1. Introduction

In this paper, we consider the classical compound Poisson risk model perturbed by diffusion, so that the insurer's surplus level at time  $t$ is given by

$t$ is given by

\begin{equation} U(t)=u+ct-\sum_{k=1}^{N(t)}Y_k+\sigma B(t),\quad t\ge 0, \end{equation}

\begin{equation} U(t)=u+ct-\sum_{k=1}^{N(t)}Y_k+\sigma B(t),\quad t\ge 0, \end{equation}where  $u=U(0)\ge 0$ is the initial surplus level,

$u=U(0)\ge 0$ is the initial surplus level,  $c>0$ is the incoming premium rate per unit time,

$c>0$ is the incoming premium rate per unit time,  $Y_k$ is the size of the

$Y_k$ is the size of the  $k$th insurance claim,

$k$th insurance claim,  $\{N(t)\}_{t\ge 0}$ is a Poisson process with rate

$\{N(t)\}_{t\ge 0}$ is a Poisson process with rate  $\lambda >0$,

$\lambda >0$,  $\{B(t)\}_{t\ge 0}$ is a standard Brownian motion, and

$\{B(t)\}_{t\ge 0}$ is a standard Brownian motion, and  $\sigma >0$ is the volatility parameter. It is further assumed that

$\sigma >0$ is the volatility parameter. It is further assumed that  $\{Y_k\}_{k=1}^{\infty }$ is a sequence of independent and identically distributed (i.i.d.) positive random variables with common probability density

$\{Y_k\}_{k=1}^{\infty }$ is a sequence of independent and identically distributed (i.i.d.) positive random variables with common probability density  $p(\cdot )$ and Laplace transform

$p(\cdot )$ and Laplace transform  $\tilde {p}(\cdot )$, and moreover

$\tilde {p}(\cdot )$, and moreover  $\{Y_k\}_{k=1}^{\infty }$,

$\{Y_k\}_{k=1}^{\infty }$,  $\{N(t)\}_{t\ge 0}$, and

$\{N(t)\}_{t\ge 0}$, and  $\{B(t)\}_{t\ge 0}$ are mutually independent. The time of ruin of the surplus process

$\{B(t)\}_{t\ge 0}$ are mutually independent. The time of ruin of the surplus process  $\{U(t)\}_{t\ge 0}$ is defined by

$\{U(t)\}_{t\ge 0}$ is defined by  $\tau =\inf \{t\ge 0:U(t)<0\}$. We assume that the positive security loading condition, which ensures the ruin probability

$\tau =\inf \{t\ge 0:U(t)<0\}$. We assume that the positive security loading condition, which ensures the ruin probability  $\psi (u)=\Pr \{\tau <\infty \,|\,U(0)=u\}$ is less than one for

$\psi (u)=\Pr \{\tau <\infty \,|\,U(0)=u\}$ is less than one for  $u>0$, is satisfied. Such a condition is given by

$u>0$, is satisfied. Such a condition is given by  $\theta >0$, where

$\theta >0$, where  $\theta$ is defined via

$\theta$ is defined via  $c=(1+\theta )\lambda E[Y_1]$. Note that ruin occurs immediately by diffusion if the process starts with zero initial surplus.

$c=(1+\theta )\lambda E[Y_1]$. Note that ruin occurs immediately by diffusion if the process starts with zero initial surplus.

The ruin probability of the model (1.1) was first obtained by Dufresne and Gerber [Reference Dufresne and Gerber17], who also decomposed the probability into two components, namely ruin by oscillation (i.e.  $U(\tau )=0$) and ruin by a claim (i.e.

$U(\tau )=0$) and ruin by a claim (i.e.  $U(\tau )<0$). These results were generalized by Gerber and Landry [Reference Gerber and Landry22] and Tsai and Willmot [Reference Tsai and Willmot34] who looked into the Gerber-Shiu expected discounted penalty function (see [Reference Gerber and Shiu23] and Eq. (1.2) below with

$U(\tau )<0$). These results were generalized by Gerber and Landry [Reference Gerber and Landry22] and Tsai and Willmot [Reference Tsai and Willmot34] who looked into the Gerber-Shiu expected discounted penalty function (see [Reference Gerber and Shiu23] and Eq. (1.2) below with  $n=m=0$), which takes into account not only the ruin time

$n=m=0$), which takes into account not only the ruin time  $\tau$ but also the surplus immediately prior to ruin

$\tau$ but also the surplus immediately prior to ruin  $U(\tau ^{-})$ and the deficit at ruin

$U(\tau ^{-})$ and the deficit at ruin  $|U(\tau )|$. See also, for example, Tsai [Reference Tsai32,Reference Tsai33] and Tsai and Willmot [Reference Tsai and Willmot35] for the application of Gerber-Shiu function in the present model to find related ruin functions such as the (joint) moments of the afore-mentioned variables. Extension to a perturbed renewal risk process was subsequently considered by Li and Garrido [Reference Li and Garrido27]. In the absence of the Brownian motion, various generalizations of the Gerber-Shiu function have been proposed to incorporate additional information of the surplus process before ruin occurrence. For example, Cheung et al. [Reference Cheung, Landriault, Willmot and Woo12] and Woo [Reference Woo37] included the surplus immediately after the second last claim before ruin and the minimum surplus before ruin into the penalty function whereas Cheung and Landriault [Reference Cheung and Landriault9] and Woo et al. [Reference Woo, Xu and Yang38] considered the maximum surplus before ruin. In addition, Cai et al. [Reference Cai, Feng and Willmot7] studied the total discounted operating costs defined via an integral of the sample path until ruin (see also [Reference Feng18,Reference Feng19]). Analysis of the Gerber-Shiu function in more general Lévy risk models has been performed by, for example, Garrido and Morales [Reference Garrido and Morales21], Asmussen and Albrecher [Reference Asmussen and Albrecher1, Chaps. XI and XII], and Kyprianou [Reference Kyprianou25], and extensions to path-dependent penalties can be found in, for example, Biffis and Morales [Reference Biffis and Morales2] and Feng and Shimizu [Reference Feng and Shimizu20]. On the other hand, Cheung [Reference Cheung8] and Cheung and Woo [Reference Cheung and Woo11] proposed to include in the Gerber-Shiu function a moment-based component pertaining to the total discounted claim cost until ruin, which is defined by

$|U(\tau )|$. See also, for example, Tsai [Reference Tsai32,Reference Tsai33] and Tsai and Willmot [Reference Tsai and Willmot35] for the application of Gerber-Shiu function in the present model to find related ruin functions such as the (joint) moments of the afore-mentioned variables. Extension to a perturbed renewal risk process was subsequently considered by Li and Garrido [Reference Li and Garrido27]. In the absence of the Brownian motion, various generalizations of the Gerber-Shiu function have been proposed to incorporate additional information of the surplus process before ruin occurrence. For example, Cheung et al. [Reference Cheung, Landriault, Willmot and Woo12] and Woo [Reference Woo37] included the surplus immediately after the second last claim before ruin and the minimum surplus before ruin into the penalty function whereas Cheung and Landriault [Reference Cheung and Landriault9] and Woo et al. [Reference Woo, Xu and Yang38] considered the maximum surplus before ruin. In addition, Cai et al. [Reference Cai, Feng and Willmot7] studied the total discounted operating costs defined via an integral of the sample path until ruin (see also [Reference Feng18,Reference Feng19]). Analysis of the Gerber-Shiu function in more general Lévy risk models has been performed by, for example, Garrido and Morales [Reference Garrido and Morales21], Asmussen and Albrecher [Reference Asmussen and Albrecher1, Chaps. XI and XII], and Kyprianou [Reference Kyprianou25], and extensions to path-dependent penalties can be found in, for example, Biffis and Morales [Reference Biffis and Morales2] and Feng and Shimizu [Reference Feng and Shimizu20]. On the other hand, Cheung [Reference Cheung8] and Cheung and Woo [Reference Cheung and Woo11] proposed to include in the Gerber-Shiu function a moment-based component pertaining to the total discounted claim cost until ruin, which is defined by  $Z_\delta (\tau )$ where

$Z_\delta (\tau )$ where  $Z_\delta (t)=\sum _{k=1}^{N(t)}e^{-\delta T_k}f(Y_k)$ for

$Z_\delta (t)=\sum _{k=1}^{N(t)}e^{-\delta T_k}f(Y_k)$ for  $t\ge 0$. Here,

$t\ge 0$. Here,  $\{T_k\}_{k=1}^{\infty }$ are the arrival times of the claims (which are the arrival epochs of the Poisson process

$\{T_k\}_{k=1}^{\infty }$ are the arrival times of the claims (which are the arrival epochs of the Poisson process  $\{N(t)\}_{t\ge 0}$ in our model),

$\{N(t)\}_{t\ge 0}$ in our model),  $f(\cdot )$ is a non-negative “cost function” defined on

$f(\cdot )$ is a non-negative “cost function” defined on  $(0,\infty )$ that assigns a cost to each claim amount, and

$(0,\infty )$ that assigns a cost to each claim amount, and  $\delta \ge 0$ is the force of interest for discounting the costs. Higher moments of the present value of dividends until ruin were further added to the analysis under different dividend strategies by Cheung et al. [Reference Cheung, Liu and Woo13] and Cheung and Liu [Reference Cheung and Liu10].

$\delta \ge 0$ is the force of interest for discounting the costs. Higher moments of the present value of dividends until ruin were further added to the analysis under different dividend strategies by Cheung et al. [Reference Cheung, Liu and Woo13] and Cheung and Liu [Reference Cheung and Liu10].

While the Brownian motion  $\{B(t)\}_{t\ge 0}$ in the dynamics (1.1) is typically interpreted as small perturbations of the surplus process due to the uncertainties in day-to-day insurance operation not explained by insurance claims, in financial mathematics it is important to take into account the time value of money. This suggests that one may look into ruin quantities in relation to the stochastic integral

$\{B(t)\}_{t\ge 0}$ in the dynamics (1.1) is typically interpreted as small perturbations of the surplus process due to the uncertainties in day-to-day insurance operation not explained by insurance claims, in financial mathematics it is important to take into account the time value of money. This suggests that one may look into ruin quantities in relation to the stochastic integral  $B_\delta (t)=\int _0^{t} e^{-\delta s}\,dB(s)$ for

$B_\delta (t)=\int _0^{t} e^{-\delta s}\,dB(s)$ for  $t\ge 0$. Inspired by the above latest developments in the study of discounted claim costs until ruin, we shall consider the total discounted perturbation until ruin, namely

$t\ge 0$. Inspired by the above latest developments in the study of discounted claim costs until ruin, we shall consider the total discounted perturbation until ruin, namely  $B_\delta (\tau )$. To the best of our knowledge, the quantity

$B_\delta (\tau )$. To the best of our knowledge, the quantity  $B_\delta (\tau )=\int _0^{\tau } e^{-\delta s}\,dB(s)$ has never been analyzed in the context of Gerber-Shiu functions. Note that although

$B_\delta (\tau )=\int _0^{\tau } e^{-\delta s}\,dB(s)$ has never been analyzed in the context of Gerber-Shiu functions. Note that although  $E[B_\delta (t)]=0$ for fixed time

$E[B_\delta (t)]=0$ for fixed time  $t\ge 0$, in general

$t\ge 0$, in general  $B_\delta (\tau )$ does not necessarily have zero mean because the ruin time

$B_\delta (\tau )$ does not necessarily have zero mean because the ruin time  $\tau$ is a random variable that depends on the sample path of

$\tau$ is a random variable that depends on the sample path of  $\{U(t)\}_{t\ge 0}$ which, in turn, involves

$\{U(t)\}_{t\ge 0}$ which, in turn, involves  $\{B(t)\}_{t\ge 0}$. Indeed, one expects that sample paths of

$\{B(t)\}_{t\ge 0}$. Indeed, one expects that sample paths of  $\{U(t)\}_{t\ge 0}$ leading to ruin are more likely to have faced unfavorable business conditions, and therefore,

$\{U(t)\}_{t\ge 0}$ leading to ruin are more likely to have faced unfavorable business conditions, and therefore,  $B_\delta (\tau )$ is expected to have negative mean (see numerical illustrations in Section 4). Hence,

$B_\delta (\tau )$ is expected to have negative mean (see numerical illustrations in Section 4). Hence,  $-B_\delta (\tau )$ may be regarded as part of the discounted costs (in addition to discounted claims), which can be important for risk management purposes as far as the event of ruin is concerned. For

$-B_\delta (\tau )$ may be regarded as part of the discounted costs (in addition to discounted claims), which can be important for risk management purposes as far as the event of ruin is concerned. For  $n,m\in \mathbb {N}$ (with

$n,m\in \mathbb {N}$ (with  $\mathbb {N}$ the set of non-negative integers), we propose to study the generalized Gerber-Shiu function

