Asgary, Ozdemir, and Ozyurek (Reference Asgary, Ozdemir and Ozyurek2020), the main risks for this sector are: (1) global economic risks, because during an economic crisis, these enterprises are more exposed because of weak cash flow and financial structures, tightened credit lines, a lack of resources and a lack of adequate skills to adopt or make effective strategic decisions; (2) global environmental and disaster risks, through aspects such as capital, labour, logistics and markets due to relative resource restrictions, less resiliency, not fully meeting standards and codes, a lack of necessary insurance, not carrying out risk assessments and often a lack of business continuity plans; (3) global geopolitical risks, which increase insurance, transaction, transportation and security costs for such companies and (4) global societal risks and global technological risks, such as data breaches, cybersecurity and intentional or accidental technological failures, which can disrupt or significantly damage the short- and long-term operation in this sector. These risks indicate that environmental sustainability is important to guarantee the growth and strength of SMEs, and appropriate strategies and measures must be developed for this sector to manage such risks.

Studies in SMEs have been developed from different perspectives, such as (1) the application of standards and environmental management in SMEs to decrease pollution indicates that these practices increase the quality of management, which support industrial and trade organizations in overcoming restrictions in this sector, such as a lack of time, finances and knowledge in the application of environmental tools using strategies such as networks, technological support and advice and consulting services, which implies that innovation processes, learning and managers' awareness of environmental and social performance are the major determinants for sustainability strategies in SMEs (Graafland & Smid, Reference Graafland and Smid2016; Roy & Thérin, Reference Roy and Thérin2008; Stewart & Gapp, Reference Stewart and Gapp2014). (2) SMEs are barriers to growth in developing countries, which can be due to internal or external factors such as access to financing, tax rates, competition, infrastructure, management skills, location, technology, corruption, regulations and political factors, which could all be used to develop adequate instruments to strengthen SMEs as key elements for poverty alleviation, job creation and economic growth (Gree & Thurnik, Reference Gree and Thurnik2003; Wang, Reference Wang2016). (3) Strategies and mechanisms for financial support in this sector (Hasan, Jackowicz, Kowalewski, & Kozłowski, Reference Hasan, Jackowicz, Kowalewski and Kozłowski2017; Kersten, Harms, Liket, & Maas, Reference Kersten, Harms, Liket and Maas2017; Wellalage & Fernandez, Reference Wellalage and Fernandez2019; World Bank, 2017), which includes advisory (diagnostics, implementation support, global advocacy and knowledge sharing of good practices) and lending services (SME Lines of Credit, Partial Credit Guarantee Schemes and Early Stage Innovation Finance), which further implies the importance of improving and expanding the strategies and financial mechanisms from banking or financial institutions to offer different possibilities through the spillover effects and improvements on employee-level competitiveness according to the requirements and level of the maturity of the enterprise. (4) The promotion of the sustainability and success of microenterprises depend on the economic, political and social environment, which represents essential support for decision making to stimulate investment and economic growth and generate opportunities in this sector (Chatterjee, DuttaGupta, & Upadhyay, Reference Chatterjee, DuttaGupta and Upadhyay2018). The main restrictions on the adaptation of sustainability practices in business are related to a lack of awareness among employees about the importance of sustainability and the benefits of sustainability practices, a lack of resources, the high initial capital cost of implementing sustainability measures, insufficient management skills, inadequate practices, a lack of information on how to implement sustainability and the interference between intended sustainability initiatives and other business initiatives (Álvarez-Jaramillo, Zartha-Sossa, & Orozco-Mendoza, Reference Álvarez-Jaramillo, Zartha-Sossa and Orozco-Mendoza2018; Costache, Dumitrascu, & Maniu, Reference Costache, Dumitrascu and Maniu2021; SKG, 2019). (5) The importance of technology and the digital economy in SMEs is a fundamental factor in market competitiveness that requires institutional capabilities to generate sustainable technological environments, to promote the availability of the latest technology by the shared economy in the sector, to create firm-level technology absorption and technology transfer, to increase energy efficiency and the transition to a low-carbon economy (Das, Kundu, & Bhattacharya, Reference Das, Kundu and Bhattacharya2020; Mukhoryanova, Kuleshova, Rusakova, & Mirgorodskaya, Reference Mukhoryanova, Kuleshova, Rusakova and Mirgorodskaya2021). These studies show the importance of SMEs as fundamental factors that drive development in these economies.

From this background, this study analyses the implementation of strategies to promote sustainable practices in 120 microenterprises in a transition economy such as Colombia, taking into account the limited studies related to possibilities in promoting environmental practices in this sector and the importance of this sector for the economy and transformation of the productivity process. The main contribution of this study is to define strategies and plans that could improve sustainability in micro, small and medium enterprises (MSMEs) in the emerging economy of Colombia, taking into account the results of an intervention project using different MSMEs and the results obtained as a baseline, which allows us to determine the importance of sustainability to improve management in this sector and to align these processes with environmental and quality protection, to guarantee economic growth, to create or maintain jobs and the possibilities of product exports, among other benefits.

