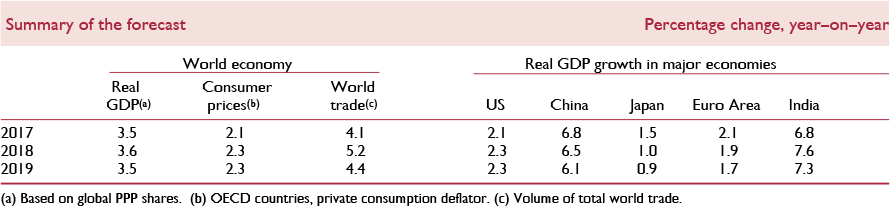

We continue to expect world GDP growth of about 3½ per cent this year, in 2018–19, and the medium term – a moderate acceleration from last year's 3.2 per cent growth, which was the weakest since the 2009 recession. No further improvement is in prospect: global growth this year and next seems likely to be as good as it gets. The 3½ per cent annual growth rate forecast for the medium term is below the 4.2 per cent a year average in the decade up to 2008.

Recent months have been characterised by unusually favourable global economic and financial developments, with generally robust growth, declining unemployment, subdued inflation (though still below targets in the major economies), broadly stable financial and foreign exchange markets, and buoyant stock markets.

An upside risk to our forecast in the short term is that recent favourable forces may gather momentum. But downside risks have not diminished, and while for the short term risks may be broadly balanced, for the medium term they seem tilted to the downside.

Downside risks may have been increased by recent market buoyancy. Some stock markets appear to have become even more richly valued, so the likelihood may have increased of market declines with negative economic repercussions. Markets are vulnerable to changes in sentiment and economic policy missteps.

In the United States, one risk is that monetary policy may need to be tightened more rapidly than assumed. Another is that persistently low inflation and interest rates could further increase leverage and stretch market valuations, exacerbating dangers of financial instability, and also reduce the Fed's capacity to reduce real interest rates in an economic downturn. Further risks arise from the unusually high current turnover on the Fed's Board.

With regard to US fiscal policy, the administration's plans to reduce taxes risk widening the deficit, further increasing public debt, and increasing demand pressures, which the Fed might need to counter by tightening monetary conditions. Another set of risks is associated with the possibility of a rollback of financial regulation and oversight. There also remain uncertainties about US trade policy: the risks of US-led protectionism remain.

In the Euro Area, there is a risk that stresses in the monetary union may become more challenging when the ECB starts raising interest rates, and risks arising from the lack of progress towards completion of the monetary union's institutional arrangements. There are also risks in China related to the high level of debt.