$\mathbb {N}$ the set of non-negative integers), we propose to study the generalized Gerber-Shiu function

\begin{equation} \phi_{\delta_{123},n,m}(u)=\phi_{w,\delta_{123},n,m}(u)+w_0\phi_{d,\delta_{123},n,m}(u), \quad u\ge 0, \end{equation}

\begin{equation} \phi_{\delta_{123},n,m}(u)=\phi_{w,\delta_{123},n,m}(u)+w_0\phi_{d,\delta_{123},n,m}(u), \quad u\ge 0, \end{equation}where

\begin{equation} \phi_{w,\delta_{123},n,m}(u)=E[e^{-\delta_1 \tau} B_{\delta_2}^{n}(\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}}\,|\,U(0)=u] \end{equation}

\begin{equation} \phi_{w,\delta_{123},n,m}(u)=E[e^{-\delta_1 \tau} B_{\delta_2}^{n}(\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}}\,|\,U(0)=u] \end{equation}is contributed by ruin occurrence due to a claim, and

\begin{equation} \phi_{d,\delta_{123},n,m}(u)=E[e^{-\delta_1 \tau} B_{\delta_2}^{n}(\tau)Z_{\delta_3}^{m}(\tau) 1_{\{\tau<\infty,U(\tau)=0\}}\,|\,U(0)=u] \end{equation}

\begin{equation} \phi_{d,\delta_{123},n,m}(u)=E[e^{-\delta_1 \tau} B_{\delta_2}^{n}(\tau)Z_{\delta_3}^{m}(\tau) 1_{\{\tau<\infty,U(\tau)=0\}}\,|\,U(0)=u] \end{equation}is the contribution from ruin by oscillation. In addition,  $w(\cdot,\cdot )$ appearing in (1.3) is a non-negative “penalty” defined on

$w(\cdot,\cdot )$ appearing in (1.3) is a non-negative “penalty” defined on  $[0,\infty )\times (0,\infty )$ as a function of the surplus prior to ruin and the deficit, and

$[0,\infty )\times (0,\infty )$ as a function of the surplus prior to ruin and the deficit, and  $w_0\ge 0$ in (1.2) is the constant “penalty” due at ruin if ruin occurs by oscillation. The notation “

$w_0\ge 0$ in (1.2) is the constant “penalty” due at ruin if ruin occurs by oscillation. The notation “ $\delta _{123}$” above can be regarded as an abbreviation that contains information about

$\delta _{123}$” above can be regarded as an abbreviation that contains information about  $\delta _1$,

$\delta _1$,  $\delta _2$, and

$\delta _2$, and  $\delta _3$, which are possibly of different values and assumed non-negative. When the orders of moments

$\delta _3$, which are possibly of different values and assumed non-negative. When the orders of moments  $n$ and

$n$ and  $m$ are both equal to zero,

$m$ are both equal to zero,  $\phi _{\delta _{123},n,m}(u)$ reduces to the traditional Gerber-Shiu function. For convenience, the powers of

$\phi _{\delta _{123},n,m}(u)$ reduces to the traditional Gerber-Shiu function. For convenience, the powers of  $B_{\delta _2}(\tau )$ and

$B_{\delta _2}(\tau )$ and  $Z_{\delta _3}(\tau )$ are written as

$Z_{\delta _3}(\tau )$ are written as  $B_{\delta _2}^{n}(\tau )=\{B_{\delta _2}(\tau )\}^{n}$ and

$B_{\delta _2}^{n}(\tau )=\{B_{\delta _2}(\tau )\}^{n}$ and  $Z_{\delta _3}^{m}(\tau )=\{Z_{\delta _3}(\tau )\}^{m}$, respectively, and we shall also denote the power of cost function as

$Z_{\delta _3}^{m}(\tau )=\{Z_{\delta _3}(\tau )\}^{m}$, respectively, and we shall also denote the power of cost function as  $f^{m}(y)=\{f(y)\}^{m}$. We remark that the special case of

$f^{m}(y)=\{f(y)\}^{m}$. We remark that the special case of  $\phi _{\delta _{123},n,m}(u)$ where

$\phi _{\delta _{123},n,m}(u)$ where  $n=0$ and the penalty function only depends on the deficit was analyzed by Liu and Zhang [Reference Liu and Zhang28]. Our general version

$n=0$ and the penalty function only depends on the deficit was analyzed by Liu and Zhang [Reference Liu and Zhang28]. Our general version  $\phi _{\delta _{123},n,m}(u)$ allows us to obtain not only the moments of

$\phi _{\delta _{123},n,m}(u)$ allows us to obtain not only the moments of  $B_{\delta _2}(\tau )$ but also the joint moments of

$B_{\delta _2}(\tau )$ but also the joint moments of  $B_{\delta _2}(\tau )$ and

$B_{\delta _2}(\tau )$ and  $Z_{\delta _3}(\tau )$. In particular, the covariance between

$Z_{\delta _3}(\tau )$. In particular, the covariance between  $B_{\delta _2}(\tau )$ and

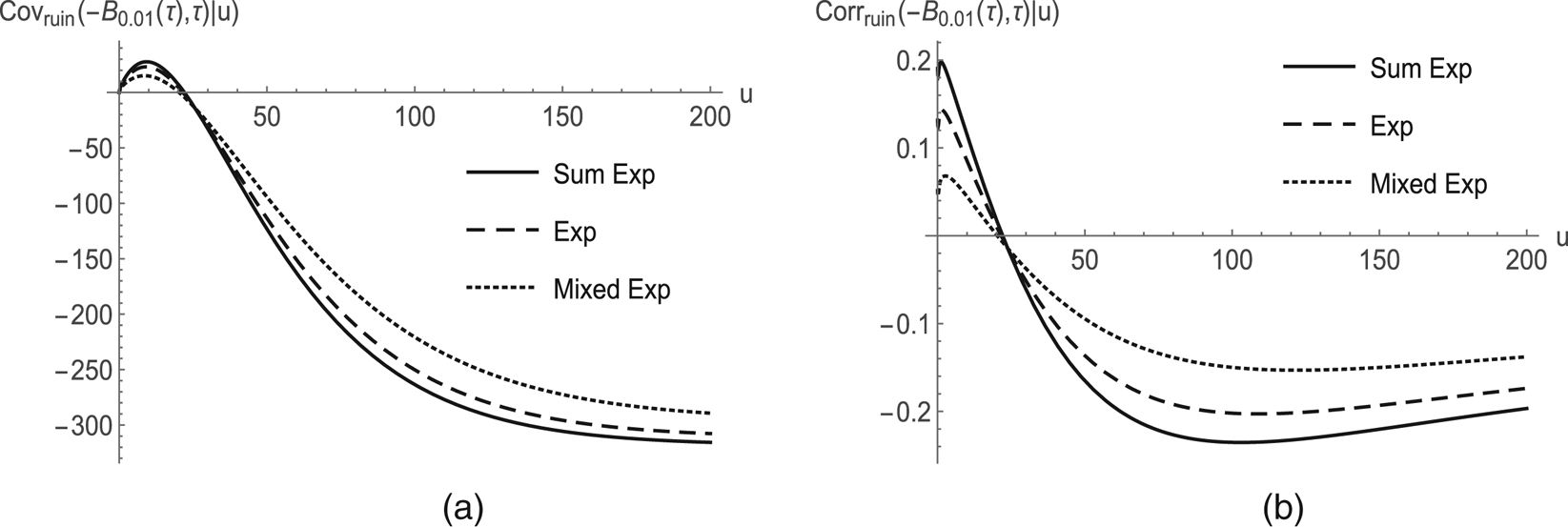

$B_{\delta _2}(\tau )$ and  $Z_{\delta _3}(\tau )$ (conditional on ruin) represents an interesting quantity that indicates whether the discounted small fluctuations and the discounted claims tend to move in the same or opposite direction when ruin occurs (see numerical analysis in Section 4). Moreover, (joint) moments involving the time of ruin

$Z_{\delta _3}(\tau )$ (conditional on ruin) represents an interesting quantity that indicates whether the discounted small fluctuations and the discounted claims tend to move in the same or opposite direction when ruin occurs (see numerical analysis in Section 4). Moreover, (joint) moments involving the time of ruin  $\tau$ can also be obtained from our Gerber-Shiu functions by differentiation with respect to

$\tau$ can also be obtained from our Gerber-Shiu functions by differentiation with respect to  $\delta _1$ (see (4.2)). It is worthwhile to point out that the technique of using potential measures in Liu and Zhang [Reference Liu and Zhang28] is no longer applicable in our case due to the presence of the stochastic integral

$\delta _1$ (see (4.2)). It is worthwhile to point out that the technique of using potential measures in Liu and Zhang [Reference Liu and Zhang28] is no longer applicable in our case due to the presence of the stochastic integral  $B_{\delta _2}(\tau )$ in our Gerber-Shiu function, and we must resort to the use of Itô's lemma.

$B_{\delta _2}(\tau )$ in our Gerber-Shiu function, and we must resort to the use of Itô's lemma.

This paper is organized as follows. In Section 2, with the help of Itô's lemma, recursive integro-differential equations (in  $n$ and

$n$ and  $m$) satisfied by

$m$) satisfied by  $\phi _{w,\delta _{123},n,m}(\cdot )$ and

$\phi _{w,\delta _{123},n,m}(\cdot )$ and  $\phi _{d,\delta _{123},n,m}(\cdot )$ are derived. These are then transformed to defective renewal equations where the components are specified (and hence, general solutions are available). Section 3 derives the explicit solutions under the special case where the claim amounts are distributed as a combination of exponentials and the penalty function

$\phi _{d,\delta _{123},n,m}(\cdot )$ are derived. These are then transformed to defective renewal equations where the components are specified (and hence, general solutions are available). Section 3 derives the explicit solutions under the special case where the claim amounts are distributed as a combination of exponentials and the penalty function  $w(\cdot,\cdot )$ depends on the deficit only but not on the surplus prior to ruin. Section 4 ends the paper with numerical illustrations, which include the computation of the covariance between discounted claims and discounted perturbation until ruin along with some intuitive explanations.

$w(\cdot,\cdot )$ depends on the deficit only but not on the surplus prior to ruin. Section 4 ends the paper with numerical illustrations, which include the computation of the covariance between discounted claims and discounted perturbation until ruin along with some intuitive explanations.

2. General results on the joint moments

Before studying  $\phi _{w,\delta _{123},n,m}(u)$ and

$\phi _{w,\delta _{123},n,m}(u)$ and  $\phi _{d,\delta _{123},n,m}(u)$ defined by (1.3) and (1.4) for

$\phi _{d,\delta _{123},n,m}(u)$ defined by (1.3) and (1.4) for  $n,m\in \mathbb {N}$, we would like to collect the assumptions/conditions that will be used in the upcoming analysis. It will be seen from Theorem 1 that the integro-differential equation (2.2) satisfied by

$n,m\in \mathbb {N}$, we would like to collect the assumptions/conditions that will be used in the upcoming analysis. It will be seen from Theorem 1 that the integro-differential equation (2.2) satisfied by  $\phi _{w,\delta _{123},n,m}(\cdot )$ is recursive in

$\phi _{w,\delta _{123},n,m}(\cdot )$ is recursive in  $n$ and

$n$ and  $m$. In particular, the nonhomogeneous term (2.4) in such equation contains the “lower-order” Gerber-Shiu functions

$m$. In particular, the nonhomogeneous term (2.4) in such equation contains the “lower-order” Gerber-Shiu functions  $\phi _{w,\delta _{123},n-1,m}(\cdot )$,

$\phi _{w,\delta _{123},n-1,m}(\cdot )$,  $\phi _{w,\delta _{123},n-2,m}(\cdot )$, and

$\phi _{w,\delta _{123},n-2,m}(\cdot )$, and  $\{\phi _{w,\delta _{123},n,j}(\cdot )\}_{j=0}^{m-1}$. As a result, its general solution in Theorem 2 depends on these lower-order Gerber-Shiu functions which, in turn, depend on Gerber-Shiu functions that are of even lower order. Inductively, the solution for

$\{\phi _{w,\delta _{123},n,j}(\cdot )\}_{j=0}^{m-1}$. As a result, its general solution in Theorem 2 depends on these lower-order Gerber-Shiu functions which, in turn, depend on Gerber-Shiu functions that are of even lower order. Inductively, the solution for  $\phi _{w,\delta _{123},n,m}(\cdot )$ (for given

$\phi _{w,\delta _{123},n,m}(\cdot )$ (for given  $n,m\in \mathbb {N}$) relies on and requires the existence of solutions for

$n,m\in \mathbb {N}$) relies on and requires the existence of solutions for  $\phi _{w,\delta _{123},i,j}(\cdot )$'s with

$\phi _{w,\delta _{123},i,j}(\cdot )$'s with  $(i,j)\in \Upsilon (n,m)$, where

$(i,j)\in \Upsilon (n,m)$, where  $\Upsilon (n,m)=\{(i,j): 0\leq i\leq n; 0\leq j \leq m\}\setminus \{(n,m)\}$. Therefore, the following assumptions/conditions concerning the analysis of

$\Upsilon (n,m)=\{(i,j): 0\leq i\leq n; 0\leq j \leq m\}\setminus \{(n,m)\}$. Therefore, the following assumptions/conditions concerning the analysis of  $\phi _{w,\delta _{123},n,m}(\cdot )$ for given

$\phi _{w,\delta _{123},n,m}(\cdot )$ for given  $n,m\in \mathbb {N}$ are also a result of the inductive procedure. The same comments apply to

$n,m\in \mathbb {N}$ are also a result of the inductive procedure. The same comments apply to  $\phi _{d,\delta _{123},n,m}(\cdot )$.

$\phi _{d,\delta _{123},n,m}(\cdot )$.

• Assumption 1. For

$i=0,1,2,\ldots,n$ and $j=0,1,2,\ldots,m$, the functions $\phi _{w,\delta _{123},i,j}(\cdot )$ and $\phi _{d,\delta _{123},i,j}(\cdot )$ are twice continuously differentiable on $[0,\infty )$.