This paper is structured as follows: Section 2 describes the main characteristics of SMEs in Colombia. Section 3 describes the methods, data and description of the intervention process in the microenterprises that participated in the project. Section 4 describes the main results of the project, particularly the success factors and lessons learned, including a discussion. The conclusions of the study are presented in Section 5.

2. SMEs in Colombia: the main trends and characteristics of this sector

Colombia is an economy based on an industry where MSMEs predominate. By definition, SMEs must have an annual income that is less than or equal to US$220,000 for manufacturing, US$305,000 for services and US$415,000 for the commerce sector (from Decree 957/2019). Various studies related to Colombian SMEs concur with the following characteristics (ANIF, 2021; Bogotá Chamber Commerce, 2020a, 2020b; Franco & Urbano, Reference Franco and Urbano2019; Galvez & Quiñones, Reference Galvez and Quiñones2019): the firms of this sector are diverse, ranging from companies of low productivity due to short commercial and productivity capacity that depend on domestic demand or specific customers, such companies are led by the strategic thinking of their founder, without innovative processes; they have adaptive capacity and resilience and they seek diversification and transformation, with little or no international vision, to fast-growing, dynamic, innovative and export-oriented medium-sized companies. Moreover, SMEs are fundamental to development and generation of employment and are the main agent of economic simulation.

The most recent available data on Colombian SMEs indicate that they are fundamental for economic growth. According to Confecamaras (2018) and OECD (2020), 1,532,290 formal companies were registered in the Single Business and Registry in 2017, where 92.7% were microenterprises and 6.7% were SMEs, comprising 99.4% of the business industries in Colombia. This sector provides approximately 67% of the country's employment and approximately 28% of the gross domestic product and uses 54% of the total credit portfolio (DANE, 2017; Superintendencia Financiera de Colombia, 2018).

The allocation of resources in SMEs during the first half of 2018, taking into account the OECD study (2020), was as follows: working capital, 63%; the consolidation of liabilities, 22%; the purchase or leasing of machinery, 11% and remodelling or adjustments, 9%.

The pandemic has affected this sector, generating changes and transformations for survival. A study by the Bogotá Chamber of Commerce (2020a, 2020b) indicated that, in general, 76% of SMEs had taken some action to transform or change their business; which includes identifying new opportunities (22%), to maintaining or finding consumers and clients (21%) and transforming production processes and redefining strategic objectives (13%). To maintain employment, this sector used the following actions: measures to reduce working hours (51.8%), measures to reduce the number of employees (15.9%), salary cuts (12.1%), early vacations (11%), increases in working hours for essential positions (9.3%), cost reductions (30%), postponement of investments (14%) and debt restructuring (17.1%). The entrepreneurs surveyed concurred on the importance of support from the public and private sectors for the reactivation, survival and viability of microenterprises and SMEs. It is fundamental to promote sustainability and reduce the environmental impact of these companies.

These facts show the importance of analysing possibilities to apply different strategies to improve and strengthen sustainability in microenterprises, considering their role in economic growth and development and their potential to promote employment, innovation and value-added exports which are key factors in productivity and competitiveness. For these reasons, this study analyses and evaluates the implementation of sustainability strategies in 120 Colombian microenterprises during the second half of 2020 and the first half of 2021.

3. Methods and description of the project

This study focuses on micro-small enterprises operating in the Bogotá region in Colombia. These firms are common and more vulnerable business types in cities. To classify a firm as a micro-small enterprise, we follow the criteria proposed by the Colombian Decree 957/2019. The current study considers only companies set up as formal legal entities through the Chamber of Commerce. This study was developed between October 2020 and May 2021 and includes the following stages.

3.1 First stage: postulation, selection and enrolment

The project began by determining the criteria for the selection of micro-small enterprises for participation in the intervention project (see Table 1) based on a database of micro-small enterprises registered in the Bogota Chamber of Commerce and selecting key variables to establish that enterprises could participate in the project, and determining key sectors, such as food, construction, chemical, health, tourism, leather, textile and fashion, due to their focus as micro-small enterprises, export potential, higher water and energy consumption and environmental impacts. With these results, an invitation is sent and a promotion campaign is developed with the aim that different enterprises are registered to participate in the project at no cost.

Table 1. Criteria for the selection of micro-small enterprises to participate in the intervention project

At this stage, approximately 310 microenterprises were considered and evaluated according to the established criteria by the team of consultants through a matrix that determined the viability of the company to participate in the project with quantitative and qualitative evidence, which allowed the selection of 140 microenterprises, with 122 enrolled in the project through a letter of commitment and an explanation of the intervention process, which generated a work plan for every company.

