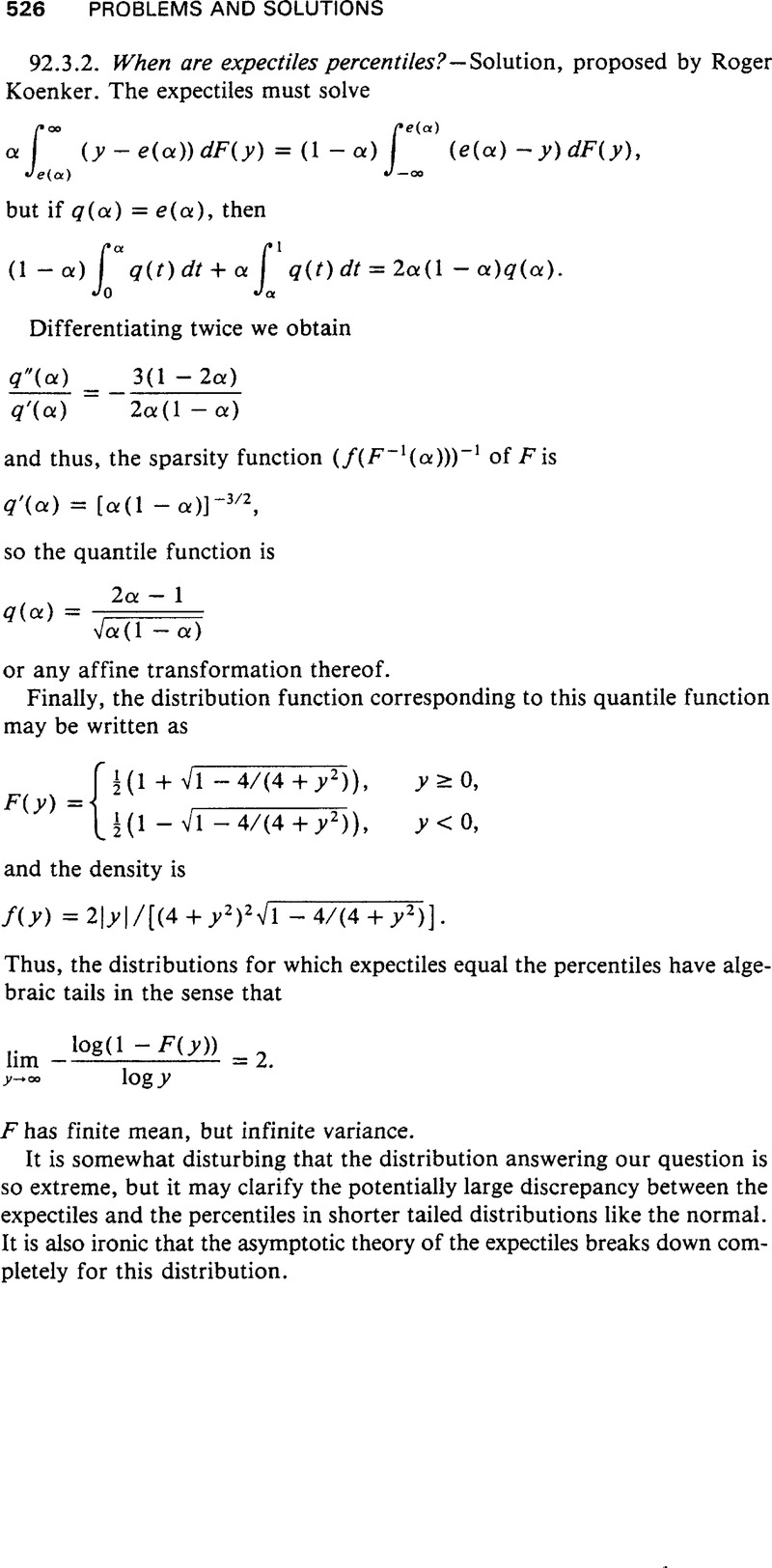

Crossref Citations

This article has been cited by the following publications. This list is generated based on data provided by Crossref.

Bellini, Fabio

Klar, Bernhard

Müller, Alfred

and

Rosazza Gianin, Emanuela

2013.