$i=0,1,2,\ldots,n$ and $j=0,1,2,\ldots,m$, the functions $\phi _{w,\delta _{123},i,j}(\cdot )$ and $\phi _{d,\delta _{123},i,j}(\cdot )$ are twice continuously differentiable on $[0,\infty )$.• Assumption 2. For

$i=0,1,2,\ldots,n$ and $j=0,1,2,\ldots,m$, the functions $\phi _{w,\delta _{123},i,j}(\cdot )$ and $\phi _{d,\delta _{123},i,j}(\cdot )$ are bounded on $[0,\infty )$, and their first and second derivatives are bounded on $[0,\infty )$ as well.

Assumptions 1 and 2 concerning continuous differentiability and bounded derivatives are rather common in ruin theory involving diffusion (e.g. [Reference Paulsen and Gjessing30, Thm. 2.1], [Reference Cai and Yang6, Thms. 3.2 and 3.3], and [Reference Cai and Xu5, Thms. 2.1–2.3]) and they are not easy to verify or prove in general. Interested readers are referred to, for example, Wang and Wu [Reference Wang and Wu36], Cai [Reference Cai4, Thm. 3.2], Cai and Yang [Reference Cai and Yang6, Thm. 2.1], Loisel [Reference Loisel29], and Zhu and Yang [Reference Zhu and Yang39] for detailed treatment of differentiability of ruin functions.

• Assumption 3. For

$i=0,1,2,\ldots,n$ and $j=0,1,2,\ldots,m$, the limits $\lim _{u \to \infty } e^{-\rho _{i,j}u}\phi _{w,\delta _{123},i,j}(u)=\lim _{u \to \infty } e^{-\rho _{i,j}u}\phi _{w,\delta _{123},i,j}'(u)=0$ and $\lim _{u \to \infty } e^{-\rho _{i,j}u}\phi _{d,\delta _{123},i,j}(u)=\lim _{u \to \infty } e^{-\rho _{i,j}u}\phi _{d,\delta _{123},i,j}'(u)=0$ are valid, where $\rho _{i,j}$ is the unique non-negative root of the Lundberg's equation (in $\xi$)

(2.1)\begin{equation} \frac{\sigma^{2}}{2}\xi^{2}+c\xi-(\lambda +\delta_1+i\delta_2+j\delta_3)+\lambda \tilde{p}(\xi)=0. \end{equation}

Except for  $\rho _{i,j}$, all other roots of the Lundberg's equation (2.1) have negative real parts. In particular,

$\rho _{i,j}$, all other roots of the Lundberg's equation (2.1) have negative real parts. In particular,  $\rho _{i,j}=0$ when

$\rho _{i,j}=0$ when  $\delta _1+i\delta _2+j\delta _3=0$ and

$\delta _1+i\delta _2+j\delta _3=0$ and  $\rho _{i,j}>0$ when

$\rho _{i,j}>0$ when  $\delta _1+i\delta _2+j\delta _3>0$ (see, e.g., [Reference Gerber and Landry22]). The Lundberg's equation (2.1) typically arises when taking Laplace transforms on both sides of the integro-differential equation satisfied by a Gerber-Shiu type function to convert it to a defective renewal equation (see, e.g., [Reference Tsai and Willmot34]). In such a transformation concerning

$\delta _1+i\delta _2+j\delta _3>0$ (see, e.g., [Reference Gerber and Landry22]). The Lundberg's equation (2.1) typically arises when taking Laplace transforms on both sides of the integro-differential equation satisfied by a Gerber-Shiu type function to convert it to a defective renewal equation (see, e.g., [Reference Tsai and Willmot34]). In such a transformation concerning  $\phi _{w,\delta _{123},n,m}(\cdot )$ and

$\phi _{w,\delta _{123},n,m}(\cdot )$ and  $\phi _{d,\delta _{123},n,m}(\cdot )$, Assumption 3 will be needed.

$\phi _{d,\delta _{123},n,m}(\cdot )$, Assumption 3 will be needed.

• Condition 1. For

$k=0,1,2,\ldots,m$, the integral $\int _0^{\infty } f^{k}(y)p(y)\,dy$ is finite.• Condition 2. For

$k=0,1,2,\ldots,m$, the integral $\int _{u}^{\infty } f^{k}(y)w(u,y-u)p(y)\,dy$ (as a function of $u\ge 0$) is bounded.

Condition 2 above involves the penalty function and is only required for the analysis of  $\phi _{w,\delta _{123},n,m}(u)$ but not

$\phi _{w,\delta _{123},n,m}(u)$ but not  $\phi _{d,\delta _{123},n,m}(u)$. Note that, upon specifying the claim density

$\phi _{d,\delta _{123},n,m}(u)$. Note that, upon specifying the claim density  $p(\cdot )$, cost function

$p(\cdot )$, cost function  $f(\cdot )$, and penalty function

$f(\cdot )$, and penalty function  $w(\cdot,\cdot )$, Conditions 1 and 2 can be checked on a case-by-case basis via direct integration.

$w(\cdot,\cdot )$, Conditions 1 and 2 can be checked on a case-by-case basis via direct integration.

For ease of reference, some notation that will be used repeatedly is summarized in Table 1.

TABLE 1. Definition of some important notation.

2.1. Integro-differential equations

We have the following theorem regarding the integro-differential equations satisfied by  $\phi _{w,\delta _{123},n,m}(\cdot )$ and

$\phi _{w,\delta _{123},n,m}(\cdot )$ and  $\phi _{d,\delta _{123},n,m}(\cdot )$.

$\phi _{d,\delta _{123},n,m}(\cdot )$.

Theorem 1 (Integro-differential equations for $\phi _{w,\delta _{123},n,m}(\cdot )$ and $\phi _{d,\delta _{123},n,m}(\cdot )$)

Under Assumptions 1–2 and Conditions 1–2,  $\phi _{w,\delta _{123},n,m}(\cdot )$ and

$\phi _{w,\delta _{123},n,m}(\cdot )$ and  $\phi _{d,\delta _{123},n,m}(\cdot )$ satisfy the recursive integro-differential equations (for

$\phi _{d,\delta _{123},n,m}(\cdot )$ satisfy the recursive integro-differential equations (for  $n,m\in \mathbb {N}$ and

$n,m\in \mathbb {N}$ and  $u>0$)

$u>0$)

\begin{align} & \frac{\sigma^{2}}{2} \phi_{w,\delta_{123},n,m}''(u)+c\phi_{w,\delta_{123},n,m}'(u)-(\lambda+\delta_1 +n\delta_2+m\delta_3)\phi_{w,\delta_{123},n,m}(u)\nonumber\\ & \quad +\lambda \int_0^{u} \phi_{w,\delta_{123},n,m}(u-y)p(y)\,dy={-}A_{w,n,m}(u), \end{align}

\begin{align} & \frac{\sigma^{2}}{2} \phi_{w,\delta_{123},n,m}''(u)+c\phi_{w,\delta_{123},n,m}'(u)-(\lambda+\delta_1 +n\delta_2+m\delta_3)\phi_{w,\delta_{123},n,m}(u)\nonumber\\ & \quad +\lambda \int_0^{u} \phi_{w,\delta_{123},n,m}(u-y)p(y)\,dy={-}A_{w,n,m}(u), \end{align}and

\begin{align} & \frac{\sigma^{2}}{2} \phi_{d,\delta_{123},n,m}''(u)+c\phi_{d,\delta_{123},n,m}'(u)-(\lambda+\delta_1 +n\delta_2+m\delta_3)\phi_{d,\delta_{123},n,m}(u)\nonumber\\ & \quad +\lambda \int_0^{u} \phi_{d,\delta_{123},n,m}(u-y)p(y)\,dy={-}A_{d,n,m}(u), \end{align}

\begin{align} & \frac{\sigma^{2}}{2} \phi_{d,\delta_{123},n,m}''(u)+c\phi_{d,\delta_{123},n,m}'(u)-(\lambda+\delta_1 +n\delta_2+m\delta_3)\phi_{d,\delta_{123},n,m}(u)\nonumber\\ & \quad +\lambda \int_0^{u} \phi_{d,\delta_{123},n,m}(u-y)p(y)\,dy={-}A_{d,n,m}(u), \end{align}respectively. The nonhomogeneous terms above are given by

\begin{align} A_{w,n,m}(u)& =n\sigma 1_{\{n \geq 1\}} \phi_{w,\delta_{123},n-1,m}'(u)+\frac{n(n-1)}{2}1_{\{n \geq 2\}}\phi_{w,\delta_{123},n-2,m}(u)\nonumber\\ & \quad +\lambda \sum_{j=0}^{m-1} {m \choose j}\int_0^{u} f^{m-j}(y)\phi_{w,\delta_{123},n,j}(u-y)p(y)\,dy \nonumber\\ & \quad +\lambda 1_{\{n=0\}} \int_u^{\infty} f^{m}(y)w(u,y-u)p(y)\,dy, \end{align}

\begin{align} A_{w,n,m}(u)& =n\sigma 1_{\{n \geq 1\}} \phi_{w,\delta_{123},n-1,m}'(u)+\frac{n(n-1)}{2}1_{\{n \geq 2\}}\phi_{w,\delta_{123},n-2,m}(u)\nonumber\\ & \quad +\lambda \sum_{j=0}^{m-1} {m \choose j}\int_0^{u} f^{m-j}(y)\phi_{w,\delta_{123},n,j}(u-y)p(y)\,dy \nonumber\\ & \quad +\lambda 1_{\{n=0\}} \int_u^{\infty} f^{m}(y)w(u,y-u)p(y)\,dy, \end{align}and

\begin{align} A_{d,n,m}(u)& =n\sigma 1_{\{n \geq 1\}} \phi_{d,\delta_{123},n-1,m}'(u)+\frac{n(n-1)}{2}1_{\{n \geq 2\}}\phi_{d,\delta_{123},n-2,m}(u)\nonumber\\ & \quad +\lambda \sum_{j=0}^{m-1} {m \choose j}\int_0^{u} f^{m-j}(y)\phi_{d,\delta_{123},n,j}(u-y)p(y)\,dy, \end{align}

\begin{align} A_{d,n,m}(u)& =n\sigma 1_{\{n \geq 1\}} \phi_{d,\delta_{123},n-1,m}'(u)+\frac{n(n-1)}{2}1_{\{n \geq 2\}}\phi_{d,\delta_{123},n-2,m}(u)\nonumber\\ & \quad +\lambda \sum_{j=0}^{m-1} {m \choose j}\int_0^{u} f^{m-j}(y)\phi_{d,\delta_{123},n,j}(u-y)p(y)\,dy, \end{align}which are expressed in terms of the respective lower-order Gerber-Shiu functions.

Proof. For notational brevity, the initial condition  $U(0)=u>0$ will be suppressed throughout the proof. We first consider the Gerber-Shiu function

$U(0)=u>0$ will be suppressed throughout the proof. We first consider the Gerber-Shiu function  $\phi _{w,\delta _{123},n,m}(u)$ defined in (1.3). By conditioning on whether the first claim occurs by time

$\phi _{w,\delta _{123},n,m}(u)$ defined in (1.3). By conditioning on whether the first claim occurs by time  $t$ (for some

$t$ (for some  $t>0$ where we will let

$t>0$ where we will let  $t\to 0^{+}$ later on), we arrive at

$t\to 0^{+}$ later on), we arrive at

\begin{align} \phi_{w,\delta_{123},n,m}(u) & =e^{-\lambda t} E[e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}} | T_1>t]\nonumber\\ & \quad +\int_0^{t} \lambda e^{-\lambda s} E[e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}} \big| T_1=s]\,ds. \end{align}

\begin{align} \phi_{w,\delta_{123},n,m}(u) & =e^{-\lambda t} E[e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}} | T_1>t]\nonumber\\ & \quad +\int_0^{t} \lambda e^{-\lambda s} E[e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}} \big| T_1=s]\,ds. \end{align} For any  $s\ge 0$, let

$s\ge 0$, let  $\mathcal {G}_s$ be the sigma-field generated by

$\mathcal {G}_s$ be the sigma-field generated by  $\{B(v)\}_{0 \leq v \leq s}$. For any

$\{B(v)\}_{0 \leq v \leq s}$. For any  $t>0$, let

$t>0$, let  $\hat {B}_t(s)=B(s+t)-B(t)$ for

$\hat {B}_t(s)=B(s+t)-B(t)$ for  $s \geq 0$. Since

$s \geq 0$. Since  $\{Y_k\}_{k=1}^{\infty },$

$\{Y_k\}_{k=1}^{\infty },$  $\{N(s)\}_{s\ge 0}$, and

$\{N(s)\}_{s\ge 0}$, and  $\{B(s)\}_{s \geq 0}$ are mutually independent and a Brownian motion has stationary and independent increments, it is clear that

$\{B(s)\}_{s \geq 0}$ are mutually independent and a Brownian motion has stationary and independent increments, it is clear that  $\{\hat {B}_t(s)\}_{s \geq 0}$ is a standard Brownian motion independent of

$\{\hat {B}_t(s)\}_{s \geq 0}$ is a standard Brownian motion independent of  $\{B(s)\}_{0 \leq s \leq t}$,

$\{B(s)\}_{0 \leq s \leq t}$,  $\{Y_k\}_{k=1}^{\infty }$, and

$\{Y_k\}_{k=1}^{\infty }$, and  $\{N(s)\}_{s\ge 0}$. Also, let

$\{N(s)\}_{s\ge 0}$. Also, let  $\hat {\tau }_0=\inf \{s\ge 0: u+cs+\sigma B(s)<0\}$ be the first time when the drifted Brownian motion