3.2 Second stage: sustainability diagnosis

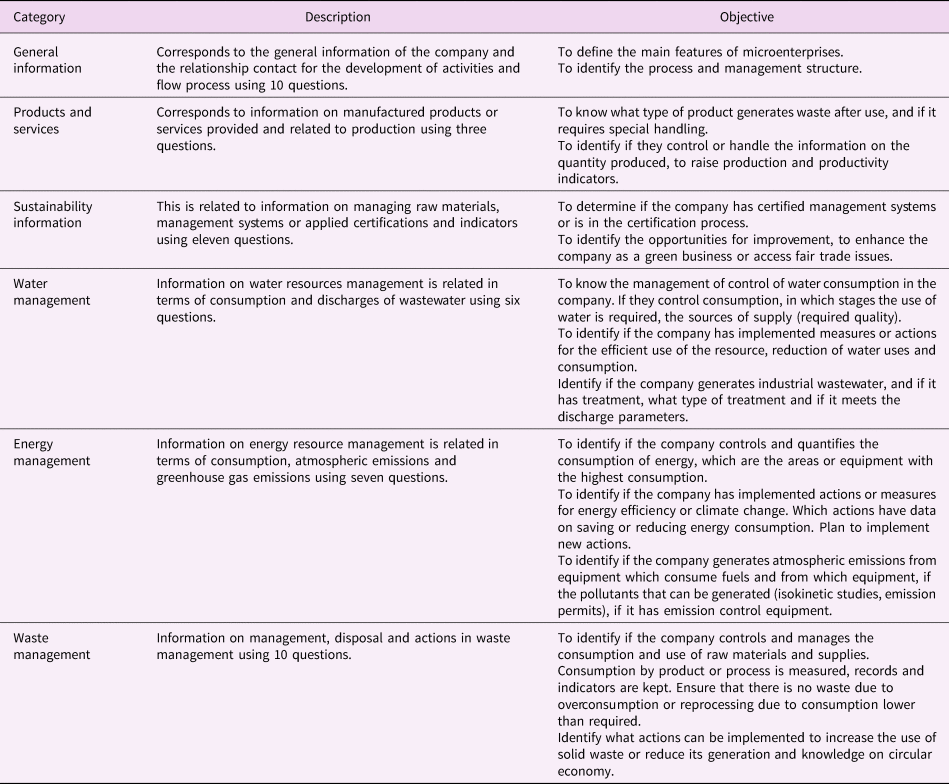

To develop this diagnosis, a template was structured and designed to capture and consolidate quantitative and qualitative information with six categories and a numerical evaluation (excellent, four points; good, three points; satisfactory, two points and unsatisfactory, one point). Table 2 shows the main features of the diagnostic instrument developed by the Environmental Business Corporation of the Chamber of Commerce.

Table 2. Criteria to select micro-small enterprises for participation in the intervention project

3.3 Third stage: action plan

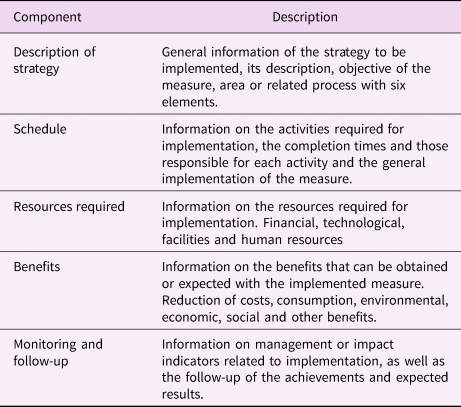

This stage identified and prioritized improvement opportunities. The microenterprises agreed on the implementation of improvement opportunities and goals. An indicator system for monitoring and follow-up was formulated. Table 3 describes the main components of the action plan.

Table 3. Description of the action plan

3.4 Fourth stage: results of implementation

According to the action plan measurements implemented in microenterprises, the implementation according to the action plan was followed up by monitoring progress towards meeting goals and developing different tools and techniques to implement sustainability strategies based on the requirements and priorities of the enterprises. In this stage, the company develops training plans, visits plants, measures different indicators, analyses processes and changes in infrastructure or techniques and documents processes, among other tasks.

3.5 Fifth stage: evaluation and feedback of results

This stage presents the results achieved by microenterprises through a project report sheet, displaying changes in indicators obtained through the intervention and recommendations to continue implementing sustainability strategies in the company. Moreover, in this stage, the results of 120 microenterprises were consolidated to evaluate and determine the improvements achieved, success factors and lessons learned from the project.

Quantitative, qualitative and mixed-method approaches (Maxwell, Reference Maxwell2016) were used in this research to analyse and evaluate sustainability strategies in microenterprises using categories established within the project to determine the main benefits and constraints for these companies to work with a sustainability approach.

4. Results

In this section, the results for every stage show that 120 microenterprises achieved improvements in sustainability performance related to raw materials, energy, water, technologies or processes, operations practices, waste management and emissions. Additionally, every microenterprise was aware of the importance of measuring and monitoring consumption and operational variables. Microenterprises appropriated tools that allowed them to automatically evaluate their processes, determine prices, select suppliers, implement technological changes that guarantee safe environments and prevent occupational diseases, taking into account legal compliance, showing their products and registering them as green and achieving circular economy strategies through symbiosis and connections between companies supporting foundations that work with vulnerable populations, which shows the importance of the project concept and the support that should be generated to microenterprises.