Generalized Quantiles as Risk Measures.

SSRN Electronic Journal,

Koenker, Roger

2013.

Discussion: Living beyond our means.

Statistical Modelling,

Vol. 13,

Issue. 4,

p.

323.

Bellini, Fabio

Klar, Bernhard

Müller, Alfred

and

Rosazza Gianin, Emanuela

2014.

Generalized quantiles as risk measures.

Insurance: Mathematics and Economics,

Vol. 54,

Issue. ,

p.

41.

Bellini, Fabio

and

Di Bernardino, Elena

2014.

Asymptotic Behaviour of High Expectiles.

SSRN Electronic Journal,

Zou, Hui

2014.

Generalizing Koenker's distribution.

Journal of Statistical Planning and Inference,

Vol. 148,

Issue. ,

p.

123.

Gschhpf, Philipp

2015.

TERES - Tail Event Risk Expectile Based Shortfall.

SSRN Electronic Journal ,

Yang, Yi

and

Zou, Hui

2015.

Nonparametric multiple expectile regression via ER-Boost.

Journal of Statistical Computation and Simulation,

Vol. 85,

Issue. 7,

p.

1442.

Bernardi, Mauro

Bignozzi, Valeria

and

Petrella, Lea

2017.

On theLp-quantiles for the Studenttdistribution.

Statistics & Probability Letters,

Vol. 128,

Issue. ,

p.

77.

Bellini, Fabio

and

Di Bernardino, Elena

2017.

Risk management with expectiles.

The European Journal of Finance,

Vol. 23,

Issue. 6,

p.

487.

Pipitpojanakarn, Varith

Maneejuk, Paravee

Yamaka, Worapon

and

Sriboonchitta, Songsak

2018.

Econometrics for Financial Applications.

Vol. 760,

Issue. ,

p.

859.

Chen, James Ming

2018.

On Exactitude in Financial Regulation: Value-at-Risk, Expected Shortfall, and Expectiles.

SSRN Electronic Journal,

Chen, James Ming

2018.

On Exactitude in Financial Regulation: Value-at-Risk, Expected Shortfall, and Expectiles.

Risks,

Vol. 6,

Issue. 2,

p.

61.

Tadese, Mekonnen

and

Drapeau, Samuel

2020.

Relative bound and asymptotic comparison of expectile with respect to expected shortfall.

Insurance: Mathematics and Economics,

Vol. 93,

Issue. ,

p.

387.

Mihoci, Andrija

Härdle, Wolfgang Karl

and

Chen, Cathy Yi-Hsuan

2021.

TERES: Tail Event Risk Expectile Shortfall.

Quantitative Finance,

Vol. 21,

Issue. 3,

p.

449.

Tadese, Mekonnen

and

Drapeau, Samuel

2021.

Dual representation of expectile-based expected shortfall and its properties.

Probability, Uncertainty and Quantitative Risk,

Vol. 6,

Issue. 2,

p.

99.

Bonaccolto, Giovanni

Caporin, Massimiliano

and

Maillet, Bertrand B.

2022.

Dynamic large financial networks via conditional expected shortfalls.

European Journal of Operational Research,

Vol. 298,

Issue. 1,

p.

322.

Arab, Idir

Lando, Tommaso

and

Oliveira, Paulo Eduardo

2022.

Comparison of Lp-quantiles and related skewness measures.

Statistics & Probability Letters,

Vol. 183,

Issue. ,

p.

109339.

Hutson, Alan D.

2024.

The generalized sigmoidal quantile function.

Communications in Statistics - Simulation and Computation,

Vol. 53,

Issue. 2,

p.

799.

Daouia, Abdelaati

Stupfler, Gilles

and

Usseglio-Carleve, Antoine

2024.

An expectile computation cookbook.

Statistics and Computing,

Vol. 34,

Issue. 3,

Bignozzi, Valeria

Merlo, Luca

and

Petrella, Lea

2024.

Inter-order relations between equivalence for L-quantiles of the Student's t distribution.

Insurance: Mathematics and Economics,

Vol. 116,

Issue. ,

p.

44.