$\hat {\tau }_0=\inf \{s\ge 0: u+cs+\sigma B(s)<0\}$ be the first time when the drifted Brownian motion  $\{u+cs+\sigma B(s)\}_{s\ge 0}$ falls below zero, and this stopping time will repeatedly appear in our analysis. Because ruin occurs by a claim on the set

$\{u+cs+\sigma B(s)\}_{s\ge 0}$ falls below zero, and this stopping time will repeatedly appear in our analysis. Because ruin occurs by a claim on the set  $\{\tau <\infty,U(\tau )<0\}$, given that the first claim occurs after time

$\{\tau <\infty,U(\tau )<0\}$, given that the first claim occurs after time  $t$ one must have

$t$ one must have  $\hat {\tau }_0>t$ (otherwise ruin would have occurred by oscillation). Therefore, the first expectation term in (2.6) is

$\hat {\tau }_0>t$ (otherwise ruin would have occurred by oscillation). Therefore, the first expectation term in (2.6) is

\begin{align} & E[e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}}\,|\, T_1>t]\nonumber\\ & \quad = E[e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}} 1_{\{\hat{\tau}_0>t\}}\,|\, T_1>t]\nonumber\\ & \quad = E\left[e^{-\delta_1 \tau}\left(B_{\delta_2}(t)+\int_t^{\tau} e^{-\delta_2 s}\,dB(s) \right)^{n} \left(e^{-\delta_3 t} \sum_{k=1}^{N(\tau)} e^{-\delta_3 (T_k-t)} f(Y_k)\right)^{m} \right.\nonumber\\ & \qquad \left.\times w(U(\tau^{-}),|U(\tau)|) 1_{\{\tau<\infty,U(\tau)<0\}} 1_{\{\hat{\tau}_0>t\}}\,|\, T_1>t\vphantom{\sum_{k=1}^{N(\tau)}}\right]\nonumber\\ & \quad = \sum_{i=0}^{n} {n \choose i} e^{-(\delta_1+m\delta_3) t}E\left[e^{-\delta_1 (\tau-t)}B_{\delta_2}^{i} (t)\left(\int_t^{\tau} e^{-\delta_2 s}\,dB(s) \right)^{n-i} \left( \sum_{k=1}^{N(\tau)} e^{-\delta_3 (T_k-t)} f(Y_k)\right)^{m}\right.\nonumber\\ & \qquad \left.\times w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}} 1_{\{\hat{\tau}_0>t\}}\,|\, T_1>t\vphantom{\sum_{k=1}^{N(\tau)}}\right]\nonumber\\ & \quad = \sum_{i=0}^{n} {n \choose i} e^{-(\delta_1+(n-i)\delta_2+m\delta_3) t}E\left[B_{\delta_2}^{i} (t)e^{-\delta_1 (\tau-t)}\left(\int_0^{\tau-t} e^{-\delta_2 s}\,dB(s+t) \right)^{n-i}\right.\nonumber\\ & \qquad \left.\times \left( \sum_{k=1}^{N(\tau)} e^{-\delta_3 (T_k-t)} f(Y_k)\right)^{m} w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}} 1_{\{\hat{\tau}_0>t\}}\,|\, T_1>t\vphantom{\sum_{k=1}^{N(\tau)}}\right]\nonumber\\ & \quad = \sum_{i=0}^{n} {n \choose i} e^{-(\delta_1+(n-i)\delta_2+m\delta_3) t}E\left[B_{\delta_2}^{i} (t)1_{\{\hat{\tau}_0>t\}}E\left[e^{-\delta_1 (\tau-t)}\left(\int_0^{\tau-t} e^{-\delta_2 s}\,d\hat{B}_t(s)\right)^{n-i}\right.\right.\nonumber\\ & \qquad \left.\left.\left.\times \left( \sum_{k=1}^{N(\tau)} e^{-\delta_3 (T_k-t)} f(Y_k)\right)^{m} w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}} \,|\, \mathcal{G}_t \vee \{T_1>t\}\right]\right|\, T_1>t\right]\nonumber\\ & \quad = \sum_{i=0}^{n} {n \choose i} e^{-(\delta_1+(n-i)\delta_2+m\delta_3) t}E[B_{\delta_2}^{i} (t)1_{\{\hat{\tau}_0>t\}} \phi_{w,\delta_{123},n-i,m}(u+ct+\sigma B(t))\,|\,T_1>t]\nonumber\\ & \quad = \sum_{i=0}^{n} {n \choose i} e^{-(\delta_1+(n-i)\delta_2+m\delta_3) t}E[B_{\delta_2}^{i} (t)1_{\{\hat{\tau}_0>t\}} \phi_{w,\delta_{123},n-i,m}(u+ct+\sigma B(t))]. \end{align}

\begin{align} & E[e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}}\,|\, T_1>t]\nonumber\\ & \quad = E[e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}} 1_{\{\hat{\tau}_0>t\}}\,|\, T_1>t]\nonumber\\ & \quad = E\left[e^{-\delta_1 \tau}\left(B_{\delta_2}(t)+\int_t^{\tau} e^{-\delta_2 s}\,dB(s) \right)^{n} \left(e^{-\delta_3 t} \sum_{k=1}^{N(\tau)} e^{-\delta_3 (T_k-t)} f(Y_k)\right)^{m} \right.\nonumber\\ & \qquad \left.\times w(U(\tau^{-}),|U(\tau)|) 1_{\{\tau<\infty,U(\tau)<0\}} 1_{\{\hat{\tau}_0>t\}}\,|\, T_1>t\vphantom{\sum_{k=1}^{N(\tau)}}\right]\nonumber\\ & \quad = \sum_{i=0}^{n} {n \choose i} e^{-(\delta_1+m\delta_3) t}E\left[e^{-\delta_1 (\tau-t)}B_{\delta_2}^{i} (t)\left(\int_t^{\tau} e^{-\delta_2 s}\,dB(s) \right)^{n-i} \left( \sum_{k=1}^{N(\tau)} e^{-\delta_3 (T_k-t)} f(Y_k)\right)^{m}\right.\nonumber\\ & \qquad \left.\times w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}} 1_{\{\hat{\tau}_0>t\}}\,|\, T_1>t\vphantom{\sum_{k=1}^{N(\tau)}}\right]\nonumber\\ & \quad = \sum_{i=0}^{n} {n \choose i} e^{-(\delta_1+(n-i)\delta_2+m\delta_3) t}E\left[B_{\delta_2}^{i} (t)e^{-\delta_1 (\tau-t)}\left(\int_0^{\tau-t} e^{-\delta_2 s}\,dB(s+t) \right)^{n-i}\right.\nonumber\\ & \qquad \left.\times \left( \sum_{k=1}^{N(\tau)} e^{-\delta_3 (T_k-t)} f(Y_k)\right)^{m} w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}} 1_{\{\hat{\tau}_0>t\}}\,|\, T_1>t\vphantom{\sum_{k=1}^{N(\tau)}}\right]\nonumber\\ & \quad = \sum_{i=0}^{n} {n \choose i} e^{-(\delta_1+(n-i)\delta_2+m\delta_3) t}E\left[B_{\delta_2}^{i} (t)1_{\{\hat{\tau}_0>t\}}E\left[e^{-\delta_1 (\tau-t)}\left(\int_0^{\tau-t} e^{-\delta_2 s}\,d\hat{B}_t(s)\right)^{n-i}\right.\right.\nonumber\\ & \qquad \left.\left.\left.\times \left( \sum_{k=1}^{N(\tau)} e^{-\delta_3 (T_k-t)} f(Y_k)\right)^{m} w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}} \,|\, \mathcal{G}_t \vee \{T_1>t\}\right]\right|\, T_1>t\right]\nonumber\\ & \quad = \sum_{i=0}^{n} {n \choose i} e^{-(\delta_1+(n-i)\delta_2+m\delta_3) t}E[B_{\delta_2}^{i} (t)1_{\{\hat{\tau}_0>t\}} \phi_{w,\delta_{123},n-i,m}(u+ct+\sigma B(t))\,|\,T_1>t]\nonumber\\ & \quad = \sum_{i=0}^{n} {n \choose i} e^{-(\delta_1+(n-i)\delta_2+m\delta_3) t}E[B_{\delta_2}^{i} (t)1_{\{\hat{\tau}_0>t\}} \phi_{w,\delta_{123},n-i,m}(u+ct+\sigma B(t))]. \end{align} In the third last step above, we have applied the tower property of conditional expectation and the fact that both  $B_{\delta _2}(t)$ and

$B_{\delta _2}(t)$ and  $1_{\{\hat {\tau }_0>t\}}$ are

$1_{\{\hat {\tau }_0>t\}}$ are  $\mathcal {G}_t$-measurable. Moreover, in the second last step, conditional on

$\mathcal {G}_t$-measurable. Moreover, in the second last step, conditional on  $\mathcal {G}_t \vee \{T_1>t\}$ and based on the memoryless property of the exponential arrival time

$\mathcal {G}_t \vee \{T_1>t\}$ and based on the memoryless property of the exponential arrival time  $T_1$, the surplus process at time

$T_1$, the surplus process at time  $t$ is “renewed” at level

$t$ is “renewed” at level  $u+ct+\sigma B(t)$ which is positive (almost surely) on the set

$u+ct+\sigma B(t)$ which is positive (almost surely) on the set  $\{\hat {\tau }_0>t\}$.

$\{\hat {\tau }_0>t\}$.

Next, we look at the integral term in (2.6). Again, given that  $T_1=s$, one must have

$T_1=s$, one must have  $\hat {\tau }_0>s$ on the set

$\hat {\tau }_0>s$ on the set  $\{\tau <\infty,U(\tau )<0\}$. Further distinguishing whether the first claim at time

$\{\tau <\infty,U(\tau )<0\}$. Further distinguishing whether the first claim at time  $s$ causes ruin leads to

$s$ causes ruin leads to

\begin{align} & \int_0^{t}\lambda e^{-\lambda s} E[e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}} \,|\, T_1=s]\,ds\nonumber\\ & \quad= \int_0^{t}\lambda e^{-\lambda s} E[e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)\nonumber\\ & \qquad \times 1_{\{\tau<\infty,U(\tau)<0\}}1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1\le u+cs+\sigma B(s) \}} \,|\, T_1=s]\,ds\nonumber\\ & \qquad +\int_0^{t}\lambda e^{-\lambda s} E[e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)\nonumber\\ & \qquad \times 1_{\{\tau<\infty,U(\tau)<0\}}1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1>u+cs+\sigma B(s) \}}\,|\, T_1=s]\,ds. \end{align}

\begin{align} & \int_0^{t}\lambda e^{-\lambda s} E[e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}} \,|\, T_1=s]\,ds\nonumber\\ & \quad= \int_0^{t}\lambda e^{-\lambda s} E[e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)\nonumber\\ & \qquad \times 1_{\{\tau<\infty,U(\tau)<0\}}1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1\le u+cs+\sigma B(s) \}} \,|\, T_1=s]\,ds\nonumber\\ & \qquad +\int_0^{t}\lambda e^{-\lambda s} E[e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)\nonumber\\ & \qquad \times 1_{\{\tau<\infty,U(\tau)<0\}}1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1>u+cs+\sigma B(s) \}}\,|\, T_1=s]\,ds. \end{align} Defining  $\mathcal {H}(Y_1)$ to be the sigma-field generated by the random variable

$\mathcal {H}(Y_1)$ to be the sigma-field generated by the random variable  $Y_1$, the expectation in the integrand of the first integral above can be obtained as