4.1 Results of the first stage: postulation, selection and enrolment

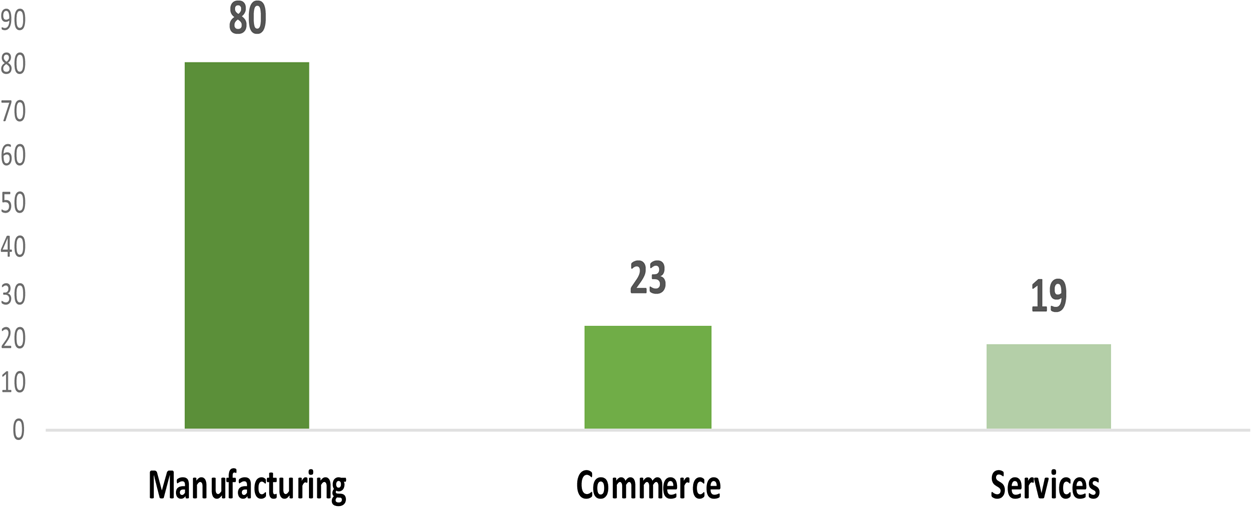

A total of 122 companies were enrolled and started the project; companies were distributed among the consulting teams. Each consultant has 20 companies engaged in intervention and generating sustainability improvement processes. The selected companies were from various productive sectors, taking into account the explained prioritization mechanism, where manufacturing predominated, followed by commerce and services (see Figure 1), with food and agro-industrial sector dominating, followed by textile, leather and fashion, chemical and plastic, construction, waste treatment and health sectors (see Figure 2). The main result of this stage was to attain a number of MSMEs of different sectors with interest in improving sustainability performance. The main lesson was the importance of increasing publicity campaigns to motivate participation in the project and engage responsible of entrepreneurs to achieve the expected results.

Fig. 1. Microenterprises that participated in the project by sector.

Fig. 2. Microenterprises by sector according to International Standard Industrial Classification of All Economic Activities (ISIC).

4.2 Results of the second stage: sustainability diagnosis

The general results of the diagnosis showed that the average score of the companies was 2.79/4, which corresponds to average performance (see Figure 3), which indicates that the participating microenterprises have begun to work on some sustainability issues, with the potential for improvements in environmental performance. The best scores were obtained for energy management and solid waste, and the lowest scores were obtained for energy management and sustainability.

Fig. 3. General results of diagnosis of 122 microenterprises.

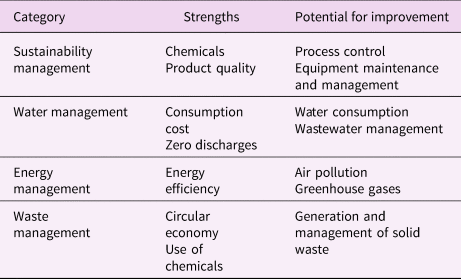

In general, the results show that the potential for improvement was in sustainability and environmental performance in matters of energy efficiency and waste management with a circular approach. Projects apply for tax exemptions for energy efficiency, certification in green businesses, the use of biomass for different uses, the saving and efficient use of water and energy, the gathering of environmental indicators and support in environmental issues related to INVIMA and the control of discharges and a maintenance programme for equipment and machines to monitor critical variables of the process. In addition, a common factor observed in most companies was that they did not have the business approach of designing, implementing and monitoring indicators, which makes it difficult to implement improvement options, process control, cost quantification and the application for environmental certifications. Table 4 shows a synthesis of the results of the diagnosis of the 122 companies in terms of their strengths and potential for improvement in each established category.

Table 4. Synthesis of the results of the 122 microenterprises based on strengths and potential for improvement

Regarding the scores obtained in the diagnosis of the 122 companies, 76 companies had an average score, and 36 had a good score in sustainability issues. In water resource management, 65 companies had a good score, and 47 had an average score. In energy resource management, 82 companies showed an average score, and 20 had a good score. In raw material and waste management, 62 companies had an average score, and 55 companies had a good score. These results show that the majority of companies in the four categories of analysis had an average score, followed by a good score and, to a lesser extent, a bad score (in this case, only one or two companies were identified).

These results allowed us to design action plans and establish the potential for these microenterprises to improve sustainability performance. Moreover, when comparing the productive sectors of the 122 companies, no marked differences were found; the sectors showed similar behaviours and ratings that were mainly concentrated in fair and good scores. However, it is important to review the action plans because they require considering the requirements of the productive sector based on the characteristics of its process or specific legal requirements.