$Y_1$, the expectation in the integrand of the first integral above can be obtained as

\begin{align} & E\left[ e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|) 1_{\{\tau<\infty,U(\tau)<0\}}1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1\le u+cs+\sigma B(s) \}} \,|\, T_1=s\right]\nonumber\\ & \quad = E[ E[ e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)\nonumber\\ & \qquad \times 1_{\{\tau<\infty,U(\tau)<0\}}1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1\le u+cs+\sigma B(s) \}}\,|\,\mathcal{G}_s \vee \mathcal{H}(Y_1) \vee \{T_1=s\} ] \,|\, T_1=s]\nonumber\\ & \quad =E\left[ E\left[ e^{-\delta_1 \tau}\left(B_{\delta_2} (s)+\int_s^{\tau} e^{-\delta_2 v}\,dB(v)\right)^{n} \left( e^{-\delta_3 s} f(Y_1) + \sum_{k=2}^{N(\tau)} e^{-\delta_3 T_k}f(Y_k) \right)^{m} w(U(\tau^{-}),|U(\tau)|)\right.\right.\nonumber\\ & \qquad \left.\left.\left.\times 1_{\{\tau<\infty,U(\tau)<0\}}1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1\le u+cs+\sigma B(s) \}}\,|\,\mathcal{G}_s \vee \mathcal{H}(Y_1) \vee \{T_1=s\} \vphantom{\sum_{k=2}^{N(\tau)}}\right] \,\right| T_1=s\right]\nonumber\\ & \quad = \sum_{i=0}^{n} \sum_{j=0}^{m} {n \choose i} {m \choose j} e^{-(\delta_1+i\delta_2+m\delta_3 )s} E\left[B_{\delta_2}^{n-i} (s)f^{m-j}(Y_1) 1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1\le u+cs+\sigma B(s) \}}\vphantom{\sum_{k=2}^{N(\tau)}}\right.\nonumber\\ & \qquad \times E\left[ e^{-\delta_1 (\tau-s)}\left(\int_0^{\tau-s} e^{-\delta_2 v}\,d\hat{B}_s(v)\right)^{i} \left( \sum_{k=2}^{N(\tau)}e^{-\delta_3 (T_k-s)} f(Y_k) \right)^{j} w(U(\tau^{-}),|U(\tau)|)\right.\nonumber\\ & \qquad \left.\left.\left.\times 1_{\{\tau<\infty,U(\tau)<0\}}\,|\,\mathcal{G}_s \vee \mathcal{H}(Y_1) \vee \{T_1=s\} \vphantom{\sum_{k=2}^{N(\tau)}}\right] \right|\,T_1=s\right]\nonumber\\ & \quad = \sum_{i=0}^{n} \sum_{j=0}^{m} {n \choose i} {m \choose j} e^{-(\delta_1+i\delta_2+m\delta_3 )s} E[B_{\delta_2}^{n-i} (s)f^{m-j}(Y_1) 1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1\le u+cs+\sigma B(s) \}}\nonumber\\ & \qquad \times \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-Y_1) \,|\, T_1=s]\nonumber\\ & \quad = \sum_{i=0}^{n} \sum_{j=0}^{m} {n \choose i} {m \choose j} e^{-(\delta_1+i\delta_2+m\delta_3 )s} E[B_{\delta_2}^{n-i} (s)f^{m-j}(Y_1) 1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1\le u+cs+\sigma B(s) \}}\nonumber\\ & \qquad \times \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-Y_1) ]. \end{align}

\begin{align} & E\left[ e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|) 1_{\{\tau<\infty,U(\tau)<0\}}1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1\le u+cs+\sigma B(s) \}} \,|\, T_1=s\right]\nonumber\\ & \quad = E[ E[ e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)\nonumber\\ & \qquad \times 1_{\{\tau<\infty,U(\tau)<0\}}1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1\le u+cs+\sigma B(s) \}}\,|\,\mathcal{G}_s \vee \mathcal{H}(Y_1) \vee \{T_1=s\} ] \,|\, T_1=s]\nonumber\\ & \quad =E\left[ E\left[ e^{-\delta_1 \tau}\left(B_{\delta_2} (s)+\int_s^{\tau} e^{-\delta_2 v}\,dB(v)\right)^{n} \left( e^{-\delta_3 s} f(Y_1) + \sum_{k=2}^{N(\tau)} e^{-\delta_3 T_k}f(Y_k) \right)^{m} w(U(\tau^{-}),|U(\tau)|)\right.\right.\nonumber\\ & \qquad \left.\left.\left.\times 1_{\{\tau<\infty,U(\tau)<0\}}1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1\le u+cs+\sigma B(s) \}}\,|\,\mathcal{G}_s \vee \mathcal{H}(Y_1) \vee \{T_1=s\} \vphantom{\sum_{k=2}^{N(\tau)}}\right] \,\right| T_1=s\right]\nonumber\\ & \quad = \sum_{i=0}^{n} \sum_{j=0}^{m} {n \choose i} {m \choose j} e^{-(\delta_1+i\delta_2+m\delta_3 )s} E\left[B_{\delta_2}^{n-i} (s)f^{m-j}(Y_1) 1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1\le u+cs+\sigma B(s) \}}\vphantom{\sum_{k=2}^{N(\tau)}}\right.\nonumber\\ & \qquad \times E\left[ e^{-\delta_1 (\tau-s)}\left(\int_0^{\tau-s} e^{-\delta_2 v}\,d\hat{B}_s(v)\right)^{i} \left( \sum_{k=2}^{N(\tau)}e^{-\delta_3 (T_k-s)} f(Y_k) \right)^{j} w(U(\tau^{-}),|U(\tau)|)\right.\nonumber\\ & \qquad \left.\left.\left.\times 1_{\{\tau<\infty,U(\tau)<0\}}\,|\,\mathcal{G}_s \vee \mathcal{H}(Y_1) \vee \{T_1=s\} \vphantom{\sum_{k=2}^{N(\tau)}}\right] \right|\,T_1=s\right]\nonumber\\ & \quad = \sum_{i=0}^{n} \sum_{j=0}^{m} {n \choose i} {m \choose j} e^{-(\delta_1+i\delta_2+m\delta_3 )s} E[B_{\delta_2}^{n-i} (s)f^{m-j}(Y_1) 1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1\le u+cs+\sigma B(s) \}}\nonumber\\ & \qquad \times \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-Y_1) \,|\, T_1=s]\nonumber\\ & \quad = \sum_{i=0}^{n} \sum_{j=0}^{m} {n \choose i} {m \choose j} e^{-(\delta_1+i\delta_2+m\delta_3 )s} E[B_{\delta_2}^{n-i} (s)f^{m-j}(Y_1) 1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1\le u+cs+\sigma B(s) \}}\nonumber\\ & \qquad \times \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-Y_1) ]. \end{align} For now, we focus on the expectation term above. By conditioning on  $Y_1$ and using the independence between

$Y_1$ and using the independence between  $\mathcal {H}(Y_1)$ and

$\mathcal {H}(Y_1)$ and  $\mathcal {G}_s$, we get

$\mathcal {G}_s$, we get

\begin{align} & E\left[B_{\delta_2}^{n-i} (s)f^{m-j}(Y_1) 1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1\le u+cs+\sigma B(s) \}} \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-Y_1) \right]\nonumber\\ & \quad= \int_0^{\infty} E\left[B_{\delta_2}^{n-i} (s)f^{m-j}(y) 1_{\{\hat{\tau}_0>s\}} 1_{\{y\le u+cs+\sigma B(s) \}} \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-y)\right]p(y)\,dy\nonumber\\ & \quad= E\left[\int_0^{\infty} B_{\delta_2}^{n-i} (s)f^{m-j}(y) 1_{\{\hat{\tau}_0>s\}} 1_{\{y\le u+cs+\sigma B(s) \}} \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-y) p(y)\,dy\right]\nonumber\\ & \quad= E\left[B_{\delta_2}^{n-i} (s) 1_{\{\hat{\tau}_0>s\}} \int_0^{u+cs+\sigma B(s)} f^{m-j}(y) \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-y) p(y)\,dy\right]. \end{align}

\begin{align} & E\left[B_{\delta_2}^{n-i} (s)f^{m-j}(Y_1) 1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1\le u+cs+\sigma B(s) \}} \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-Y_1) \right]\nonumber\\ & \quad= \int_0^{\infty} E\left[B_{\delta_2}^{n-i} (s)f^{m-j}(y) 1_{\{\hat{\tau}_0>s\}} 1_{\{y\le u+cs+\sigma B(s) \}} \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-y)\right]p(y)\,dy\nonumber\\ & \quad= E\left[\int_0^{\infty} B_{\delta_2}^{n-i} (s)f^{m-j}(y) 1_{\{\hat{\tau}_0>s\}} 1_{\{y\le u+cs+\sigma B(s) \}} \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-y) p(y)\,dy\right]\nonumber\\ & \quad= E\left[B_{\delta_2}^{n-i} (s) 1_{\{\hat{\tau}_0>s\}} \int_0^{u+cs+\sigma B(s)} f^{m-j}(y) \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-y) p(y)\,dy\right]. \end{align} Note that the interchange of integration and expectation in the second last equality is due to Fubini's theorem as follows. Recall that the Gerber-Shiu functions  $\phi _{w,\delta _{123},i,j}(\cdot )$'s are assumed bounded (see Assumption 2) and integrals in the form of

$\phi _{w,\delta _{123},i,j}(\cdot )$'s are assumed bounded (see Assumption 2) and integrals in the form of  $\int _0^{\infty } f^{m-j}(y)p(y)\,dy$ are assumed finite (see Condition 1). Therefore, there exists

$\int _0^{\infty } f^{m-j}(y)p(y)\,dy$ are assumed finite (see Condition 1). Therefore, there exists  $L>0$ such that

$L>0$ such that

\begin{align} & \int_0^{\infty} |B_{\delta_2}^{n-i} (s)f^{m-j}(y) 1_{\{\hat{\tau}_0>s\}} 1_{\{y\le u+cs+\sigma B(s) \}} \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-y) p(y)|\,dy \nonumber\\ & \quad \leq L |B_{\delta_2}(s)|^{n-i} \end{align}

\begin{align} & \int_0^{\infty} |B_{\delta_2}^{n-i} (s)f^{m-j}(y) 1_{\{\hat{\tau}_0>s\}} 1_{\{y\le u+cs+\sigma B(s) \}} \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-y) p(y)|\,dy \nonumber\\ & \quad \leq L |B_{\delta_2}(s)|^{n-i} \end{align}for  $0\leq s \leq t$. Because

$0\leq s \leq t$. Because  $B_{\delta _2}(s)=\int _0^{s} e^{-\delta _2 v}\,dB(v)$ follows a normal distribution (with mean

$B_{\delta _2}(s)=\int _0^{s} e^{-\delta _2 v}\,dB(v)$ follows a normal distribution (with mean  $0$ and variance

$0$ and variance  $\int _0^{s} e^{-2\delta _2 v}\,dv$), the random variable

$\int _0^{s} e^{-2\delta _2 v}\,dv$), the random variable  $|B_{\delta _2}(s)|$ follows a half-normal distribution. For

$|B_{\delta _2}(s)|$ follows a half-normal distribution. For  $k\in \mathbb {N}^{+}$ (where

$k\in \mathbb {N}^{+}$ (where  $\mathbb {N}^{+}$ is the set of positive integers), its

$\mathbb {N}^{+}$ is the set of positive integers), its  $k$th moment is known to be bounded because

$k$th moment is known to be bounded because

\begin{equation} E[|B_{\delta_2}(s)|^{k}]= L^{*}_k \left(\int_0^{s} e^{{-}2\delta_2 v}\,dv\right)^{\frac{k}{2}} \end{equation}

\begin{equation} E[|B_{\delta_2}(s)|^{k}]= L^{*}_k \left(\int_0^{s} e^{{-}2\delta_2 v}\,dv\right)^{\frac{k}{2}} \end{equation}for some constant  $L^{*}_k$. Therefore, the expectation on the right-hand side of (2.11) is bounded for

$L^{*}_k$. Therefore, the expectation on the right-hand side of (2.11) is bounded for  $0\leq s \leq t$ and

$0\leq s \leq t$ and  $i=0,1,\ldots,n$, justifying the use of Fubini's theorem.

$i=0,1,\ldots,n$, justifying the use of Fubini's theorem.

Similarly, we omit the repetitive details and state that the expectation in the integrand of the second integral in (2.8) is given by

\begin{align} & E\left[e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}}1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1>u+cs+\sigma B(s) \}}\,|\, T_1=s\right]\nonumber\\ & \quad = E[ e^{-\delta_1 s}B_{\delta_2}^{n} (s)(e^{-\delta_3 s}f(Y_1))^{m} w(u+cs+\sigma B(s),Y_1-u-cs-\sigma B(s))1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1>u+cs+\sigma B(s) \}}]\nonumber\\ & \quad=e^{-(\delta_1+m\delta_3) s}E\left[B_{\delta_2}^{n} (s) 1_{\{\hat{\tau}_0>s\}} \int_{u+cs+\sigma B(s) }^{\infty} f^{m}(y) w(u+cs+\sigma B(s),y-u-cs-\sigma B(s)) p(y)\,dy\right], \end{align}

\begin{align} & E\left[e^{-\delta_1 \tau}B_{\delta_2}^{n} (\tau)Z_{\delta_3}^{m}(\tau)w(U(\tau^{-}),|U(\tau)|)1_{\{\tau<\infty,U(\tau)<0\}}1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1>u+cs+\sigma B(s) \}}\,|\, T_1=s\right]\nonumber\\ & \quad = E[ e^{-\delta_1 s}B_{\delta_2}^{n} (s)(e^{-\delta_3 s}f(Y_1))^{m} w(u+cs+\sigma B(s),Y_1-u-cs-\sigma B(s))1_{\{\hat{\tau}_0>s\}} 1_{\{Y_1>u+cs+\sigma B(s) \}}]\nonumber\\ & \quad=e^{-(\delta_1+m\delta_3) s}E\left[B_{\delta_2}^{n} (s) 1_{\{\hat{\tau}_0>s\}} \int_{u+cs+\sigma B(s) }^{\infty} f^{m}(y) w(u+cs+\sigma B(s),y-u-cs-\sigma B(s)) p(y)\,dy\right], \end{align}where Condition 2 has been used.

Using (2.7)–(2.10) and (2.13), it can be seen that (2.6) becomes

\begin{align} & \phi_{w,\delta_{123},n,m}(u)\nonumber\\ & \quad = \sum_{i=0}^{n} {n \choose i} e^{-(\lambda+\delta_1+(n-i)\delta_2+m\delta_3) t}E\left[B_{\delta_2}^{i} (t)1_{\{\hat{\tau}_0>t\}} \phi_{w,\delta_{123},n-i,m}(u+ct+\sigma B(t))\right]\nonumber\\ & \qquad +\lambda \sum_{i=0}^{n} \sum_{j=0}^{m} {n \choose i} {m \choose j} \int_0^{t} e^{-(\lambda+\delta_1+i\delta_2+m\delta_3 )s} \nonumber\\ & \qquad \times E\left[B_{\delta_2}^{n-i} (s) 1_{\{\hat{\tau}_0>s\}} \int_0^{u+cs+\sigma B(s)} f^{m-j}(y) \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-y) p(y)\,dy\right]ds\nonumber\\ & \qquad +\lambda \int_0^{t} e^{-(\lambda+\delta_1+m\delta_3) s}\nonumber\\ & \qquad \times E\left[B_{\delta_2}^{n} (s) 1_{\{\hat{\tau}_0>s\}} \int_{u+cs+\sigma B(s) }^{\infty} f^{m}(y) w(u+cs+\sigma B(s),y-u-cs-\sigma B(s)) p(y)\,dy\right]ds. \end{align}

\begin{align} & \phi_{w,\delta_{123},n,m}(u)\nonumber\\ & \quad = \sum_{i=0}^{n} {n \choose i} e^{-(\lambda+\delta_1+(n-i)\delta_2+m\delta_3) t}E\left[B_{\delta_2}^{i} (t)1_{\{\hat{\tau}_0>t\}} \phi_{w,\delta_{123},n-i,m}(u+ct+\sigma B(t))\right]\nonumber\\ & \qquad +\lambda \sum_{i=0}^{n} \sum_{j=0}^{m} {n \choose i} {m \choose j} \int_0^{t} e^{-(\lambda+\delta_1+i\delta_2+m\delta_3 )s} \nonumber\\ & \qquad \times E\left[B_{\delta_2}^{n-i} (s) 1_{\{\hat{\tau}_0>s\}} \int_0^{u+cs+\sigma B(s)} f^{m-j}(y) \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-y) p(y)\,dy\right]ds\nonumber\\ & \qquad +\lambda \int_0^{t} e^{-(\lambda+\delta_1+m\delta_3) s}\nonumber\\ & \qquad \times E\left[B_{\delta_2}^{n} (s) 1_{\{\hat{\tau}_0>s\}} \int_{u+cs+\sigma B(s) }^{\infty} f^{m}(y) w(u+cs+\sigma B(s),y-u-cs-\sigma B(s)) p(y)\,dy\right]ds. \end{align}With the help of the L'Hôpital's rule, we would like to consider the limits

\begin{align} & \lim_{t \to 0^{+}} \frac{1}{t}\int_0^{t} e^{-(\lambda+\delta_1+i\delta_2+m\delta_3 )s} \nonumber\\ & \qquad \times E\left[B_{\delta_2}^{n-i} (s) 1_{\{\hat{\tau}_0>s\}} \int_0^{u+cs+\sigma B(s)} f^{m-j}(y) \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-y) p(y)\,dy\right]ds \nonumber\\ & \quad = \lim_{t \to 0^{+}} E\left[B_{\delta_2}^{n-i} (t) 1_{\{\hat{\tau}_0>t\}} \int_0^{u+ct+\sigma B(t)} f^{m-j}(y) \phi_{w,\delta_{123},i,j}(u+ct+\sigma B(t)-y) p(y)\,dy\right] \end{align}

\begin{align} & \lim_{t \to 0^{+}} \frac{1}{t}\int_0^{t} e^{-(\lambda+\delta_1+i\delta_2+m\delta_3 )s} \nonumber\\ & \qquad \times E\left[B_{\delta_2}^{n-i} (s) 1_{\{\hat{\tau}_0>s\}} \int_0^{u+cs+\sigma B(s)} f^{m-j}(y) \phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-y) p(y)\,dy\right]ds \nonumber\\ & \quad = \lim_{t \to 0^{+}} E\left[B_{\delta_2}^{n-i} (t) 1_{\{\hat{\tau}_0>t\}} \int_0^{u+ct+\sigma B(t)} f^{m-j}(y) \phi_{w,\delta_{123},i,j}(u+ct+\sigma B(t)-y) p(y)\,dy\right] \end{align}and

\begin{align} & \lim_{t \to 0^{+}} \frac{1}{t} \int_0^{t} e^{-(\lambda+\delta_1+m\delta_3) s}\nonumber\\ & \qquad \times E\left[B_{\delta_2}^{n} (s) 1_{\{\hat{\tau}_0>s\}} \int_{u+cs+\sigma B(s) }^{\infty} f^{m}(y) w(u+cs+\sigma B(s),y-u-cs-\sigma B(s)) p(y)\,dy\right]ds\nonumber\\ & \quad = \lim_{t \to 0^{+}} E\left[B_{\delta_2}^{n} (t) 1_{\{\hat{\tau}_0>t\}} \int_{u+ct+\sigma B(t) }^{\infty} f^{m}(y) w(u+ct+\sigma B(t),y-u-ct-\sigma B(t)) p(y)\,dy\right]. \end{align}

\begin{align} & \lim_{t \to 0^{+}} \frac{1}{t} \int_0^{t} e^{-(\lambda+\delta_1+m\delta_3) s}\nonumber\\ & \qquad \times E\left[B_{\delta_2}^{n} (s) 1_{\{\hat{\tau}_0>s\}} \int_{u+cs+\sigma B(s) }^{\infty} f^{m}(y) w(u+cs+\sigma B(s),y-u-cs-\sigma B(s)) p(y)\,dy\right]ds\nonumber\\ & \quad = \lim_{t \to 0^{+}} E\left[B_{\delta_2}^{n} (t) 1_{\{\hat{\tau}_0>t\}} \int_{u+ct+\sigma B(t) }^{\infty} f^{m}(y) w(u+ct+\sigma B(t),y-u-ct-\sigma B(t)) p(y)\,dy\right]. \end{align}To evaluate (2.15), we can follow the discussions subsequent to (2.10) and note also that (2.11) implies

\begin{equation} \left| B_{\delta_2}^{n-i}(s) 1_{\{\hat{\tau}_0>s\}} \int_0^{u+cs+\sigma B(s)}f^{m-j}(y)\phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-y)p(y)\,dy \right| \leq L |B_{\delta_2}(s)|^{n-i} \end{equation}

\begin{equation} \left| B_{\delta_2}^{n-i}(s) 1_{\{\hat{\tau}_0>s\}} \int_0^{u+cs+\sigma B(s)}f^{m-j}(y)\phi_{w,\delta_{123},i,j}(u+cs+\sigma B(s)-y)p(y)\,dy \right| \leq L |B_{\delta_2}(s)|^{n-i} \end{equation}for  $0\leq s \leq t$. Utilizing (2.12) for

$0\leq s \leq t$. Utilizing (2.12) for  $k\in \mathbb {N}^{+}$, one has

$k\in \mathbb {N}^{+}$, one has

$$\lim_{t \to 0^{+}} E[|B_{\delta_2}(t)|^{n-i}] =0=E \left[\lim_{t \to 0^{+}} |B_{\delta_2}(t)|^{n-i}\right],$$

$$\lim_{t \to 0^{+}} E[|B_{\delta_2}(t)|^{n-i}] =0=E \left[\lim_{t \to 0^{+}} |B_{\delta_2}(t)|^{n-i}\right],$$for  $i< n$ where we have used the fact that

$i< n$ where we have used the fact that  $B_{\delta _2}(t)$ is continuous in

$B_{\delta _2}(t)$ is continuous in  $t\ge 0$ and

$t\ge 0$ and  $B_{\delta _2}(0)=0$ in the last equality. When

$B_{\delta _2}(0)=0$ in the last equality. When  $i=n$, the right-hand side of (2.17) is equal to the constant

$i=n$, the right-hand side of (2.17) is equal to the constant  $L$. Consolidating these results for

$L$. Consolidating these results for  $i\le n$, noting that

$i\le n$, noting that  $\hat {\tau }_0>0$ almost surely given

$\hat {\tau }_0>0$ almost surely given  $u>0$ and utilizing the generalized dominated convergence theorem (see, e.g., [Reference Billingsley3, Prob. 16.4]), we find that

$u>0$ and utilizing the generalized dominated convergence theorem (see, e.g., [Reference Billingsley3, Prob. 16.4]), we find that

\begin{align} & \lim_{t \to 0^{+}}E\left[B_{\delta_2}^{n-i}(t) 1_{\{\hat{\tau}_0>t\}} \int_0^{u+ct+\sigma B(t)}f^{m-j}(y)\phi_{w,\delta_{123},i,j}(u+ct+\sigma B(t)-y)p(y)\,dy\right] \nonumber\\ & \quad =E\left[\lim_{t \to 0^{+}}B_{\delta_2}^{n-i}(t) 1_{\{\hat{\tau}_0>t\}} \int_0^{u+ct+\sigma B(t)}f^{m-j}(y)\phi_{w,\delta_{123},i,j}(u+ct+\sigma B(t)-y)p(y)\,dy\right]\nonumber\\ & \quad =1_{\{i=n\}}\int_0^{u}f^{m-j}(y)\phi_{w,\delta_{123},n,j}(u-y)p(y)\,dy. \end{align}

\begin{align} & \lim_{t \to 0^{+}}E\left[B_{\delta_2}^{n-i}(t) 1_{\{\hat{\tau}_0>t\}} \int_0^{u+ct+\sigma B(t)}f^{m-j}(y)\phi_{w,\delta_{123},i,j}(u+ct+\sigma B(t)-y)p(y)\,dy\right] \nonumber\\ & \quad =E\left[\lim_{t \to 0^{+}}B_{\delta_2}^{n-i}(t) 1_{\{\hat{\tau}_0>t\}} \int_0^{u+ct+\sigma B(t)}f^{m-j}(y)\phi_{w,\delta_{123},i,j}(u+ct+\sigma B(t)-y)p(y)\,dy\right]\nonumber\\ & \quad =1_{\{i=n\}}\int_0^{u}f^{m-j}(y)\phi_{w,\delta_{123},n,j}(u-y)p(y)\,dy. \end{align}Moreover, under Condition 2, it can be shown that (2.16) is given by

\begin{align} & \lim_{t \to 0^{+}}E\left[B_{\delta_2}^{n}(t) 1_{\{\hat{\tau}_0>t\}} \int_{u+ct+\sigma B(t)}^{\infty} f^{m}(y)w(u+ct+\sigma B(t),y-u-ct-\sigma B(t))p(y)\,dy\right]\nonumber\\ & \quad = 1_{\{n=0\}} \int_u^{\infty} f^{m}(y)w(u,y-u)p(y)\,dy. \end{align}

\begin{align} & \lim_{t \to 0^{+}}E\left[B_{\delta_2}^{n}(t) 1_{\{\hat{\tau}_0>t\}} \int_{u+ct+\sigma B(t)}^{\infty} f^{m}(y)w(u+ct+\sigma B(t),y-u-ct-\sigma B(t))p(y)\,dy\right]\nonumber\\ & \quad = 1_{\{n=0\}} \int_u^{\infty} f^{m}(y)w(u,y-u)p(y)\,dy. \end{align}In light of the first term in (2.14), we also apply similar arguments to obtain

\begin{align} & \lim_{t \to 0^{+}}E[B_{\delta_2}^{i} (t)1_{\{\hat{\tau}_0>t\}} \phi_{w,\delta_{123},n-i,m}(u+ct+\sigma B(t))]\nonumber\\ & \quad =E\left[\lim_{t \to 0^{+}}B_{\delta_2}^{i} (t)1_{\{\hat{\tau}_0>t\}} \phi_{w,\delta_{123},n-i,m}(u+ct+\sigma B(t))\right]\nonumber\\ & \quad =1_{\{i=0\}} \phi_{w,\delta_{123},n,m}(u). \end{align}

\begin{align} & \lim_{t \to 0^{+}}E[B_{\delta_2}^{i} (t)1_{\{\hat{\tau}_0>t\}} \phi_{w,\delta_{123},n-i,m}(u+ct+\sigma B(t))]\nonumber\\ & \quad =E\left[\lim_{t \to 0^{+}}B_{\delta_2}^{i} (t)1_{\{\hat{\tau}_0>t\}} \phi_{w,\delta_{123},n-i,m}(u+ct+\sigma B(t))\right]\nonumber\\ & \quad =1_{\{i=0\}} \phi_{w,\delta_{123},n,m}(u). \end{align} Now, we proceed by rearranging the terms in (2.14), dividing both sides by  $t$ and taking the limit

$t$ and taking the limit  $t \to 0^{+}$. Applying (2.18)–(2.20) and further noting that

$t \to 0^{+}$. Applying (2.18)–(2.20) and further noting that  $e^{-(\lambda +\delta _1+(n-i)\delta _2+m\delta _3)t}=1-(\lambda +\delta _1+(n-i)\delta _2+m\delta _3)t+o(t)$, we arrive at