The main results in this stage indicated that companies have possibilities to improve sustainability from soft to tough measures especially in energy and sustainability issues. The entrepreneurs strive to evaluate sustainability performance with an understanding of the process and business activities. The main lesson, in this stage, demonstrated the importance of understanding the business from a sustainability standpoint and quantify the performance criteria with key indicators to establish gaps and improvement possibilities.

4.3 Results of the third stage: action plan

With the results of the diagnoses of each of the microenterprises, the action plans to be implemented in each of the 122 selected companies were defined, and were discussed with and approved by the companies, formulating a total of 242 action plans. Figure 4 shows the plans to be implemented in the companies according to the sustainability categories established for the project.

Fig. 4. Action plans formulated in microenterprises by category.

The action plans that predominated the list of microenterprises were those of good practices (85%), followed by regulations (10%) and technological changes (5%), which was mainly due to the limited resources of the microenterprises. The implication is that designing actions that allow managing environmental and sustainability performance with the resources they have contributes comprehensively to microenterprises. These actions raise awareness and allow preparation for measures that require greater investments and actions in the medium and long term, which in many cases was recommended to microenterprises, and guidelines were left for potential possibilities of accessing financing and/or generating an awareness of the importance of evaluating sustainability in future projects to guarantee decision-making that contributes comprehensively to microenterprises.

The formulation of action plans was carried out based on the issues resulting from the diagnosis that allow improving business sustainability. In many cases their implementation began, but to continue, it was necessary to have financing mechanisms due to changes or adaptations of infrastructure, technology improvements and equipment, human resources, the acquisition of renewable energy systems and investments in procedures, among others, showing the importance of having financing, so that these microenterprises can achieve these acquisitions or adopt changes in favour of productivity and sustainability. Table 5 shows the action plans formulated for the microenterprises according to the established sustainability categories and the range of estimated budgets to achieve the expected results in the medium and long term, which were defined by every enterprise according to possibilities and recommendations of the consultants. This took place by prioritizing investments of low prices such as installation of water saving systems, changing the illumination by led technology, training activities, demarcation of areas, systems of collection and storage of solid waste according to Colombian regulations, documentation of process, monitoring, control and measurement of sustainability variables, among others. The application and implementation of the action plan was financed by every firm, taking into account that the project only included the advisory to develop diagnosis, implementation of the action plan and recommendations, training, follow-up of the implementation, selection and application of indicator systems and evaluation. However, the projects achieved agreements with governmental agencies to explain the different scenarios of financing with preferences related to amount, time and interest rates specially to implement renewable energy, cleaner technologies, changes in process and infrastructure, requirements to export, among others.

Table 5. Synthesis of the results of the microenterprises based on strengths and potential for improvement

The formulation and development of these action plans allowed the microentrepreneurs to know how to improve their processes; to define strategies that included technical, environmental and economic performance; to be able to analyse new possibilities to manage their processes in a more environmentally friendly way; to develop operational controls to improve performance standards and results; to make decisions regarding their purchases and selection of suppliers and to demonstrate the environmental and sustainability advantages of their products and services. These elements made it easier for these 122 microenterprises to continue working on the environmental issues and strengthen their actions to continue improving the sustainability of their businesses with soft and hard measures, generating a culture of measurement that allows us to demonstrate how different actions can achieve economic benefits while caring for the environment.

The main result of the third stage achieved that these entrepreneurs developed sustainability projects observing before and after improvements indicators and performance understanding of the benefits of integrating the environment and sustainability in the process. The main lesson, especially for developers of projects, showed the importance of joining these initiatives with specific financing programmes that promote the sustainability performance of easy and fast access.

4.4 Fourth stage: results of implementation

The intervention process had different stages according to the characteristics of the action plan where characterizations of equipment stand out, the capture of information on consumption and costs, diagnoses of health records, talks with the company's employees, improvement of exploring environmental issues, infrastructure and equipment improvements, legal compliance, micro measurements, waste inventory, etc. By category, the results are shown in Table 6.

Table 6. Main results by category

The main result of fourth stage indicated that companies achieved improvements in sustainability performance from different approaches saving resources and decreasing environmental impacts. The main lesson is that the interests of MSMEs to achieve sustainability as a strategy to increase market share and gain new consumers and the importance of compliance to environmental law or to access of different sustainability certifications.