$e^{-(\lambda +\delta _1+(n-i)\delta _2+m\delta _3)t}=1-(\lambda +\delta _1+(n-i)\delta _2+m\delta _3)t+o(t)$, we arrive at

\begin{align} & \lim_{t \to 0^{+}}\frac{E[\phi_{w,\delta_{123},n,m}(u+ct+\sigma B(t))]-\phi_{w,\delta_{123},n,m}(u)}{t}\nonumber\\ & \quad -\lim_{t \to 0^{+}}\frac{E[\phi_{w,\delta_{123},n,m}(u+ct+\sigma B(t)) (1-1_{\{\hat{\tau}_0>t\}})]}{t}\nonumber\\ & \quad +\sum_{i=1}^{n} {n \choose i} \lim_{t \to 0^{+}} \frac{E[B_{\delta_2}^{i}(t)\phi_{w,\delta_{123},n-i,m}(u+ct+\sigma B(t))1_{\{\hat{\tau}_0>t\}}]}{t}\nonumber\\ & \quad-(\lambda+\delta_1 +n\delta_2+m\delta_3)\phi_{w,\delta_{123},n,m}(u)\nonumber\\ & \quad+\lambda \sum_{j=0}^{m} {m \choose j}\int_0^{u} f^{m-j}(y)\phi_{w,\delta_{123},n,j}(u-y)p(y)\,dy\nonumber\\ & \quad +\lambda 1_{\{n=0\}} \int_u^{\infty} f^{m}(y)w(u,y-u)p(y)\,dy =0. \end{align}

\begin{align} & \lim_{t \to 0^{+}}\frac{E[\phi_{w,\delta_{123},n,m}(u+ct+\sigma B(t))]-\phi_{w,\delta_{123},n,m}(u)}{t}\nonumber\\ & \quad -\lim_{t \to 0^{+}}\frac{E[\phi_{w,\delta_{123},n,m}(u+ct+\sigma B(t)) (1-1_{\{\hat{\tau}_0>t\}})]}{t}\nonumber\\ & \quad +\sum_{i=1}^{n} {n \choose i} \lim_{t \to 0^{+}} \frac{E[B_{\delta_2}^{i}(t)\phi_{w,\delta_{123},n-i,m}(u+ct+\sigma B(t))1_{\{\hat{\tau}_0>t\}}]}{t}\nonumber\\ & \quad-(\lambda+\delta_1 +n\delta_2+m\delta_3)\phi_{w,\delta_{123},n,m}(u)\nonumber\\ & \quad+\lambda \sum_{j=0}^{m} {m \choose j}\int_0^{u} f^{m-j}(y)\phi_{w,\delta_{123},n,j}(u-y)p(y)\,dy\nonumber\\ & \quad +\lambda 1_{\{n=0\}} \int_u^{\infty} f^{m}(y)w(u,y-u)p(y)\,dy =0. \end{align} The three limits in the above equation will be evaluated as follows. First, as  $\phi _{w,\delta _{123},n,m}(\cdot )$ is assumed twice continuously differentiable as in Assumption 1, it follows from, for example, Tsai and Willmot [Reference Tsai and Willmot34, Sect. 2] that the first limit in the above equation is given by

$\phi _{w,\delta _{123},n,m}(\cdot )$ is assumed twice continuously differentiable as in Assumption 1, it follows from, for example, Tsai and Willmot [Reference Tsai and Willmot34, Sect. 2] that the first limit in the above equation is given by

\begin{equation} \lim_{t \to 0^{+}}\frac{E[\phi_{w,\delta_{123},n,m}(u+ct+\sigma B(t))]-\phi_{w,\delta_{123},n,m}(u)}{t}=\frac{\sigma^{2}}{2} \phi_{w,\delta_{123},n,m}''(u)+c\phi_{w,\delta_{123},n,m}'(u). \end{equation}

\begin{equation} \lim_{t \to 0^{+}}\frac{E[\phi_{w,\delta_{123},n,m}(u+ct+\sigma B(t))]-\phi_{w,\delta_{123},n,m}(u)}{t}=\frac{\sigma^{2}}{2} \phi_{w,\delta_{123},n,m}''(u)+c\phi_{w,\delta_{123},n,m}'(u). \end{equation} To derive the second limit in (2.21), the boundedness of  $\phi _{w,\delta _{123},n,m}(\cdot )$ on

$\phi _{w,\delta _{123},n,m}(\cdot )$ on  $[0,\infty )$ in Assumption 2 (together with the convention that

$[0,\infty )$ in Assumption 2 (together with the convention that  $\phi _{w,\delta _{123},n,m}(\cdot )=0$ on

$\phi _{w,\delta _{123},n,m}(\cdot )=0$ on  $(-\infty,0)$ in connection to the trivial boundary condition (2.40)) assures that there exists some

$(-\infty,0)$ in connection to the trivial boundary condition (2.40)) assures that there exists some  $L^{\ast }>0$ such that

$L^{\ast }>0$ such that  $|\phi _{w,\delta _{123},n,m}(u+ct+\sigma B(t)) (1-1_{\{\hat {\tau }_0>t\}})|\le L^{\ast } (1-1_{\{\hat {\tau }_0>t\}})$. Thus, we have

$|\phi _{w,\delta _{123},n,m}(u+ct+\sigma B(t)) (1-1_{\{\hat {\tau }_0>t\}})|\le L^{\ast } (1-1_{\{\hat {\tau }_0>t\}})$. Thus, we have

\begin{align} \lim_{t \to 0^{+}}\left|\frac{E[\phi_{w,\delta_{123},n,m}(u+ct+\sigma B(t)) (1-1_{\{\hat{\tau}_0>t\}}) ]}{t}\right| & \leq L^{{\ast}} \lim_{t \to 0^{+}} \frac{E[1-1_{\{\hat{\tau}_0>t\}}]}{t}\nonumber\\ & = L^{{\ast}} \lim_{t \to 0^{+}} \frac{\Pr\{\hat{\tau}_0 \leq t\}}{t}\nonumber\\ & = L^{{\ast}} \lim_{t \to 0^{+}} \frac{\Pr\{\inf_{0 \leq s \leq t} (cs+\sigma B(s))\leq{-}u\}}{t}\nonumber\\ & = 0, \end{align}

\begin{align} \lim_{t \to 0^{+}}\left|\frac{E[\phi_{w,\delta_{123},n,m}(u+ct+\sigma B(t)) (1-1_{\{\hat{\tau}_0>t\}}) ]}{t}\right| & \leq L^{{\ast}} \lim_{t \to 0^{+}} \frac{E[1-1_{\{\hat{\tau}_0>t\}}]}{t}\nonumber\\ & = L^{{\ast}} \lim_{t \to 0^{+}} \frac{\Pr\{\hat{\tau}_0 \leq t\}}{t}\nonumber\\ & = L^{{\ast}} \lim_{t \to 0^{+}} \frac{\Pr\{\inf_{0 \leq s \leq t} (cs+\sigma B(s))\leq{-}u\}}{t}\nonumber\\ & = 0, \end{align}where the last step follows from the last equality on p. 147 of Jeanblanc et al. [Reference Jeanblanc, Yor and Chesney24] concerning an explicit expression for  $\Pr \{\inf _{0 \leq s \leq t} (cs+\sigma B(s))\leq -u\}$. The above implies

$\Pr \{\inf _{0 \leq s \leq t} (cs+\sigma B(s))\leq -u\}$. The above implies

\begin{equation} \lim_{t \to 0^{+}}\frac{E[\phi_{w,\delta_{123},n,m}(u+ct+\sigma B(t)) (1-1_{\{\hat{\tau}_0>t\}}) ]}{t}=0. \end{equation}

\begin{equation} \lim_{t \to 0^{+}}\frac{E[\phi_{w,\delta_{123},n,m}(u+ct+\sigma B(t)) (1-1_{\{\hat{\tau}_0>t\}}) ]}{t}=0. \end{equation} It requires much more efforts to determine the third limit in (2.21). Since  $B_{\delta _2}(t)=\int _0^{t} e^{-\delta _2s}\,dB(s)$, it is immediate that

$B_{\delta _2}(t)=\int _0^{t} e^{-\delta _2s}\,dB(s)$, it is immediate that  $dB_{\delta _2}(s)=e^{-\delta _2 s}\,dB(s)$ and hence

$dB_{\delta _2}(s)=e^{-\delta _2 s}\,dB(s)$ and hence  $dB_{\delta _2}(s)\,dB_{\delta _2}(s)=e^{-2\delta _2 s}\,ds$. For

$dB_{\delta _2}(s)\,dB_{\delta _2}(s)=e^{-2\delta _2 s}\,ds$. For  $i \geq 2$, use of Itô's lemma gives rise to

$i \geq 2$, use of Itô's lemma gives rise to

\begin{align*} dB_{\delta_2}^{i}(s)& =i B_{\delta_2}^{i-1}(s)\,dB_{\delta_2}(s)+\tfrac{1}{2}i(i-1)B_{\delta_2}^{i-2}(s)\,dB_{\delta_2}(s)\,dB_{\delta_2}(s)\\ & =ie^{-\delta_2 s} B_{\delta_2}^{i-1}(s)\,dB(s)+\tfrac{1}{2}i(i-1)e^{{-}2\delta_2 s}B_{\delta_2}^{i-2}(s)\,ds. \end{align*}

\begin{align*} dB_{\delta_2}^{i}(s)& =i B_{\delta_2}^{i-1}(s)\,dB_{\delta_2}(s)+\tfrac{1}{2}i(i-1)B_{\delta_2}^{i-2}(s)\,dB_{\delta_2}(s)\,dB_{\delta_2}(s)\\ & =ie^{-\delta_2 s} B_{\delta_2}^{i-1}(s)\,dB(s)+\tfrac{1}{2}i(i-1)e^{{-}2\delta_2 s}B_{\delta_2}^{i-2}(s)\,ds. \end{align*} Applying Itô's lemma to the term  $\phi _{w,\delta _{123},n-i,m}(u+cs+\sigma B(s))$ on the set

$\phi _{w,\delta _{123},n-i,m}(u+cs+\sigma B(s))$ on the set  $\{\hat {\tau }_0>t\}$ (because of twice continuous differentiability of

$\{\hat {\tau }_0>t\}$ (because of twice continuous differentiability of  $\phi _{w,\delta _{123},n-i,m}(\cdot )$ on

$\phi _{w,\delta _{123},n-i,m}(\cdot )$ on  $[0,\infty )$ as in Assumption 1 and the fact that

$[0,\infty )$ as in Assumption 1 and the fact that  $\inf _{0 \leq s \leq t}(u+cs+\sigma B(s))>0$ on

$\inf _{0 \leq s \leq t}(u+cs+\sigma B(s))>0$ on  $\{\hat {\tau }_0>t\}$) yields

$\{\hat {\tau }_0>t\}$) yields

\begin{align*} & d\phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s))\\ & \quad =\left(c\phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))+\frac{\sigma^{2}}{2}\phi_{w,\delta_{123},n-i,m}''(u+cs+\sigma B(s))\right)\,ds\\ & \qquad +\sigma \phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s)) \,dB(s). \end{align*}

\begin{align*} & d\phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s))\\ & \quad =\left(c\phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))+\frac{\sigma^{2}}{2}\phi_{w,\delta_{123},n-i,m}''(u+cs+\sigma B(s))\right)\,ds\\ & \qquad +\sigma \phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s)) \,dB(s). \end{align*} With these two results, for  $i=1,2,\ldots,n$ we have by Itô's product rule that

$i=1,2,\ldots,n$ we have by Itô's product rule that

\begin{align*} & d\left(B_{\delta_2}^{i}(s) \phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s))\right)\\ & \quad =B_{\delta_2}^{i}(s)\,d\phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s)) +\phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s))\,dB_{\delta_2}^{i}(s) \\ & \qquad +d\phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s))\,dB_{\delta_2}^{i}(s)\\ & \quad = B_{\delta_2}^{i}(s) \left(c\phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))+\frac{\sigma^{2}}{2}\phi_{w,\delta_{123},n-i,m}''(u+cs+\sigma B(s))\right)\,ds \\ & \qquad + \sigma B_{\delta_2}^{i}(s) \phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s)) \,dB(s)\\ & \qquad +\phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s)) \left(ie^{-\delta_2 s} B_{\delta_2}^{i-1}(s)\,dB(s)+\frac{1}{2}i(i-1)1_{\{i \geq 2\}}e^{{-}2\delta_2 s}B_{\delta_2}^{i-2}(s)\,ds\right)\\ & \qquad +i \sigma e^{-\delta_2 s} B_{\delta_2}^{i-1}(s) \phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))\,ds. \end{align*}

\begin{align*} & d\left(B_{\delta_2}^{i}(s) \phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s))\right)\\ & \quad =B_{\delta_2}^{i}(s)\,d\phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s)) +\phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s))\,dB_{\delta_2}^{i}(s) \\ & \qquad +d\phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s))\,dB_{\delta_2}^{i}(s)\\ & \quad = B_{\delta_2}^{i}(s) \left(c\phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))+\frac{\sigma^{2}}{2}\phi_{w,\delta_{123},n-i,m}''(u+cs+\sigma B(s))\right)\,ds \\ & \qquad + \sigma B_{\delta_2}^{i}(s) \phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s)) \,dB(s)\\ & \qquad +\phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s)) \left(ie^{-\delta_2 s} B_{\delta_2}^{i-1}(s)\,dB(s)+\frac{1}{2}i(i-1)1_{\{i \geq 2\}}e^{{-}2\delta_2 s}B_{\delta_2}^{i-2}(s)\,ds\right)\\ & \qquad +i \sigma e^{-\delta_2 s} B_{\delta_2}^{i-1}(s) \phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))\,ds. \end{align*} By rewriting this in integral form, multiplying by  $1_{\{\hat {\tau }_0>t\}}$ and taking expectation, we obtain