4.5 Fifth stage: evaluation and feedback of results

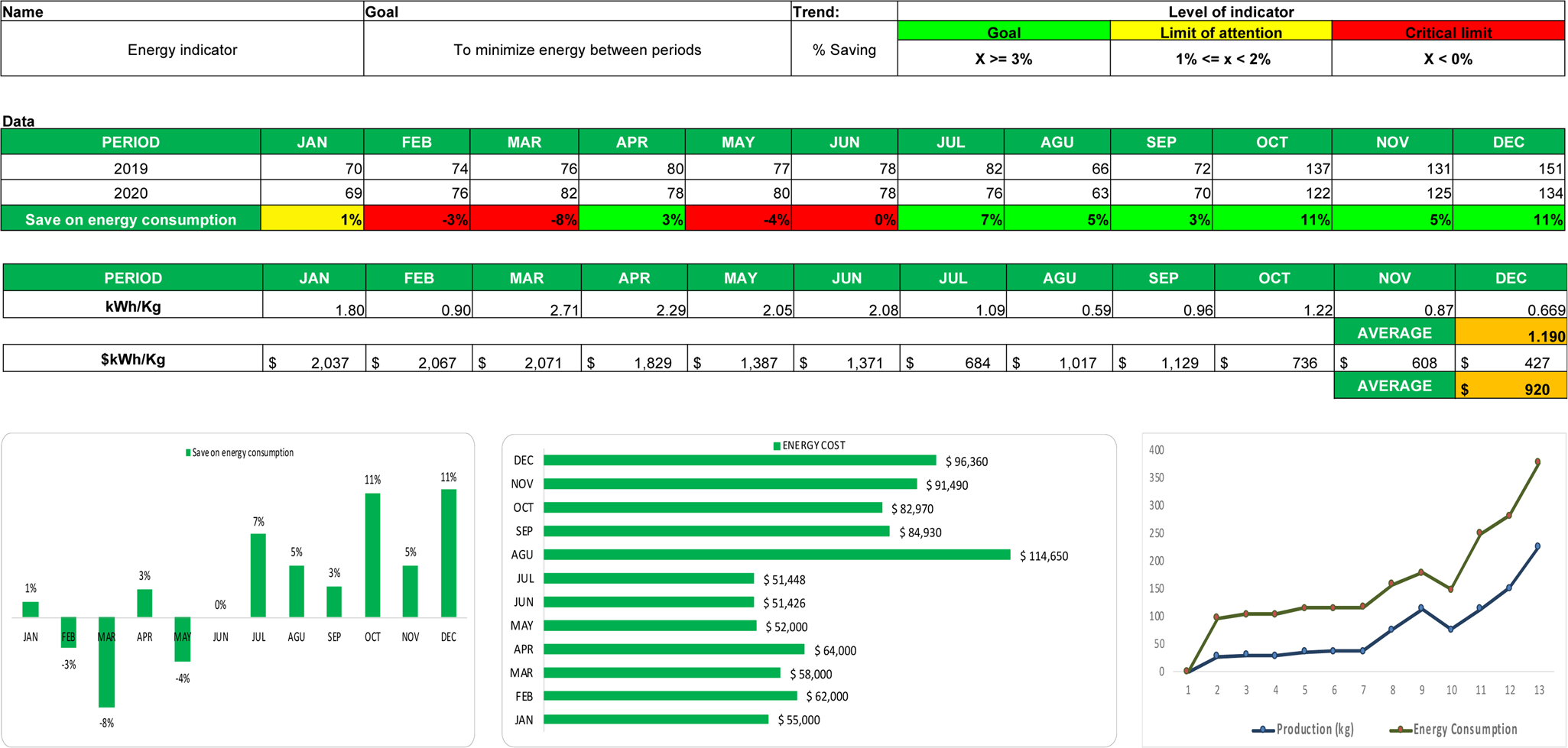

Regarding sustainability issues, the results and improvements in the intervened microenterprises were generated by the application of the indicator tool in Excel which included monthly measurements for every component (water, energy and waste) including consumption and costs of resources, value of production (physical or monetary), normalization of consumption or costs by production, indications on achieving the goal, calculation of baseline and comparison between periods and alerts. Figure 5 shows examples of the application of the indicator tool.

Fig. 5. Examples of the application of the indicator tool in every firm.

The indicator tool was implemented by 65 of the microenterprises that participated in the programme, which is equivalent to 53% with positive results, since the tool evidenced equilibrium point in production, strategies to pay for the product, planned changes in equipment with the respective impacts on reducing consumption and costs and the importance of installed capacity to reduce consumption and costs, taking advantage of economies of scale.

In microenterprises that worked on the management of water resources, different results can be highlighted: the savings of water resources in consumption and costs were estimated to range from 1 to 6% based on good practices and preventive maintenance; a water-saving filter was installed in the process of washing, representing savings of approximately 56% in this process; the microenterprises that installed water-saving devices in their hydraulic facilities are expected to save between 15 and 20% with a return on investment over a period of 6 months on average and the microenterprises that installed rainwater collectors are estimated to save up to 40% in the consumption of water resources.

Based on the interventions, these examples can be highlighted compared to the quantitative improvements in energy resource management that were achieved from the 34 plans implemented in the intervened microenterprises: installation of pipelines to control the emission of particulate matter and/or emissions, improving working conditions for employees by reducing these emissions and their possible health effects by approximately 30–50%. Savings in energy resources of 3% in approximately 10% of the intervention companies and 4% in fuels, and two companies in the brick sector analysed the viability of accessing tax incentives.

In the case of the integral management of solid waste, 52 action plans were implemented in the intervening microenterprises; on average, the monthly production of waste was an average of 30.1 kg per month, of which 38% corresponded to hazardous waste. Examples of the main achievements on the issue of waste management in companies through the action plans implemented during the intervention are as follows: of the 100% of the total waste generated, an average of 25–80% was recycled, managed and/or recovered adequately in several of the companies, with a representative value of 55%, and 35% of the microenterprises implemented the new colour code for separation at the source of solid waste regulated by Resolution 2184 of 2019, thus strengthening the waste management of each of the companies that developed a plan of action focused on optimizing solid waste.

The main result of this stage indicated that it is possible that MSMEs can use sophisticated and effective tools to monitor sustainability and understand risks or changes of performance and to take decisions through alerts and adopt a prevention perspective. The main lesson indicated the importance of empowering this sector on sustainability issues to achieve a multiplication effect in the value chain, which increased social and environmental responsibility through results and evidence.

In this stage, 122 companies were analysed in every category. The actions with higher effect in the score of sustainability using a dynamic panel model with results obtained in the end evaluation in every company were used to determine the topics with a higher intervention impact. The model used for this purpose is the estimator of the generalized method of moments of dynamic panel data developed by Arellano and Bover (Reference Arellano and Bover1995) and Blundell and Bond (Reference Blundell and Bond1998). This method estimates a difference regression equation and a level regression equation simultaneously, with a specific set of instrumental variables used in each regression. For the sustainability model, a balanced panel is estimated with the following functional form:

Note that Sit is the level of sustainability obtained in period t for firm i; Sit −λ is the lagged coefficient of the level of sustainability; PMit is the product management; MCSit is the management of chemical substances of the firms; ECit are the potential environmental certifications of the companies; CPit is the control process of the different companies; QPit is the quality of products; MMEit is the maintenance and management equipment and STit is the sustainability trade in period t for company i.

Regarding sustainability, the results indicated (see Table 7) that companies with higher sustainability have a significant direct relationship with product management, environmental certifications, the control process, the quality of products, maintenance and management equipment, sustainability trade and the management of chemical substances, which demonstrated the importance of integral management to achieve sustainability with adequate plans and strategies as developed in this project.

Table 7. Results of sustainability in the 122 companies

Notes: Figures in parentheses are the standard errors: *significant at the 10% level, **significant at the 5% level and ***significant at the 1% level.

For the water management model, the estimated structure is as follows:

Note that WMit is the water management in period t for firm i; WMit −λ is the lagged coefficient of water management; WEPit is water efficiency practices and ZWWDit is the zero wastewater discharges in period t for company i.

For water management (see Table 8), the main important interventions are related to the application of water efficiency practices and possibilities to significantly achieve zero wastewater discharges. These plans were developed through good practices from sources and in every process, indicating the importance of understanding the process and defining pollution sources to determine changes or best actions to control consumption and discharges, generating positive environmental and sustainability results in the companies that worked water action plans.

Table 8. Results of water management in the 122 companies that intervened

Notes: Figures in parentheses are the standard errors: *significant at the 10% level, **significant at the 5% level and ***significant at the 1% level.

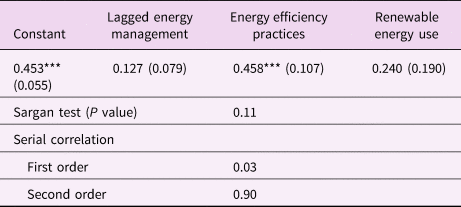

For the energy management model, the functional form is as follows:

Note that EMit is the energy management in period t for firm i; EMit −λ is the lagged coefficient of energy management; EEPit is the energy management and REUit is the renewable energy use in period t for company i.

For energy management (see Table 9), the measures that achieved adequate results were energy efficiency practices and renewable energy use, demonstrating the importance of soft and strong measures to improve energy use. Renewable energy was not significant, indicating that these processes require investments and changes in the companies. However, in the medium and long run, this will be a requirement for the companies.

Table 9. Results of energy management in the 122 companies that intervened

Notes: Figures in parentheses are the standard errors: *significant at the 10% level, **significant at the 5% level and ***significant at the 1% level.

For the solid waste management model, the estimated structure is as follows:

Now note that SWMit is the solid waste management in period t for firm i; SWMit −λ is the lagged coefficient of solid waste management; GSWit is the decreased generation of solid waste; CDSWit is the cost of disposal of solid waste; WMPit is the waste management practices and CEit is the circular economy in period t for company i.

For solid waste management (see Table 10), the main practices to improve sustainability are related to a decrease in the generation of solid waste, a higher cost of solid waste disposition and the application of better waste management and circular economy practices to improve sustainability, which implies that companies should include adequate management practices and plan changes in technologies and processes from environmental perspectives to achieve sustainability, decrease waste, improve processes and decrease costs, among others.

Table 10. Results of solid waste management in the 122 companies that intervened

Notes: Figures in parentheses are the standard errors: *significant at the 10% level, **significant at the 5% level and ***significant at the 1% level.

These results indicated that in the different categories of sustainability it is important to promote adequate practices at the source, and that entrepreneurs understand the advantages of cleaner production practices as strategy to improve process, increase customers, reduce costs and guarantee quality of products.