$1_{\{\hat {\tau }_0>t\}}$ and taking expectation, we obtain

\begin{align} & E[B_{\delta_2}^{i}(t) \phi_{w,\delta_{123},n-i,m}(u+ct+\sigma B(t))1_{\{\hat{\tau}_0>t\}}]\nonumber\\ & \quad =E\left[1_{\{\hat{\tau}_0>t\}}\int_0^{t} B_{\delta_2}^{i}(s) \left(c\phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))\right.\right.\nonumber\\ & \qquad \left.\left.+\frac{\sigma^{2}}{2}\phi_{w,\delta_{123},n-i,m}''(u+cs+\sigma B(s))\right)\,ds\right]\nonumber\\ & \qquad +\sigma E\left[1_{\{\hat{\tau}_0>t\}}\int_0^{t} B_{\delta_2}^{i}(s) \phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s)) \,dB(s) \right]\nonumber\\ & \qquad +iE\left[1_{\{\hat{\tau}_0>t\}}\int_0^{t} \phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s)) e^{-\delta_2 s} B_{\delta_2}^{i-1}(s) \,dB(s) \right]\nonumber\\ & \qquad +\frac{1}{2}i(i-1)1_{\{i \geq 2\}} E\left[1_{\{\hat{\tau}_0>t\}}\int_0^{t} \phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s))e^{{-}2\delta_2s}B_{\delta_2}^{i-2}(s)\,ds\right]\nonumber\\ & \qquad +i \sigma E\left[1_{\{\hat{\tau}_0>t\}} \int_0^{t} e^{-\delta_2 s} B_{\delta_2}^{i-1}(s) \phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))\,ds\right]. \end{align}

\begin{align} & E[B_{\delta_2}^{i}(t) \phi_{w,\delta_{123},n-i,m}(u+ct+\sigma B(t))1_{\{\hat{\tau}_0>t\}}]\nonumber\\ & \quad =E\left[1_{\{\hat{\tau}_0>t\}}\int_0^{t} B_{\delta_2}^{i}(s) \left(c\phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))\right.\right.\nonumber\\ & \qquad \left.\left.+\frac{\sigma^{2}}{2}\phi_{w,\delta_{123},n-i,m}''(u+cs+\sigma B(s))\right)\,ds\right]\nonumber\\ & \qquad +\sigma E\left[1_{\{\hat{\tau}_0>t\}}\int_0^{t} B_{\delta_2}^{i}(s) \phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s)) \,dB(s) \right]\nonumber\\ & \qquad +iE\left[1_{\{\hat{\tau}_0>t\}}\int_0^{t} \phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s)) e^{-\delta_2 s} B_{\delta_2}^{i-1}(s) \,dB(s) \right]\nonumber\\ & \qquad +\frac{1}{2}i(i-1)1_{\{i \geq 2\}} E\left[1_{\{\hat{\tau}_0>t\}}\int_0^{t} \phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s))e^{{-}2\delta_2s}B_{\delta_2}^{i-2}(s)\,ds\right]\nonumber\\ & \qquad +i \sigma E\left[1_{\{\hat{\tau}_0>t\}} \int_0^{t} e^{-\delta_2 s} B_{\delta_2}^{i-1}(s) \phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))\,ds\right]. \end{align} As we will be dividing the above expression by  $t$ and letting

$t$ and letting  $t \to 0^{+}$ according to (2.21), we first deal with the first expectation on the right-hand side. Noting that

$t \to 0^{+}$ according to (2.21), we first deal with the first expectation on the right-hand side. Noting that  $\phi _{w,\delta _{123},n-i,m}'(\cdot )$ and

$\phi _{w,\delta _{123},n-i,m}'(\cdot )$ and  $\phi _{w,\delta _{123},n-i,m}''(\cdot )$ are bounded according to Assumption 2 and the moments of

$\phi _{w,\delta _{123},n-i,m}''(\cdot )$ are bounded according to Assumption 2 and the moments of  $|B_{\delta _2}(s)|$ (and hence,

$|B_{\delta _2}(s)|$ (and hence,  $\int _0^{t} E[|B_{\delta _2}^{i}(s)|]\,ds$) are finite, we apply Fubini's theorem to arrive at

$\int _0^{t} E[|B_{\delta _2}^{i}(s)|]\,ds$) are finite, we apply Fubini's theorem to arrive at

\begin{align*} & \lim_{t \to 0^{+}} \left|\frac{E[1_{\{\hat{\tau}_0>t\}}\int_0^{t} B_{\delta_2}^{i}(s) (c\phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))+\frac{\sigma^{2}}{2}\phi_{w,\delta_{123},n-i,m}''(u+cs+\sigma B(s)))\,ds ]}{t}\right|\\ & \quad \leq \lim_{t \to 0^{+}} \frac{\int_0^{t} E[|B_{\delta_2}^{i}(s) (c\phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))+\frac{\sigma^{2}}{2}\phi_{w,\delta_{123},n-i,m}''(u+cs+\sigma B(s)))|]\,ds}{t}\\ & \quad =\lim_{t \to 0^{+}} E\left[\left|B_{\delta_2}^{i}(t) \left(c\phi_{w,\delta_{123},n-i,m}'(u+ct+\sigma B(t))+\frac{\sigma^{2}}{2}\phi_{w,\delta_{123},n-i,m}''(u+ct+\sigma B(t))\right)\right|\right]\\ & \quad=0. \end{align*}

\begin{align*} & \lim_{t \to 0^{+}} \left|\frac{E[1_{\{\hat{\tau}_0>t\}}\int_0^{t} B_{\delta_2}^{i}(s) (c\phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))+\frac{\sigma^{2}}{2}\phi_{w,\delta_{123},n-i,m}''(u+cs+\sigma B(s)))\,ds ]}{t}\right|\\ & \quad \leq \lim_{t \to 0^{+}} \frac{\int_0^{t} E[|B_{\delta_2}^{i}(s) (c\phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))+\frac{\sigma^{2}}{2}\phi_{w,\delta_{123},n-i,m}''(u+cs+\sigma B(s)))|]\,ds}{t}\\ & \quad =\lim_{t \to 0^{+}} E\left[\left|B_{\delta_2}^{i}(t) \left(c\phi_{w,\delta_{123},n-i,m}'(u+ct+\sigma B(t))+\frac{\sigma^{2}}{2}\phi_{w,\delta_{123},n-i,m}''(u+ct+\sigma B(t))\right)\right|\right]\\ & \quad=0. \end{align*} Note that we have also used generalized dominated convergence theorem (similar to the proof of (2.18)) and the fact that  $B_{\delta _2}^{i}(0)=0$ (as

$B_{\delta _2}^{i}(0)=0$ (as  $i$ starts from 1). The inequality above implies

$i$ starts from 1). The inequality above implies

\begin{equation} \lim_{t \to 0^{+}}\frac{E[1_{\{\hat{\tau}_0>t\}}\int_0^{t} B_{\delta_2}^{i}(s) (c\phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))+\frac{\sigma^{2}}{2}\phi_{w,\delta_{123},n-i,m}''(u+cs+\sigma B(s)))\,ds]}{t}=0. \end{equation}

\begin{equation} \lim_{t \to 0^{+}}\frac{E[1_{\{\hat{\tau}_0>t\}}\int_0^{t} B_{\delta_2}^{i}(s) (c\phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))+\frac{\sigma^{2}}{2}\phi_{w,\delta_{123},n-i,m}''(u+cs+\sigma B(s)))\,ds]}{t}=0. \end{equation} Similarly, for the fourth expectation in (2.25), one has for  $i>2$ that

$i>2$ that

\begin{equation} \lim_{t \to 0^{+}} \frac{E[1_{\{\hat{\tau}_0>t\}}\int_0^{t} \phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s))e^{{-}2\delta_2 s}B_{\delta_2}^{i-2}(s)\,ds]}{t} =0, \end{equation}

\begin{equation} \lim_{t \to 0^{+}} \frac{E[1_{\{\hat{\tau}_0>t\}}\int_0^{t} \phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s))e^{{-}2\delta_2 s}B_{\delta_2}^{i-2}(s)\,ds]}{t} =0, \end{equation}with the understanding that  $\phi _{w,\delta _{123},n-i,m}(\cdot )\equiv 0$ for

$\phi _{w,\delta _{123},n-i,m}(\cdot )\equiv 0$ for  $i>n$. Next, we shall find the above limit but for

$i>n$. Next, we shall find the above limit but for  $i=2$ and begin by writing

$i=2$ and begin by writing

\begin{align*} & \lim_{t \to 0^{+}} \frac{E[1_{\{\hat{\tau}_0>t\}}\int_0^{t} \phi_{w,\delta_{123},n-2,m}(u+cs+\sigma B(s))e^{{-}2\delta_2 s}\,ds]}{t}\\ & \quad = \lim_{t \to 0^{+}} \frac{E[\int_0^{t} \phi_{w,\delta_{123},n-2,m}(u+cs+\sigma B(s))e^{{-}2\delta_2 s}\,ds]}{t}\\ & \qquad -\lim_{t \to 0^{+}} \frac{E[1_{\{\hat{\tau}_0\leq t\}}\int_0^{t} \phi_{w,\delta_{123},n-2,m}(u+cs+\sigma B(s))e^{{-}2\delta_2 s}\,ds]}{t} \\ & \quad =\phi_{w,\delta_{123},n-2,m}(u)-\lim_{t \to 0^{+}} \frac{E[1_{\{\hat{\tau}_0\leq t\}}\int_0^{t} \phi_{w,\delta_{123},n-2,m}(u+cs+\sigma B(s))e^{{-}2\delta_2 s}\,ds]}{t}, \end{align*}

\begin{align*} & \lim_{t \to 0^{+}} \frac{E[1_{\{\hat{\tau}_0>t\}}\int_0^{t} \phi_{w,\delta_{123},n-2,m}(u+cs+\sigma B(s))e^{{-}2\delta_2 s}\,ds]}{t}\\ & \quad = \lim_{t \to 0^{+}} \frac{E[\int_0^{t} \phi_{w,\delta_{123},n-2,m}(u+cs+\sigma B(s))e^{{-}2\delta_2 s}\,ds]}{t}\\ & \qquad -\lim_{t \to 0^{+}} \frac{E[1_{\{\hat{\tau}_0\leq t\}}\int_0^{t} \phi_{w,\delta_{123},n-2,m}(u+cs+\sigma B(s))e^{{-}2\delta_2 s}\,ds]}{t} \\ & \quad =\phi_{w,\delta_{123},n-2,m}(u)-\lim_{t \to 0^{+}} \frac{E[1_{\{\hat{\tau}_0\leq t\}}\int_0^{t} \phi_{w,\delta_{123},n-2,m}(u+cs+\sigma B(s))e^{{-}2\delta_2 s}\,ds]}{t}, \end{align*}where the last equality follows from Fubini's theorem, L'Hôpital's rule and dominated convergence theorem. The limiting term in the last line is indeed equal to zero, which can be shown by noting that the boundedness of  $\phi _{w,\delta _{123},n-2,m}(\cdot )$ in Assumption 2 implies there exists

$\phi _{w,\delta _{123},n-2,m}(\cdot )$ in Assumption 2 implies there exists  $L^{**}>0$ such that

$L^{**}>0$ such that

\begin{align*} \left| \frac{E[1_{\{\hat{\tau}_0\leq t\}}\int_0^{t} \phi_{w,\delta_{123},n-2,m}(u+cs+\sigma B(s))e^{{-}2\delta_2 s}\,ds]}{t}\right| & \leq L^{**} \frac{E[\int_0^{t} e^{{-}2\delta_2 s}\,ds1_{\{\hat{\tau}_0\leq t\}}]}{t}\\ & \le L^{**}\Pr\{\hat{\tau}_0\leq t\}, \end{align*}

\begin{align*} \left| \frac{E[1_{\{\hat{\tau}_0\leq t\}}\int_0^{t} \phi_{w,\delta_{123},n-2,m}(u+cs+\sigma B(s))e^{{-}2\delta_2 s}\,ds]}{t}\right| & \leq L^{**} \frac{E[\int_0^{t} e^{{-}2\delta_2 s}\,ds1_{\{\hat{\tau}_0\leq t\}}]}{t}\\ & \le L^{**}\Pr\{\hat{\tau}_0\leq t\}, \end{align*}and taking limit as  $t \to 0^{+}$ yields zero following the steps in (2.23). Combining this case of

$t \to 0^{+}$ yields zero following the steps in (2.23). Combining this case of  $i=2$ with (2.27) for the case

$i=2$ with (2.27) for the case  $i>2$ results in

$i>2$ results in

\begin{equation} \lim_{t \to 0^{+}} \frac{E[1_{\{\hat{\tau}_0>t\}}\int_0^{t} \phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s))e^{{-}2\delta_2 s}B_{\delta_2}^{i-2}(s)\,ds]}{t} =1_{\{i = 2\}}\phi_{w,\delta_{123},n-i,m}(u). \end{equation}

\begin{equation} \lim_{t \to 0^{+}} \frac{E[1_{\{\hat{\tau}_0>t\}}\int_0^{t} \phi_{w,\delta_{123},n-i,m}(u+cs+\sigma B(s))e^{{-}2\delta_2 s}B_{\delta_2}^{i-2}(s)\,ds]}{t} =1_{\{i = 2\}}\phi_{w,\delta_{123},n-i,m}(u). \end{equation}Similarly, for the fifth expectation in (2.25), we get

\begin{equation} \lim_{t \to 0^{+}} \frac{E[1_{\{\hat{\tau}_0>t\}}\int_0^{t} e^{-\delta_2 s} B_{\delta_2}^{i-1}(s) \phi_{w,\delta_{123},n-i,m}'(u+cs+\sigma B(s))\,ds]}{t} =1_{\{i = 1\}}\phi_{w,\delta_{123},n-i,m}'(u). \end{equation}