5. Discussion

This project demonstrated the importance of informing the development of an adequate instrument to promote sustainability awareness in microenterprises, which concurs with various studies that indicated that a lower level of sustainability awareness could be considered the main bottleneck. This is the first step because its impacts will not only directly generate a change in practices or processes, but could also support the inclusion of new processes and strategies in the long term to decrease environmental impacts, taking into account the constraints related to direct subsidies or free technical assistance that could be based on a fee-based system for technical assistance to achieve green business (Defra, 2011; OECD, 2015).

The project determined that microenterprises have an interest in sustainability as a strategy to improve processes and business through different projects that increase quality, efficiency and competitiveness, which concurs with GRI (2020), who determined that sustainability in SMEs as a factor for business success is a crucial aspect of competitiveness and market access. In transition economies, it contributes to more sustainable development and the reduction of poverty, which is also dependent on legal certainty, a healthy environment, peaceful conditions and good human relationships within a microenterprise and its conditions. This last point was a success factor in this intervention because microenterprises knew and evaluated their process from an integral perspective of sustainability. The continuous improvement of the process obtained multiple benefits, such as higher productivity and competitiveness and reduction of costs and possibilities to open new markets.

Further to the four components, was the standardization and measurements of the process in every intervened microenterprise, which generated advantages in the organizations (European Commission, 2012): (1) improvements to the quality of the product or service provided (increasing customer satisfaction and attracting new customers); (2) increased capability to validate the quality of products or services and environmental performance; (3) increased confidence in the business and its products or services (demonstrating a commitment to quality, safety and reliability); (4) improvements to company image; (5) the ability to cooperate and trade using a common ‘language’ (the codification of knowledge can help businesses cooperate, create strategic alliances and trade efficiently); (6) improved ability to trade across borders and exports (export strategy can create new business opportunities and increased sales, with reduced trading costs); (7) improved ability to meet legislative and regulatory requirements; (8) improved internal risk management and planning (to improve their business processes, implement best practices and monitor their progress and results in a structured way); (9) reduced costs (more efficient activities and better management that drive profitability) (10) increased competitiveness, which was demonstrated in the microenterprises of the project.

The findings of this study are important for understanding the best strategies and programmes to improve sustainability in microenterprises, as it is an important sector to decrease poverty and guarantee new opportunities in different sectors of the economy. Governments and policymakers could perform the following actions: enhance the conversion of informal entrepreneurship into formal businesses; provide growth and innovation support, address bottlenecks in skills, formulate policy responses related to a selection of business support instruments, provide financial incentives for sustainable economic opportunities, adopt local purchasing and procurement schemes aimed at SMEs and create new partnership funds and schemes, among others, which require SME education and training, better legislation and regulation, the availability of skills, improving limited access, taxation and financial matters, strengthening the technological capacity, successful e-business and sustainability models and top-class business support and developing a stronger, more effective representation of small enterprises (OECD, 2009).

6. Conclusions

This intervention project with 120 microenterprises allowed each microenterprise to demonstrate different actions that it could take regarding environmental sustainability and how this could generate other benefits for its processes and product, improving its competitiveness and productivity, culminating in a successful project with 116 microenterprises in each of the stages and with results of improvement in sustainability and the environment.

The action plans implemented by each of the microenterprises made it possible to demonstrate the importance of taking into account key elements of sustainability in decision-making, which allows a comprehensive vision of all the benefits to be obtained when integral evaluations that balance all organizational factors in a company are carried out.

The microenterprises achieved fundamental changes in their processes on sustainability, water and energy management and waste-based measures of good practices, technological and regulatory change that achieved improvements in environmental performance and standardized processes from the perspectives of sustainability.

One of the main results obtained in this project is related to the creation of the sustainability indicators tool, which was successful in terms of the requirements of microentrepreneurs and the results of the project, since the consolidation, registration and documentation of consumption in the use of natural resources such as water and energy resources and the generation of solid waste allowed for more specific control and better planning of environmental decisions.

The project also achieved the consolidation of the indicators of each company and established what their savings were and, in some cases, what the consumption per unit of product was. It is expected that the 116 companies with interventions could continue using the tools they adopted and continue with the processes of continuous improvement in sustainability issues and be able to demonstrate their commitment to the environment and sustainability that increasingly demands products that protect the environment.

These types of programmes are important to promote sustainability in microenterprises through limited resources. They could help increase growth and development through green markets, applying strategies and improvement actions to decrease environmental problems and cleaner production; actions that are regularly not taken into account in the decisions of these businesses.

Acknowledgements

The authors thank Dra. Belsy Munive and consulting team and the Bogotá Chamber of Commerce Team for their helpful suggestions and comments during the development of this project.

Author contributions

Clara Inés Pardo Martínez: Conceived and designed the analysis, wrote the paper and performed the analysis. Alexander Cotte Poveda: Contributed to data or analysis tools and performed the analysis.

Financial support

This study was financed through contract No. LA/2019/407-735 signed by the European Commission and the Bogotá Chamber of Commerce.

Conflict of interest

We wish to confirm that there are no known conflicts of interest associated with this publication and that there has been no significant financial support for this work that could have influenced its outcome.

Research transparency and reproducibility

The authors confirm the research transparency and reproducibility according to the journal's policy.

Open access

Open access